- As climate change has become increasingly problematic for the world, the investment community is starting to pay attention to the investment risks it poses. In this paper, however, we focus on the exciting opportunities in companies involved in combating climate change (i.e., the climate change sector), either through climate change mitigation or helping the world adapt to climate change.

- As costs have fallen for solar, wind, batteries, etc., we are approaching an inflection point where clean energy solutions will be cheaper than conventional alternatives, even in the absence of subsidies. We believe the improving economics for clean energy combined with a growing global awareness of the magnitude of the problem we’re up against will support secular growth in the climate change sector for decades to come.

- We think current growth projections are likely to dramatically understate realized growth as the world continues to mobilize to address climate change and costs continue to fall for clean energy solutions.

- Liquidity, cost, and the ability to diversify are advantages to investing in the climate change sector via the public equity market rather than via private investment.

- We don’t believe that you have to sacrifice returns in order to invest in companies helping the world address climate change; on the contrary, we believe there will be many opportunities to generate strong returns.

- Despite strong growth projections, the climate change sector has generally been trading in line with the broad equity market from a valuation perspective.

- We believe that the climate change sector is likely to be a particularly inefficient sector and that a disciplined value orientation will be key to harvesting strong returns.

- Though there are risks to investing in the climate change sector, the risks we worry about are the same risks investors face in other sectors: getting caught up in hype and stories, paying the wrong price, and investing in industries with poor competitive dynamics.

Introduction

Rising oceans and intensifying hurricanes threaten our coastlines, more frequent and severe droughts and floods threaten our food and water supplies, and wildfires threaten our forests and infrastructure. As temperatures have accelerated upward and the deleterious effects of rising temperatures have become more apparent, we’ve become increasingly worried about the impact of climate change on the world. We believe the problems and risks associated with climate change are much worse than the average investor or businessperson realizes.

The challenge in heading off climate change is enormous and has profound investment implications. As Jeremy noted in 2010, “Global warming will be the most important investment issue for the foreseeable future.”1 Climate change poses many risks for investors. Carbon pricing, technological disruption in the energy, automobile and utilities industries, and stranded assets (i.e., the risk that fossil fuel producers will be forced to leave reserves in the ground) are just a few examples of climaterelated threats that loom large and must be considered in constructing a portfolio.

In this paper, however, we focus on climate change-related opportunities. Over the past few years, public policy support combined with the dramatically declining costs of solar, wind, and batteries have spurred unexpectedly strong growth in renewables and electric vehicles. We expect strong secular growth in clean energy efforts to continue in the coming decades and to provide investors with opportunities to invest in companies that both deliver impressive returns and help the world avert the potentially disastrous consequences of climate change. Over the past few years, our research into clean energy, batteries and storage, electric vehicles, energy efficiency, and other clean energy solutions has led us to believe there are tremendous investment opportunities for long-term investors willing to take on shorter-term risk.

The climate change sector

As we think about businesses that stand to benefit from heightened efforts to address climate change, we see business models focused on the mitigation of climate change and the transition to a clean energy world. In addition, we see businesses that will help the world adapt to the impacts of climate change. In aggregate, let’s refer to this as the climate change sector.

Mitigation

Industries involved in the mitigation of climate change and the transition to a clean energy world include solar, wind, nuclear, hydro, geothermal, batteries and storage, smart grid, and clean power generation. Importantly, we also look at the inputs into these efforts, so lithium, copper, and other critical materials fit the bill as well. Energy efficiency efforts are also within scope, including energy efficient building materials, energy efficient lighting, and electric vehicles.

Adaptation

Climate change is already impacting the world, and these effects will become more pronounced as temperatures continue to rise. We consider companies helping the world adapt to a changing climate as part of the climate change sector as well. The impacts of climate change on agriculture and water are particularly worrying. A recent study published by the National Academy of Sciences concluded that as temperatures continue to rise, agricultural productivity could drop to levels last seen prior to 1980 by the year 2050.2 Good luck feeding 9 or 10 billion people in 2050 with productivity at 1980 levels or worse! Companies helping to support agricultural productivity through the production of seeds, fertilizers, farm machinery, etc., would find desperate need for their products. Droughts, floods, and changes in precipitation patterns also threaten our water supply. We believe companies focused on water recycling and treatment, water use minimization, and water system engineering will find their services in high demand as well.

The secular growth opportunity

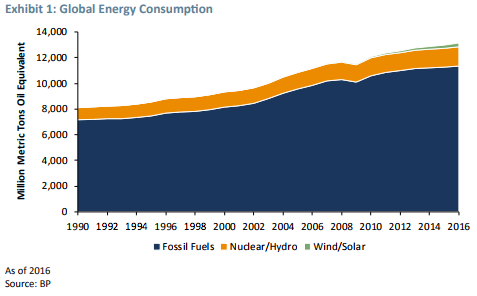

The transition to clean energy will be no small task. The International Energy Agency (IEA) estimates that it will cost $9 trillion through 2050 to decarbonize electricity with another $6.4 trillion going into energy efficiency efforts in the buildings, industry, and transportation sectors. In order to meet the intended nationally determined contributions (INDCs) associated with the Paris Agreement, the IEA expects it will take another $4 to $5 trillion to overhaul the world’s archaic electric grids through 2030. The need for investment is somewhat staggering; however, these numbers pale in comparison with the potential costs associated with climate change, and despite considerable growth over the last few years and lots of media attention, renewable energy continues to represent a small fraction of the overall energy puzzle (see Exhibit 1). Fossil fuel consumption continues to rise, and carbon dioxide concentrations in the atmosphere continue to hit record highs year after year.

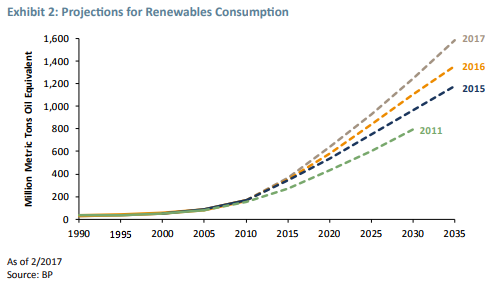

The good news is that wind and solar are expected to grow at a substantial rate for the next few decades. Importantly, the projections for renewables growth have continually been revised upwards (see Exhibit 2), and we believe that current projections are likely to fall well short of the growth that is actually realized as the world continues to mobilize to address climate change. Unanticipated growth, of course, sows the seeds for great investment opportunities.

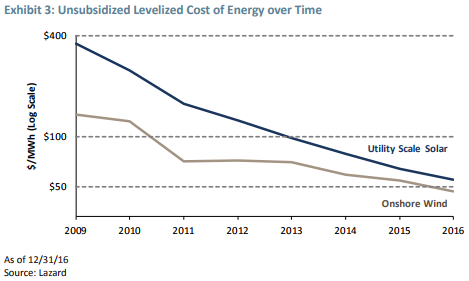

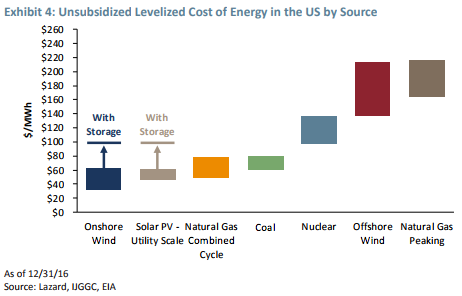

Two factors behind the repeated upward revisions to projections for renewables are general forecasting conservatism/anchoring and the falling costs of renewables. The latter factor is measurable and has been particularly impressive. Wind and solar costs have declined dramatically over the past few years (see Exhibit 3), and renewables are increasingly competitive even without subsidies (see Exhibit 4). Even better, the costs for renewables are expected to continue to fall into the future. While there are still challenges surrounding storage and the integration of intermittent, distributed renewables into the electric grid, we can now see the light at the end of the tunnel, a far cry from where we were just a few years ago. Imagine where we might be a few years from now.

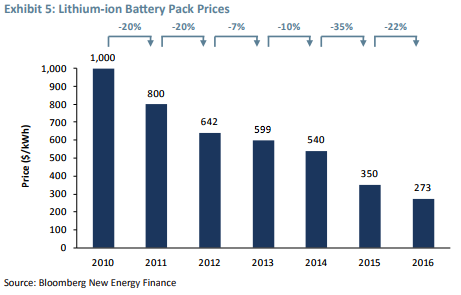

We see a similar story in electric vehicles, where electric vehicle sales have grown rapidly in the last few years and are expected to do so for many years to come. Electric vehicles continue to represent a tiny sliver of overall vehicle sales,3 but once again, falling costs bode well for the future; lithium-ion battery costs have fallen by almost three quarters over the last few years (see Exhibit 5) and are expected to fall dramatically from here. Given that battery costs generally make up approximately 20-25% of the cost of an electric vehicle, declining battery costs will make a big impact on the competitiveness of electric vehicles. Various projections indicate that electric vehicles will be cheaper than internal combustion engine vehicles within 5 to 10 years; when that happens, electric vehicles will be an economic nobrainer. Why would you pay more for a vehicle that costs more to run (i.e., fuel costs) and to maintain4 and pollutes the environment? There could be a rapid transition to electric vehicles, much more rapid than generally understood. None of this, by the way, means that Tesla is necessarily a good investment. More on valuation later…

Global public policy and the private market will support the clean energy transition

At first glance, President Trump’s decision to exit the Paris Agreement seems like bad news for climate change mitigation efforts. Unintentionally, though, the decision has had a galvanizing effect on those concerned about climate change; cities, states, universities, and businesses within the United States have banded together in various forms to commit to meeting, or perhaps exceeding, the US’s Paris Agreement commitment. In an ironic twist, President Trump’s decision to withdraw from the Paris Agreement has drawn more attention to climate change than environmentalists have been able to generate in the last 20 years. In the wake of the decision, climate change was front page news, and internet searches on the subject jumped by hundreds of percent.

There’s also still a fair amount of uncertainty about US federal policy with regards to climate change. Climate change is a multi-decade problem. In that context, the effects of any one administration’s policies are limited, and, as the abandonment of the Clean Power Plan demonstrates, policies aren’t permanent. President Trump has also indicated that he’s “okay” with the federal tax credits incentivizing solar and wind development, and the tax credits are perhaps the most important support for US renewable energy efforts. Additionally, with the renewables industry growing jobs at almost 10 times the pace of the broad job market coupled with the administration’s focus on job growth, it’s hard to imagine the government endangering the 200,000 jobs that are expected to be added to the booming renewable energy industry by 2020. Even now, Mr. Trump himself is talking about putting solar panels on his proposed wall at the US-Mexico border!

More importantly, climate change is a global problem, not a US one, and rather than wavering on their promises, other countries have instead rallied together to reaffirm their commitments in the wake of President Trump’s decision. China, India, and others are champing at the bit to take a leadership position on climate change and to reap the potential rewards. Germany, France, China, India, and others are setting goals to eliminate internal combustion engine vehicle sales within the next two decades or so, and many countries are targeting dramatic increases in renewable energy capacity. If anything, the global community seems to be accelerating efforts to address the challenges posed by climate change.

While public policy support has been critical for clean energy in the past, it’s not obvious that it will be a necessity going forward. As renewables, electric vehicles, etc., become cheaper than conventional alternatives, public policy will be icing on the cake. We believe the combination of global public policy support, the profit-seeking private market, and the continually increasing competitiveness of clean energy solutions will support growth for many years to come. We are in the very early stages of a massive transition to clean energy, and in a world struggling to find growth, climate change-related industries should truly stand out.

Investing in the climate change sector: public vs. private equity

There are two obvious options for investors interested in accessing the opportunities in the climate change sector: public and private equity. There are important differences in the lifecycle stage and risk/return profiles offered by public equities and venture capital start-ups. Public equities provide exposure to more mature, proven technologies, while start-ups offer the chance at a game-changer and the associated windfall, as well as the much more frequent disappointments and bankruptcies. These seem like differences, not necessarily advantages or disadvantages. However, while this doesn’t seem like an “either/or” question, there are some advantages to the public equities.

Perhaps most importantly, the public equity markets offer a relatively easy avenue for diversification, and we think diversification is important in the climate change sector. There will be a fair amount of uncertainty about the precise growth rates of various segments of the climate change sector, and we believe that it will be important to invest in a variety of business models that stand to benefit from efforts to address climate change. It would be extremely difficult and expensive to pull together a basket of private investments spanning wind, solar, geothermal, smart grid, storage, seeds, fertilizer, and water, just to pick a few relevant industries. Getting this type of diversification via the public equity markets is much more achievable.

Liquidity also obviously favors the public equity markets, and while this is always the case, we believe it’s particularly important in the climate change sector where there is the potential for a large amount of technological disruption. It would be painful to sit on a 10-year lock-up in a technology that has been rendered obsolete due to a technological breakthrough.

Finally, let’s not overlook the cost advantages of public equities over private equity or the difficulty getting access to the few private equity managers with identifiable skill. We’ve chosen to focus our efforts on opportunities in the public equity markets, but public and private equity investments can certainly complement each other.

The opportunity in the public equity markets

Risk and returns

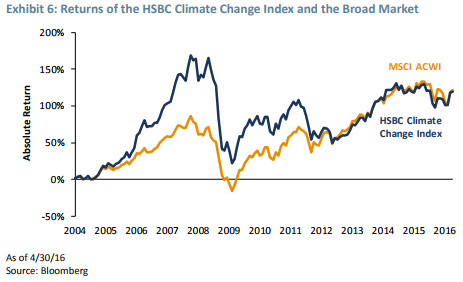

In impact investing circles, there’s often a belief that you have to give up returns when making investments that help the world, so it’s reasonable to wonder how returns have been in the climate change sector. Unfortunately, we can’t study the climate change sector going back 90 years the way we would study financials or energy companies. The longest running relevant index was the HSBC Climate Change Index, which was run for around 12 years before being discontinued in March of 2016.5 Over the entirety of its existence, the HSBC Climate Change Index kept up with the broad equity market,6 albeit with volatility about 15% higher than the broad market and a somewhat different pattern (see Exhibit 6).

The negative spin on this would be that the HSBC Climate Change Index delivered the same returns as the broad equity market with significantly higher volatility, not exactly a dream risk/return tradeoff. The big run-up and subsequent drawdown for the HSBC Climate Change Index revolved around the energy spike when oil prices peaked around $150 per barrel in July 2008. Energy prices dragged the entire energy sector along for the ride, and obviously the prospects for renewables are much better with oil and natural gas prices at the dizzying heights we saw back then. As oil and natural gas prices came back down to earth, the HSBC Climate Change Index did as well, and for the last few years of its existence, it tracked closely with the broad equity market.

The positive spin would be that the HSBC Climate Change Index delivered equity-like returns during a period in which the economics weren’t favorable for many of the constituents (e.g., wind, solar, electric vehicles). As discussed, the economics for clean energy have improved considerably and we believe will continue to improve in the future, opening the door for better returns going forward. We don’t think there’s a tax associated with investing in the climate change sector. On the contrary, we believe a pragmatic, disciplined, value-oriented approach to the climate change sector can lead to impressive returns.

The valuation of the climate change sector

Buying at a good price is always the tricky part when investing in a secular growth story, so how is the climate change sector valued today? In recent months, our internal Climate Change Universe has generally traded in line with or at a slight discount to the broad equity market; as a sanity check, the valuation of the MSCI Global Environment Index, though an imperfect proxy for how we define the climate change sector, paints a similar picture.7 This may seem a bit incongruous; there’s a great growth opportunity, but investors don’t have to pay a premium to access that growth. This is in stark contrast to the Tech Bubble, where investors paid 50, 100, or much higher earnings multiples to get exposure to expected growth. Why aren’t investors paying a premium for companies expected to grow faster than the market? Well, the most obvious answer we can see is that while it may be almost certain that companies in the climate change sector will grow their top-line revenues faster than the broad market, it’s much less certain that they’ll be able to convert that top-line growth to bottom-line earnings and profits. Obviously, sales growth, in and of itself, doesn’t do much good for equity investors.

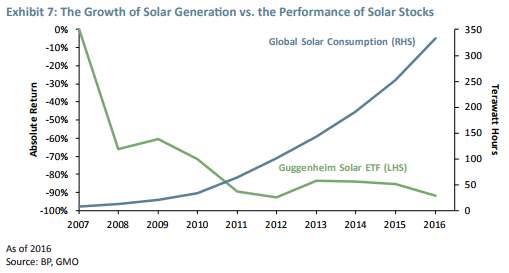

The market may be particularly worried about this considering the spotty history of alternative energy investments. Two solar ETFs that launched in 2008, the Guggenheim Solar ETF and the VanEck Vectors Solar Energy ETF, are down more than 90% since inception8 despite strong growth in solar installed capacity (see Exhibit 7). While 2008 was a particularly inopportune time to launch a solar ETF due to the impending collapse in energy prices, it’s clear that the solar industry has been more effective at electricity generation than earnings generation. The competitive dynamics of the industry haven’t favored profitability: relatively simple technology, lots of competitors, very little product differentiation, and almost no barriers to entry. Throw the dumping of cheap Chinese solar panels into the mix, and you have a problem on your hands.

The importance of a value orientation

This leads us to an important point. We don’t believe that you’ll magically make money by investing in the climate change sector. We think there will be great opportunities, but in order to harvest those opportunities, it will be important to focus on the fundamentals, understand the industry dynamics within the sector (no small task!), and pay close attention to the prices on offer.

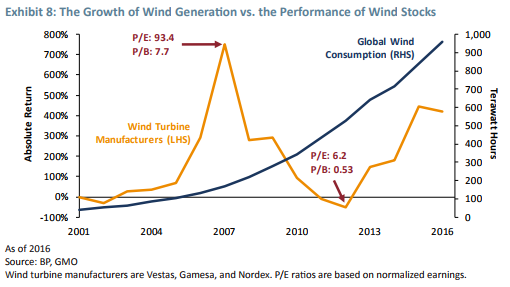

To underscore the importance of value, let’s look at wind turbine manufacturers going back a bit further than we looked at the solar ETFs (see Exhibit 8). The major wind companies, operating in an industry with much better competitive dynamics than the solar industry, delivered almost 16% per annum from 2000 through June of this year, a healthy outperformance of around 11% per annum relative to MSCI ACWI. Yet, investors who bought into wind at the energy peak in 2007-08 had a very different experience; this shouldn’t be too surprising given that wind companies were trading at around 100 times normalized earnings and 8 times book value at the end of 2007. Very few investments end up justifying such lofty valuations. In contrast, those brave enough to invest in the out-of-favor wind industry in 2012, when wind companies traded at 6 times normalized earnings and half book value, have been rewarded with returns of more than 50% per annum over the last 5 years.9

Once again, we don’t think it’s enough to invest in the climate change sector and expect things to work out well. Where there is growth and innovation, and both will surely be in plentiful supply in the climate change sector, there will be hype and hysteria. We believe that it’s critical to have a disciplined value orientation and to understand the evolving fundamentals of the relevant industries and companies.

The climate change sector is likely to be particularly inefficient

We also think that a value orientation will be particularly effective in the climate change sector, as it’s likely to be relatively inefficient. One reason for the inefficiencies is that analyst coverage is low. We can measure coverage on the sell side where MSCI ACWI constituents have about 50% more coverage than the constituents of our Climate Change Universe. Anecdotally, we’ve seen this to be true on the buy side as well, where there are many more bank or consumer staples analysts than solar or storage analysts.

Additionally, the climate change sector, at least as we’ve defined it, is a small to mid cap universe at this point. The biggest company in our Climate Change Universe has a market cap of around $50 billion. The biggest solar companies in the world are a few billion dollars in market cap, trivial compared to the behemoths in the oil and gas industry.

The climate change sector is also a relatively new, poorly understood sector; in fact, we more or less made it up! Understanding the big picture, global policies, the details of changing technologies, and the companies themselves is a tall order. The uncertainty about how things will play out leads to large swings in sentiment and wide dispersions in expectations, all things that breed opportunities. Yet, value managers are unlikely to frequent the climate change sector precisely because of the uncertainties and the inability to identify a comfortable margin of safety. To the extent that value managers aren’t fishing in this pond, we expect to see bigger fish.

All in all, we expect the climate change sector to be fertile ground for stock selection.

Risks to investing in the climate change sector

While we think the opportunities in the climate change sector are exciting, there are obviously risks. Clearly, there are policy risks. The United States pulling out of the Paris Agreement is a good example of a policy change that could impact clean energy efforts, though as we noted, it may paradoxically end up being a positive. China or India or other major countries wavering on their commitments would have an impact as well, though things seem to be trending in a positive direction right now.

Technological disruption is another significant risk to investing in the climate change sector. For the most part, this risk can be mitigated through diversification. However, one can’t completely discount the possibility that cold fusion or some unforeseen technology changes the game in a way that affects large swaths of the climate change sector. This possibility seems remote enough – at least in the next couple decades – that it won’t keep us up at night.10 A lot of people have spent a lot of time and money trying to develop clean energy, and the advances we see are generally incremental in nature.

The main risks investors face in the climate change sector are the same risks investors face in other sectors of the market: getting caught up in hype and stories, paying the wrong price, and investing in industries with poor competitive dynamics. These risks loom larger in our minds than policy or disruption risk, but they all must be considered when investing in this sector.

Conclusions

We believe that there are likely to be tremendous investment opportunities in the climate change sector for many years to come. The consequences of inaction on climate change are unthinkably high, and the world will continue to mobilize in ways not currently foreseen in order to address the biggest threat humanity has ever faced. We expect the unanticipated growth resulting from these efforts and the uncertainty about the path of the clean energy transition to provide investors with many opportunities. We believe that a value orientation and a deep understanding of the fundamentals will be the most effective way of identifying the winners. Investors that get this right stand to enjoy heroic returns.

1 Jeremy Grantham, “Summer Essays,” GMO 2Q 2010 Quarterly Letter, available with registration at www.gmo.com.

2 Xin-Zhong Liang et al., “Determining climate effects on US total agricultural productivity,” Proceedings of the National Academy of Sciences of the United States of America, 2017.

3 In 2016, battery and plug-in hybrid electric vehicles combined made up around 1% of overall vehicle sales.

4 Electric vehicles are expected to be much easier and less expensive to maintain because they have far fewer moving parts.

5 Our understanding is that the discontinuation of the HSBC Climate Change Index was part of a broader decision to no longer support various indexes due to regulatory changes and legal concerns.

6 The broad equity market is represented by the MSCI All Country World Index (MSCI ACWI).

7 As of June 2017, the median P/IBES Forward Earnings for the GMO Climate Change Universe, the MSCI Global Environment Index, and MSCI ACWI were 16.9, 19.0, and 17.3 respectively.

8 Through June 2017.

9 Through June 2017.

10 As investors. Clearly, a groundbreaking technological breakthrough like cold fusion would be great for the world.

Lucas White is the lead portfolio manager for the GMO Climate Change Strategy and a member of GMO’s Focused Equity team. Previously at GMO, he served in other capacities, including portfolio management for the Global Equity team and leadership of strategic firm-wide initiatives. Prior to joining GMO in 2006, he worked as a programmer and analyst for Standish Mellon Asset Management. Mr. White earned his B.A. in Economics and Psychology from Duke University. He is a CFA charterholder.

Jeremy Grantham co-founded GMO in 1977 and is a member of GMO’s Asset Allocation team, serving as the firm’s chief investment strategist. Prior to GMO’s founding, Mr. Grantham was co-founder of Batterymarch Financial Management in 1969 where he recommended commercial indexing in 1971, one of several claims to being first. He began his investment career as an economist with Royal Dutch Shell. He is a member of the GMO Board of Directors and has also served on the investment boards of several non-profit organizations. He earned his undergraduate degree from the University of Sheffield (U.K.) and an MBA from Harvard Business School.

Disclaimer: The views expressed are the views of Lucas White and Jeremy Grantham through the period ending August 2017, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2017 by GMO LLC. All rights reserved.

© GMO

Read more commentaries by GMO