Chautauqua Capital Management is a long-term, quality-growth global equity investor with a generally optimistic view. However, we are less so today. While potentially unpopular to point out market risks, we believe it is important that we be transparent about our market views and how we may be adjusting the portfolio.

To be clear, we do not possess the ability to predict a bear market. But from our perspective as enumerated in the following commentary, risks have increased, and the global financial markets appear to be at a heightened risk of a sell-off. Our concerns are around several factors, including the unwinding of extraordinary central bank policy, high valuations, investor compliancy, and heightened geopolitical risk.

We have already taken some measures to mitigate the negative impact of a potential market sell-off and provide us with greater liquidity to exploit the ensuing pricing anomalies and we may do more. In other words, it is our goal to participate in further upside and protect against the downside should the markets experience disorderly selling.

Background on Central Bank Policy

In the aftermath of the “Great Financial Crisis” borrowing and investing were subdued. In order to stimulate investing and spending, Central Bankers in the developed world embarked on monetary accommodation through interest rate reductions and asset purchases. Those tools are not revolutionary, but the magnitude and length of deployment of those programs are unprecedented. As a lender of last resort, Central Banks have historically been called upon in bank liquidity crises to avert subsequent bank failures by providing cheap capital to banks so they can withstand depositor withdrawals and resume lending to aid economic recovery. Typically, Central Banks set their benchmark rate low enough for member banks to borrow at a low rate on a temporary basis. The benchmark rate influences all other rates across the quality and duration spectrum. Under normal circumstances, government bonds form the basis for the “risk free rate” and should yield about 100 basis points (1%) more than the prevailing rate of inflation. Such historical perspective suggests the U.S. 10-year bond yield should be close to 3.0%, yet today it stands around 2.25%, a discount that is reflective of highly accommodative Central Bank policy.

Such abnormal monetary accommodation from the Central Banks can have a number of consequences. First, it can pull purchasing demand forward. Households may opt to replace a car earlier than they otherwise would because the cost of financing in a low rate environment is thought to be attractive and temporary. Second, monetary stimulus, as compared to fiscal stimulus, is deemed to be a blunt instrument and can aid those who are least in need by making the cost of money cheaper for everybody. On the other hand, fiscal stimulus in the form of tax incentives, for example for new industry development to assist people in a depressed region of the country, is a more precise tool. Third, as rates go lower the interest income from a bond and the dividend income of a stock becomes more valuable. As investors are willing to pay more for these valuable sources of income, asset prices go up. Existing investors experience price appreciation, but with the passage of time the potential for asset prices to continually appreciate comes under a high valuation strain. As yields on 10-year U.S treasury bonds have fallen from 14% to 2% over the past 35 years, investment returns have also fallen. This has been a multi-decade trend but abnormal accommodation has exacerbated what we see as a problem. Lower investment returns have negatively impacted pension plans (many of which have unfunded liabilities and require a higher investment return to compensate) and financial sector businesses such as banks and insurance companies (which need to earn a spread between their borrowing costs or premiums and their investment returns).

Typically, monetary accommodation via abnormally low interest rates is considered an extreme measure that needs to be quickly reversed after the crisis is averted. It is like life support, which needs to be withdrawn once the patient gets moving. This time, however, artificially low interest rates have been consistently applied in the United States, Eurozone, Japan, the United Kingdom, and the countries that peg their currency to a major currency for the past 9 years.

If this were not enough, the same Central Banks also embarked on “Quantitative Easing” (QE). While they are not new, these are often described as unorthodox. Low rates in a recession are often described as pushing on a string – if a potential borrower is simply not in the market to borrow money, low rates will not induce anything. So in addition to setting benchmark interest rates near zero, Central Banks have used their ability to create money and have purchased a massive amount of financial securities.

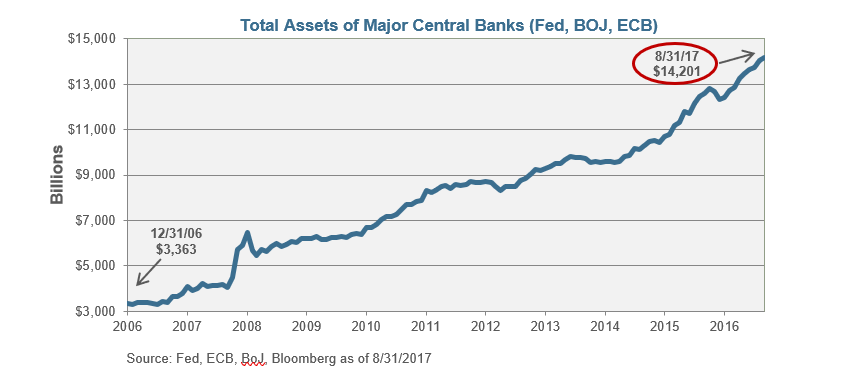

Source: Fed, ECB, BoJ, Bloomberg as of 8/31/2017

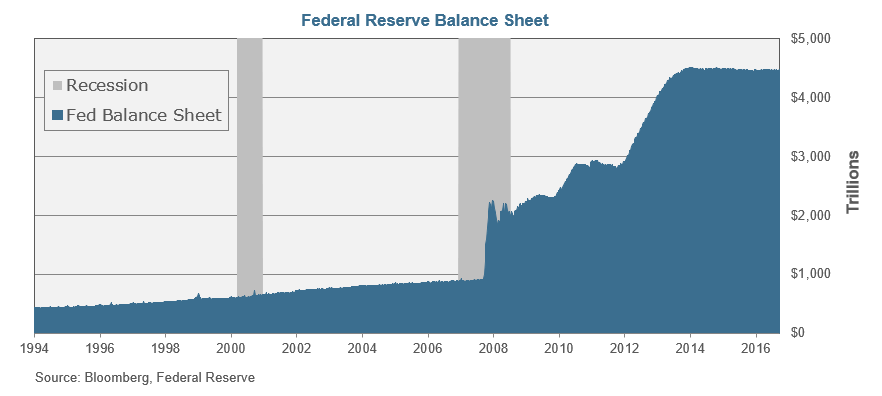

This has had the effect of adding incremental demand, given a stable supply of securities, and infusing money into the economy. When the Federal Reserve buys a U.S. treasury bond from an individual, that individual then has the cash that can be spent on a vacation, used to remodel their home, or invested back into the market. The quantity theory of money states that money times velocity equals price times quantity (MV=PQ). So, in theory, if you increase the supply of money by buying up bonds, you should be able to push prices up, thereby jump starting the rate at which money moves through the economy and increasing the rate of inflation. All of these are desirable when there is a high unemployment rate and an economy is operating at a rate below its full capacity. In the aftermath of the Great Recession such a bold and unorthodox action made sense. However, this tool has been massively applied for such a long time that investors express doubt that they could live without it. In the summer of 2014 the U.S. Fed announced that they would be slowing the level of bond buying, and bond and stock markets sold off in what was described as a “Taper Tantrum”.

Source: Bloomberg, Federal Reserve

Effects on the Current Market

Late in 2014, the U.S. Federal Reserve ceased buying bonds, but at present, it is estimated that the Fed still owns $4.2 trillion worth of bonds. The money supply of the U. S. is reported to be $14 trillion. This would mean at least 30% of the liquidity of money is attributable to the Fed infusing money as they purchased bonds from the market. The European Central Bank (ECB) has been buying bonds at a rate of €60 billion (approximately $71 Billion) per month. While they are beginning to signal that they will reduce and end their bond-buying program, their rate of buying, month after month, year after year, has infused a massive amount of money into European economies and has put upward pressure on bond prices. The Bank of Japan (BOJ) has bought so many bonds that they have had to look to the Japanese equity markets to fill their prescription of asset purchases. In an effort to not favor one company’s shareholders versus another, the BOJ has bought broad based exchange traded funds (ETFs) of Japanese stocks. Their program has been so aggressive that today it is believed that they own about 75% of all Japanese ETFs. Together the Fed, the BOJ and the ECB own one-third of the global bond market.

A few questions come to mind:

- Can economies survive without further QE?

- Has the expanded money supply from QE resulted in increased economic activity and a pick-up in inflation?

- What will happen to the bond and stock markets when asset purchases by Central Banks go away?

Whether because of the stimulus or due to the economy’s self-correcting forces, investors have re-entered the markets, and households and businesses have resumed borrowing. Additionally, excess labor has been absorbed, evidenced by declines in unemployment rates all over the globe. Low unemployment rates exist in the U.S., Japan, Germany, U.K., Denmark, Norway, Switzerland, Hong Kong, Singapore, Thailand, and other countries. These augur for eventual wage-based inflation.

Source: The World Bank, as of 12/31/2016

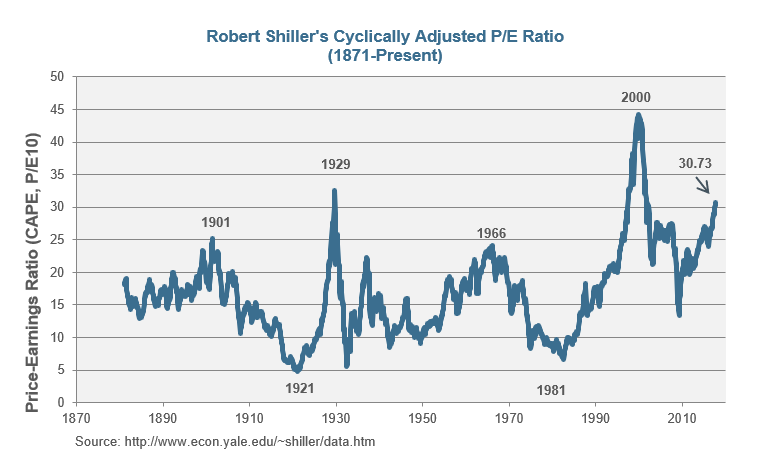

After eight years of global monetary stimulus most financial assets are trading at historically high valuations. Evidence of high risk taking behavior to earn returns akin to what was possible in the past is rampant, and price risk generally seems pervasive. Based on Robert Shiller’s cyclically adjusted P/E ratio, U.S. equities are trading at levels exceeding valuations that preceded the corrections in 1987 and 2007 and not seen since 1998-2000. Further exacerbating valuations are yield chasing investors that have bid up valuations in a number of higher dividend paying equity sectors, including consumer staples, utilities and real-estate. Bond valuations are also skewed as 10-year German Bonds yield 0.25%, while the German Producer Price Index, an inflation proxy, is running at 2.8%. In the U.S., high yield bonds sell at a premium to investment grade bonds on a default-adjusted basis, and debt issued by risky issuers has been oversubscribed.

Source: http://www.econ.yale.edu/~shiller/data.htm

The monetary stimulus that drove high valuations peaked in the spring. Global Central Banks are in different stages of pivoting towards “normalization”. This will involve adjusting their benchmark rates higher and possibly selling bonds and stocks. As they do, they are likely to move in well-signaled, measured steps. Central bank buying (excess demand) has driven interest rates to artificially low levels so, in the absence of support from Central Banks, interest rates will go higher. And as a result, valuation multiples for equities should contract. Absent faster economic growth, which leads to better earnings and lower default rates, asset prices should decline.

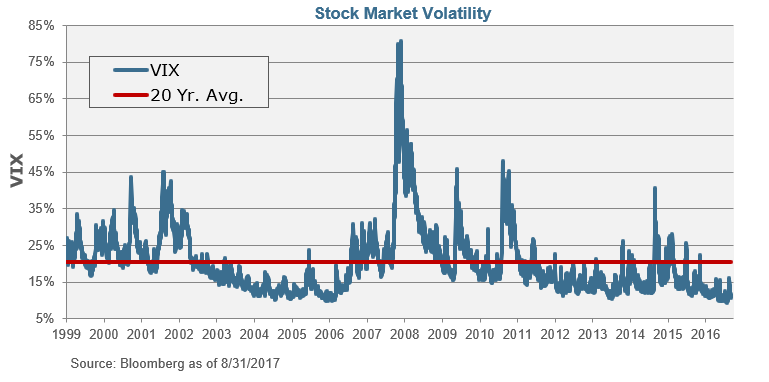

In addition to the risk of rising rates and high equity valuations, we see additional signs of caution. Investors have appeared complacent, as measured by the VIX volatility index, in the face of historically high valuations and potential liquidity withdrawals. This might be expected given global synchronized growth and healthy corporate profits. Recently, market volatility has notched up, though likely in reaction to North Korea’s nuclear weapon threats and hurricanes.

Source: Bloomberg as of 8/31/2017

Although the typical market exuberance that accompanies stock market tops is not anecdotally obvious, market participation in the U.S. as measured by low cash levels, new account openings and record high levels of margin debt implies that the upward force of additional market participation may be running out of steam.

What makes some equity markets potentially fragile, in our view, is the increased presence of value-agnostic participants (e.g. index funds, ETFs and algorithmic traders) who are likely to be less rational in a market sell-off. This is illustrated by JP Morgan’s claim, in Q3 2017, that actively managed assets only represent 10% of U.S. stock market activity. Further, some of the new commingled products may be challenged to meet investor redemption demands. Exchange Traded Funds, also known as ETFs, come in various forms but they are all designed to give the investor exposure to an underlying asset. In some cases the underlying assets may be illiquid. Additionally, since individual securities are imbedded in the broader fund it is not possible to discern where valuation anomalies are occurring. Investors in individual securities often provide price support by buying back in when sell-offs look over done. This is not possible with most ETFs and index funds so this change in market structure may lead to a run-on-the-bank mentality.

Given the more widespread presence of value agnostic participants and higher relative valuation, we believe that the risk of a sell-off is more acute in the United States than in non-U.S. markets. Global economic growth is improving steadily and the removal of monetary accommodation is in its very early stages. Therefore, on a relative basis non-U.S. investments are more attractive in our view. That said, when the U.S. has experienced a significant and disorderly market sell-off in the past it has unnerved investors worldwide.

Chautauqua Capital Management’s Positioning in this Environment

Given all of this, what is an investor to do? Confirmation bias encourages investors to get more bullish as stocks and bonds get more expensive, not less. As a result, expensive markets can appreciate further and further.

But it is hard to make the case, after Chautauqua has achieved returns in excess of 25% for the first nine months of 2017, that it will be easy keeping up that pace. In the current environment history suggests that it might be more prudent to temper our expectations versus becoming more enthusiastic.

Unlike other times over the past few decades there are few areas of the investing universe that are still cheap. This market is different from the 1998 to 2001 internet bubble that was isolated to what people were calling the “New Economy”. That said, there are differing levels of risk in equities around the globe.

Outside of the U.S. there is a smaller presence of value-agnostic participants. This should mean that active investors employing price discovery will be buyers when individual stocks sell below their intrinsic value, which mitigates the risk of all-out panic selling. These non-U.S. markets are also a bit earlier in their course of recovery than the U.S., and their economies are likely to continue to grow after the U.S. economy stalls out. And best of all, by almost every valuation measure, foreign stocks are cheaper. Another benefit to international exposure is that the degree to which the world’s stock markets move in sync with each other has fallen to the lowest level since 1997.1

Simply put, lower correlation between equity markets underpins the risk-reducing diversification benefits to U.S. investors of diversifying internationally. Therefore, we feel less anxious about non-U.S. equities.

As we continue to evaluate new ideas and test the validity of existing holdings. In the deployment of our philosophy and process we continue to emphasize quality and evaluate each idea with regard the factors of growth, profitability and valuation. At this time we want to make sure that we are taking steps to help protect the portfolio, and at the same time, not sacrifice the returns we can achieve through our proprietary and time-tested process.

Accordingly, the partners of Chautauqua Capital Management have taken extra precautions in managing the Chautauqua Global Growth and International Growth funds, such as: getting pre-approval for stop-loss trades and deemphasizing higher beta and higher valuation companies. These actions have already proved helpful. We have made adjustments to ensure that the holdings in the portfolios have adequate liquidity. Finally, while we typically maintain a low cash position, we may take cash levels as high as 10% of total portfolio value, in order to mitigate harm in a disorderly sell-off and, importantly, to redeploy to exploit pricing opportunities that arise.

We believe that the strength of our team, the durability of our investment process, and the selective nature of our portfolios and our strict adherence to our investment disciplines give us a better chance to adapt to change and exploit volatility-driven opportunities. Our superior risk-adjusted returns, relative to the strategies respective indices, have historically been achieved through stock selection skill. This has been especially true during and in the aftermath of choppy markets.

Sincerely,

Brian Beitner, CFA

Managing Director

Brian Beitner is the Senior Portfolio Manager for the Chautauqua International Growth Strategy and Chautauqua Global Growth Strategy. He formed Chautauqua Capital Management in January 2009. Prior to this, he was a member of the TCW Concentrated Core Equities portfolio management team from 1998, which was responsible for the management of up to $27 billion in assets. In 1999, he was named Director of Equity Research. In 2003, he became a Senior Equity Strategist. In 2005, Mr. Beitner began managing International and Global Equity portfolios. Prior to working at Trust Company of the West, he worked with Scudder, Stevens and Clark; Bear Stearns & Co.; and Security Pacific Bank in roles including portfolio management, research, and trading. He earned a B.S. in Public Administration and an M.B.A. from the University of Southern California, Los Angeles. He holds a certificate for Global Investing from INSEAD. He received his CFA charter in 1989.

Important Disclosures

Investors should consider the investment objectives, risks, charges and expenses of the fund carefully before investing. This and other information can be found in the prospectus or summary prospectus. A prospectus or summary prospectus may be obtained from your financial advisor and should be read carefully before investing.

Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. Investments in international and emerging markets securities and ADRs include exposure to risks including currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability.

MSCI ACWI ex-U.S. Index is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed and emerging marketing excluding the United States MSCI EAFE Index: A free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada.

Benchmark returns have been calculated using dividends that are net of withholding taxes, resulting in a net dividend return.

Read more commentaries by Chautauqua Capital Management