A downturn for stocks may not be top of mind these days, but one will happen eventually. To prepare for that, Russ discusses why the source of the selloff matters as much as the magnitude.

With the S&P 500 at another new high and volatility beaten into a state of permanent submission, it seems churlish to discuss preparing for a downturn using hedges and downside protection. That said, while the market rally can continue, it is worth pausing to contemplate how surreal things are getting.

For example, the Sharpe ratio, which measures units of excess return per unity of volatility, is used by professional investors to calculate risk-adjusted returns. Currently, the one-year Sharpe Ratio on the S&P 500 is comfortably above 2, a remarkably high number. Not only is the market producing stellar returns, those returns are coming with virtually no volatility.

With that in mind, and with respect to those who prefer to do their holiday shopping in midsummer, maybe it isn’t too early to start thinking about positioning for the next downturn. The challenge for asset allocators is that when insulating a portfolio, the source of the downturn is as important as the magnitude.

Growth or interest rate shocks

While it is impossible to quantify all the ways things can go wrong, broadly speaking, most corrections fall into one of two broad categories: growth or interest rate shocks. The former describes any event that calls into question economic growth. The latter encompasses periods when investors are facing an unexpected rise in interest rates, either due to an unexpected pickup in inflation or a change in central bank behavior.

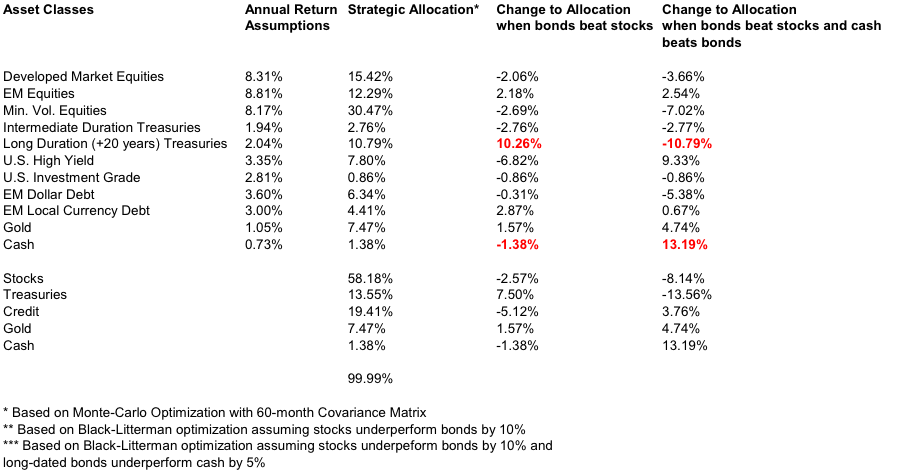

Whether an equity market downturn is caused by a growth or rate shock is a crucial distinction. To illustrate, consider a long-term portfolio targeting a 9% risk level. Now assume a shock that causes stocks to underperform bonds by 10%. Consider this the growth shock, as we assume no change in long-term bond returns.

Analysis of this scenario suggests a few conclusions. The obvious changes: Own less stocks, and of the stocks you do own, opt for lower volatility names. You could also theoretically sell credit and raise a bit of cash. The funds from lower equity, credit and cash would be reallocated to long duration bonds, the preferred post-crisis hedge against equity risk.

Now change the scenario. Using the same methodology consider what happens if stocks are selling off because bonds are underperforming, something that has rarely happened in the post crisis environment.

Under this scenario the portfolio rebalance looks very different. To start, you would want to consider lowering your equity allocation even further than in the first example. The reason is that when rates rise, low volatility stocks are often the worst place to hide. Another difference would be raising the allocation to high yield bonds, which are less rate-sensitive than traditional bonds.

Both growth and rate shocks can produce stock market corrections; what changes is the prescription. The typical post-crisis correction has been driven by a growth scare. But that is not always the case. If the next correction comes from twitchy central banks, running to bonds is counterproductive.

Both growth and rate shocks can produce stock market corrections; what changes is the prescription. The typical post-crisis correction has been driven by a growth scare. But that is not always the case. If the next correction comes from twitchy central banks, running to bonds is counterproductive.