Value stocks have started to show signs of life. Russ discusses why energy and financial stocks are currently the best ways to play the theme.

Value stocks are not surging, but they have at least begun to stir. Since the August lows, U.S. large cap value stocks have gained around 5.50%, in line with the overall market and a bit ahead of growth stocks.

Back at the end of August, I suggested that value was unfairly being left for dead, despite the fact that the style was looking cheap, perhaps cheaper than at any time since 2000. What value lacked was a catalyst, something that has recently emerged in the form of firmer data and resurrected tax cut talk. To the extent this continues, the next question is how to play the theme. Within the U.S. market, energy and financial stocks stand out.

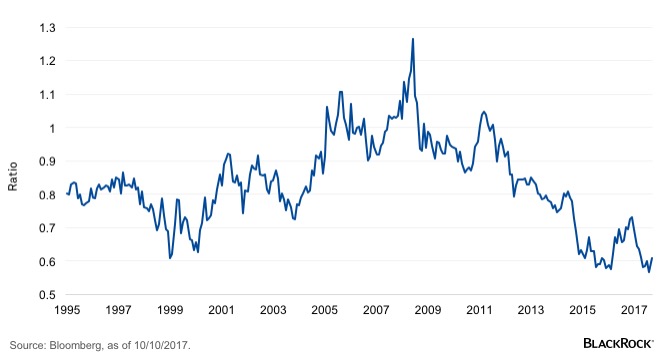

On an absolute basis, financials, energy and utility stocks appear the cheapest based on the price-to-book (P/B) ratio. However, utilities, thanks to a steady stream of bond market refugees searching for yield, are not particularly cheap compared to their history. This leaves energy and financials. Energy in particular appears inexpensive relative to the broader market. Since 1995 the S&P 500 energy sector has traded at approximately a 17% discount to the broader market. Today that discount is nearly 40%. See the chart below.

S&P Energy Sector P/B vs. S&P 500

The preponderance of value in these sectors is also evident in their respective weighting within value indexes. Banks and insurance companies make up around 26% of the S&P 500 Value Index, double their weighting in the S&P 500 Index. Similarly, the weighting of oil and gas in value indexes is approximately double the weight in the broader market.

What to watch: Crude oil and long-term rates

While both energy and financials are likely to continue to benefit from a rebound in value, each has its own idiosyncratic drivers. Not surprisingly, for financials, particularly banks, it is interest rates; and energy companies, the price of oil.

Starting with banks, as you might expect, banks benefit when long-term rates rise and the yield curve steepens. During the past two years, weekly changes in 10-year Treasury yields explained approximately 40% of the weekly moves in the Bank Index.

Energy has a similar story. Since late 2015, weekly changes in crude oil have accounted for more than 50% of the variation in weekly returns. This helps explain why these sectors have performed so well of late: Both interest rates and crude oil have risen sharply in recent weeks.

The takeaway is value still appears cheap. Should economic growth remain firmand investors stay enticed by the possibility of tax cuts, value is likely to continue to perform well. In the U.S., energy and financials appear the best way to play the theme, but with the caveat that each is as much driven by their respective fundamentals as style preferences. The good news is that for now, what is good for value—firmer growth—is also good for rates and oil prices.

Russ Koesterich, CFA, is Portfolio Manager for BlackRock’s Global Allocation team and is a regular contributor to The Blog.

Investing involves risks, including possible loss of principal. Investments that concentrate in specific industries, sectors, markets or asset classes may underperform or be more volatile than other industries, sectors, markets or asset classes and than the general securities market.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of October 2017 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

©2017 BlackRock, Inc. All rights reserved. BLACKROCK is a registered trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

280166

© BlackRock

Read more commentaries by BlackRock