Quarterly Update: October 2017

Last month, after 19 years in operation and running dangerously low on fuel, the Cassini spacecraft executed its final assignment: a death plunge deep into Saturn’s atmosphere where it was crushed and vaporized. At the time of its launch, Cassini’s mission was unprecedented in its ambitions but also in its risks, among them a treacherous pass through the asteroid belt. Yet the expertly designed probe proved a model of reliability over its nearly two decades of service, allowing scientists to extend its mission a total of three times.

In some ways, investors too began a journey into the unknown after the great financial crisis in 2007-2008. And if only we were so fortunate as NASA engineers in applying a rigorous set of scientific principles to timing the economic cycle, we would all be very wealthy indeed. But, alas, the journey of each economic expansion has unique characteristics and unpredictable timetables that are resistant to precise forecasting.

The minds at the Federal Reserve Bank are perhaps the world’s best. However, not once since it was founded in 1913 has the Fed been able to accurately forecast the next recession a year before it materialized. In fact, Fed officials are notorious for being behind the curve. As investment managers, this is all the evidence we need that the better approach is to assess risks and, when they are high and rising, take appropriate steps to mitigate some of those risks where we can.

Despite eight uninterrupted years of growth, and after a 346% rise in total equity returns to new record highs, our analysis indicates that the economic expansion is not yet in peril of ending from natural causes. However, it certainly can end from unnatural causes, like self-inflicted geopolitical problems, or unanticipated hikes in interest rates by the Fed.

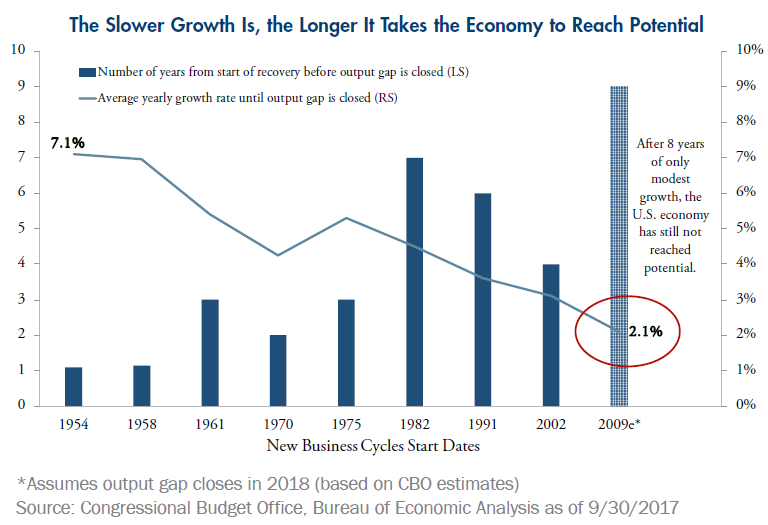

As the nearby chart shows, a lower 2.1% average growth rate over this expansion has led to economic slack being eroded much more slowly than in previous business cycles. In fact, the current output gap is not projected to close until sometime in 2018. This suggests that the economy is in no danger of overheating and that modest growth can continue for some time before excesses build that could lead to the next recessionary downturn. This is also a reason why equities are rising strongly this year. Investors are optimistic because they expect that continuing economic growth will support improving corporate profits over the next several quarters. We agree.

Measuring risks is a process and is statistically supported through rigorous analysis. In thinking about what stage of the current economic expansion and equity bull market we are in, we like to rely on forward-looking indicators and financial market data that has historically been useful as a gauge. Our asset allocation committee continually assesses when risks have grown too high to sustain full exposure to an asset class.

Below are some of the indicators we monitor and where each stands.

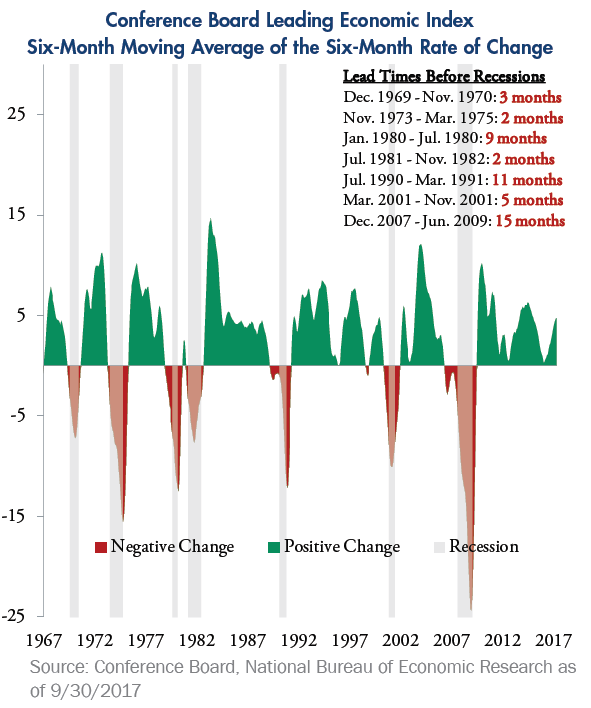

- Leading Economic Index. While the lead time between when the Conference Board’s Leading Economic Indicators turn negative and when a recession begins has historically been highly variable, the index has done a good job of signaling when an expansion is in jeopardy of ending. Recently, the LEI has been improving, indicating that modest growth should continue and that near-term recession risk is low.

- Equity Valuations. Valuations of U.S. equities are now at levels that historically have been categorized as high. However, all this really means is that risks related to valuation are elevated, not that the bull market will end soon. Analysis reveals there is not much correlation historically between valuation levels and the equity market’s return over the next 12 months. In fact, valuations can stay at high levels for years, without stocks correcting.

- Margin Debt. The higher the level of margin debt, the more investors are confident enough to borrow money to buy stocks and bonds. While confidence is high today, we are watching to see if margin debt goes to levels of excessive speculation. So far, it has not.

- High-Yield Debt Interest Rate Spreads. The excess return from investing in lower-quality bonds versus Treasuries totals 5.35% YTD. The present level of HY credit spreads is near a three-year low. However, this relatively low level can persist for years, as was the case from 1994 through 1998 and more recently from early 2004 through mid-2007.

- Leveraged Loans. In the senior secured loan market, the amount of lending currently being made to medium- to low-credit-quality companies without covenants is 75% of new issuance (up from 24% in 2012). This means that borrowers are being granted relatively inexpensive financing without the standard covenant packages and therefore lenders have weaker controls over borrower operations.

While we are confident this economic expansion will not last the almost two decades that Cassini did, if it continues for 22 months more, it will be the longest in U.S. history. Given the highly uncertain geopolitical environment, we might have to navigate an asteroid belt of our own over the next year to get there, but our best estimate is that modest economic growth will continue through 2018. Still, rather than try to predict what is not predictable, we believe assessing risks and investing in high-quality companies with improving future earnings prospects, adaptive management teams, and strong balance sheets remains the best way of sustaining your investment portfolio and achieving long-term investment goals.

Garrett R. D’Alessandro, CFA, CAIA, AIF®

Chief Executive Officer and Chief Investment Officer

City National Rochdale

Productivity, Growth, and U.S. GDP

By Garrett D’Alessandro, CFA, CAIA, AIF®

- Modest growth rate contributes to length of economic expansion

- Low levels of business investment hurting productivity growth

- Less regulation, lower taxes could help the economy significantly

The U.S. economic expansion is in good condition and will likely last well into 2018 and potentially beyond. More Americans are working today than ever before, household balance sheets are healthy, housing is growing steadily, and equities are setting record highs. Contributing to the longevity of this expansion is that the modest rate of growth we have experienced has not led to any substantial imbalances that could cause a recession. As a result, although interest rates and inflation historically have risen after an expansion of this length, this time they have remained low.

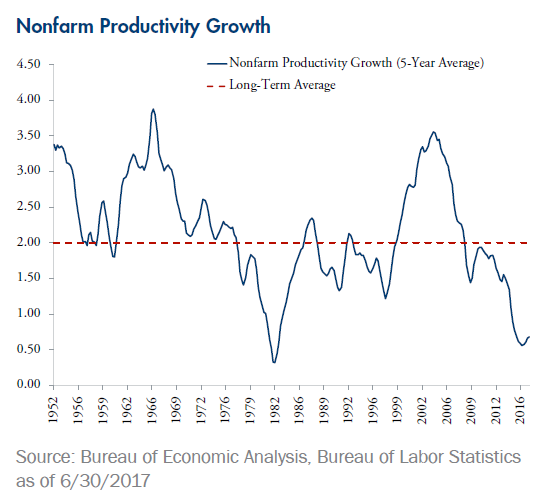

The biggest problem facing the economy is that labor productivity growth, a key driver of rising living standards, has fallen to the lowest level since the early 1980s (see chart). Nearly 17 million jobs have been created in this expansion, but, because wages are not rising as much as they would if productivity was increasing, this has not spurred the type of increases in consumer spending that drive significant GDP growth. In addition, due to the severity of the Great Recession, households now have a higher propensity to save and are not taking on the same levels of debt they once did. Combining these factors leads to this expansion being steady but modest, with GDP growing at about 2% annually.

Part of the slowdown in productivity growth is likely due to the fading impacts of the IT revolution. Demographic changes are also playing a role, with the economy increasingly relying on older workers whose productivity is not as likely to rise as much as that of their younger associates. More recently, the makeup of job gains has been skewed toward lower-productivity industries and away from high-productivity ones where technological advances have the most impact. Firms in industries such as information and mining have hired fewer people, while sectors such as education, leisure and hospitality, and healthcare services have hired more.

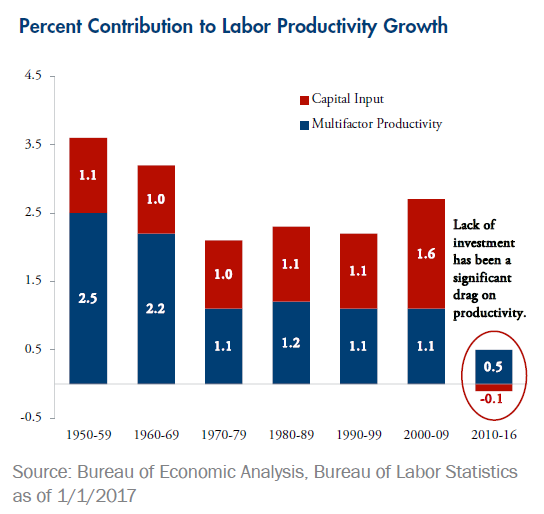

Perhaps the biggest contributing factor, though, has been the pullback in business investment. The contribution to productivity growth from capital intensity fell from an average of 1.6% between 2000 and 2009 to -0.1% between 2010 and 2016 – a glaring decline (see chart). Despite high levels of corporate cash, low interest rates, and widely accessible capital market funding, business investment has been one of the more disappointing elements of the economic recovery. Since the Great Recession, the level of capital relative to labor and output has been declining or flat. Instead of adding to productivity growth, it has subtracted from it.

So what could turn things around? Several policy changes from Washington could provide the key to spurring capital investment by American businesses. The first is the ongoing effort to reduce government regulation and provide a more favorable climate for investment. Ever-increasing regulation, however well intentioned, has been detrimental to the formation of capital, especially for the average worker. Small businesses surveyed by the NFIB have increasingly cited government requirements as their single most important challenge. Overall, the Competitive Enterprise Institute estimates that nearly 10% of GDP is associated with the cost of federal regulation and intervention.

Likewise, there is bipartisan agreement that the current corporate tax code is overly complex and contains perverse incentives. Capital is mobile, and a higher tax rate hurts America’s competitive position as a place for businesses to invest. Research by the Organisation for Economic Co-operation and Development has found that corporate tax rates have the most adverse impact on business investment and productivity. One study found that a 10% reduction in the current rate could lift annual growth in GDP per capita by 1-2%.

Addressing all these factors would have a favorable impact on potential GDP growth, though increasing capital investment back to precrisis levels still wouldn’t be enough alone to lift growth all the way up to 3%. Historically, productivity advances in bursts for a few years, then settles down, and then advances in another burst. What makes the U.S. economy one of the world’s best is our ability to innovate, and that is usually dependent on both business and government capital spending.

The challenge the U.S. economy finds itself in is a negative feedback loop. Lower productivity per worker drives labor costs up and profits down. With modest demand, businesses don’t see enough ROI from increased capital spending and thus are hesitant to invest in the equipment needed to make workers more efficient or the research necessary for the next technological breakthrough.

Putting all of this in perspective leaves us with a comprehensive assessment of why this expansion has been steady but modest and why it looks likely to continue well into 2018. The longest expansion in U.S. history occurred from 1991 to 2001 (120 months); the current one could potentially turn out to be even longer. With a disciplined Fed, no adverse geopolitical events, and some modest reductions in small and medium business taxes, we might have more than a year left for this expansion. While we want productivity and innovation to grow at better rates, there is an offsetting benefit: this slow and steady expansion is likely to continue.

American Households in Best Financial Shape in Decades

By Paul Single and Steven Denike

- Healthy households are a major positive for the economy

- Consumers are generally employed, wealthier, and increasingly confident

- Income growth, a key driver of spending, is on the rise

Consumer sentiment has reached its highest level in 16 years, and a quick look at American household fundamentals helps explains why. The jobless rate is now below its prerecession low and likely to fall further. Meanwhile, household net worth is at an all-time high, debt has been reduced, and rising housing prices have pulled millions of homeowners out of negative equity. Perhaps the best news though has been the rapid rebound in household income over the past few years.

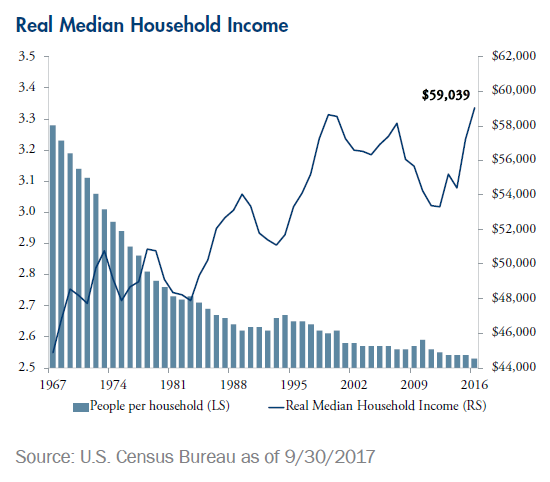

The Census Bureau recently reported that real median household income increased in 2016 for the fourth consecutive year and now stands at its highest level ever. Longer-term gains are even more impressive, especially considering average household size has gradually declined over the last 50 years (see chart). The typical household today has an annual income $14,144 greater than in 1967 – that’s almost $1,200 every month for fewer people.

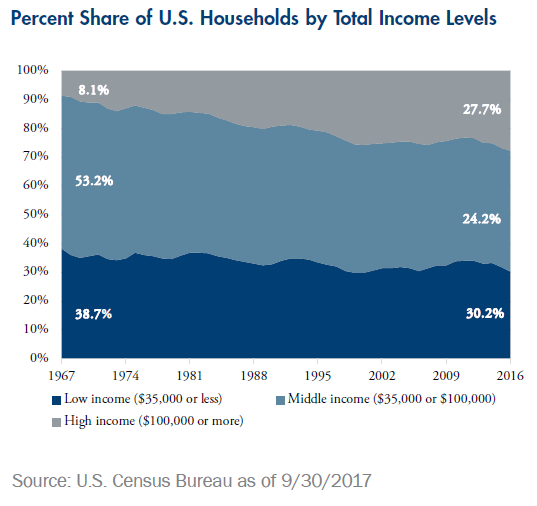

And it’s not just the wealthy who are benefiting from the current economic expansion anymore. Recently, those on the lower end of income distribution have seen their income gains outpace those on the higher end—a continuation of a long-term trend in upward mobility that has unfortunately gone underreported. Yes, the “middle-class is disappearing,” but it’s because households are gradually moving up into higher income groups, not down into lower ones (see chart).

Not all the news is good. The aftereffects of the Great Recession included many years of income stagnation that cannot be made up, and a good part of recent gains have come because Americans are working harder and longer rather than experiencing significant wage growth. Many families also are now having to rely on more than one breadwinner to get ahead. Still, from a broader perspective, the average U.S. household is in better shape today than it’s been in a very long time.

When asked about our positive outlook for the economy, we point to the consumer sector. The extent of the U.S. economy’s dependence on the consumer for growth is difficult to overstate. Personal household consumption accounts for nearly 70% of U.S. GDP, a figure that’s more than 10% higher than the average for other developed countries. Or, put another way, as long as the U.S. consumer continues to do well, the U.S. economy should too.

Dividend Equities Continuing to Accrue Value

By David Abella, CFA

- Dividend growth has outpaced stock returns in several sectors

- Ongoing economic expansion is positive for yield-oriented equities

- Strong operating earnings driving dividends toward our growth targets

After a good performance in 2016, the challenge for dividend stocks this year was to continue to deliver attractive total returns, particularly in light of a rising interest rate environment. As 2017 progressed, we have seen a strong rally in the S&P 500 index, with particular benefit to large-cap growth stocks. This has left some investors in dividend-oriented equities wondering if there are still opportunities in these stocks.

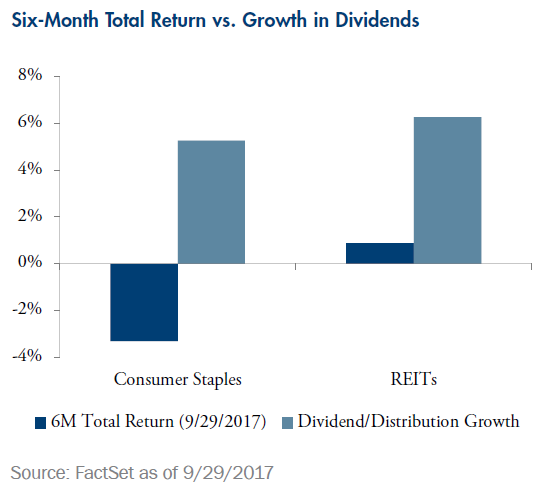

We remain optimistic about our dividend-paying companies in light of their strong operating performance and solid dividend growth. We are aware that our High Dividend & Income (HDI) buy universe stocks have not moved up at nearly the same pace as large-cap growth stocks. We also note that some of our sectors, notably Real Estate Investment Trusts (REITs) and Consumer Staples, have had relative underperformance over the past six months despite a steadily rising rate of dividend growth (see chart). However, in our view, this muted performance relative to dividend growth has enabled our HDI buy universe stocks to accrue value and makes them more attractive over the long haul.

With two interest rate hikes already enacted by the Federal Reserve and one more possible this year, investors continue to wonder about the potential effects of rising interest rates on income-oriented equities.

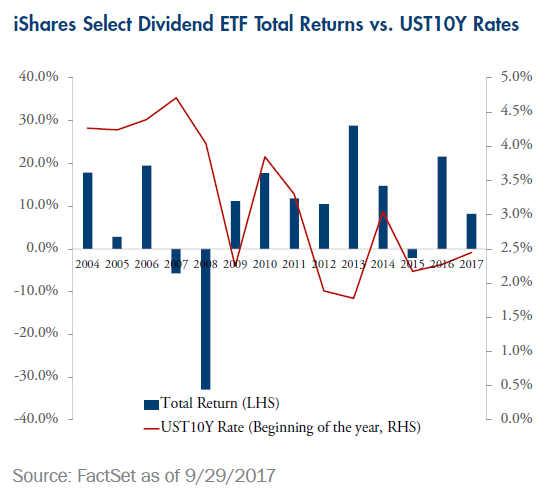

As part of our equity analysis work, we seek to invest in companies that can grow their earnings and dividends consistently. We have found that these stocks have performed well over longer periods of time. In the second chart, we see how the iShares Select Dividend ETF has performed over the past 13 years. Overall, the total return has been independent of the level and move in rates, as represented by the 10-year Treasury. We target dividend growth of 3-8%, which we feel can offset some of the effect of rising rates and help drive our longer-term total returns.

Going forward, we feel that modest return expectations in the 5-7% range, driven by solid dividend yields and their projected growth, continue to be realistic.

Interest Rates Poised to Rise Further, but Sharp Increase Unlikely

By Gregory S. Kaplan, CFA

- Fed may delay next hike after soft inflation readings; hurricanes

- Key for investors is not timing of hikes but where rate winds up

- “Barbell” portfolio strategy indicated as yield curve flattens

In a note to clients earlier this year, we made the case that interest rates would move modestly higher in 2017. Our expectations have proven correct on the short end of the yield curve, although yields on the long end have been lower year-to-date. Bonds have performed well as the market lowered the odds of meaningful fiscal stimulus, a key driver in expectations for faster GDP growth and higher rates.

Nevertheless, the economy has remained stable and growth shows signs of accelerating. With inflation expected to edge higher, unemployment heading even lower, and tax cuts still on the table, we are expecting yields across the curve to edge higher as well.

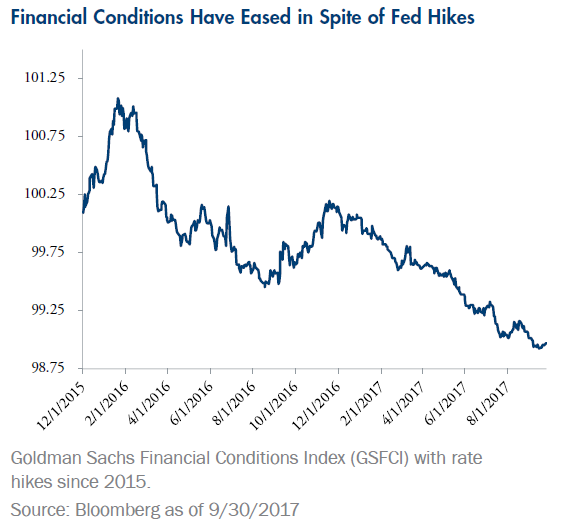

Although the market is now pricing in a greater than 50% probability of another interest rate increase in December, we think the Fed is more likely to delay due to continued softness in inflation and disruption in the economic data from the two hurricanes that made landfall in August and September. Risks to this forecast lie in the recent hawkish shift of the FOMC and the easing of financial conditions in spite of Fed rate hikes (see chart).

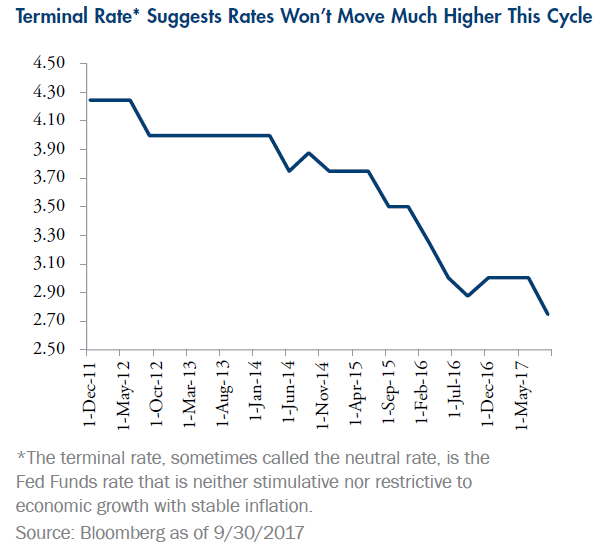

The exact timing of the next increase is less important to financial markets than the Fed’s forecast for the Fed Funds rate at the end of this hiking cycle. This “terminal rate,” sometimes called the neutral rate, has migrated lower throughout the current expansion and reset another quarter-point lower, to 2.75%, at the FOMC meeting in September (see chart). The neutral rate is the Fed Funds rate that is neither stimulative nor restrictive to economic growth with stable inflation.

What does this mean for investors? Even though the Fed is expected to continue tightening monetary policy and raising short-term rates, longer-term rates are likely to be contained. This suggests that a barbell strategy – investing in long and short duration bonds but underweighting intermediate duration issues – is still preferred so as to take advantage of the flattening yield curve. We also may see longer duration assets surprise with continued solid performance.

Important Disclosures

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. This presentation is not an offer to buy or sell, or a solicitation of any offer to buy or sell, any of the securities mentioned herein.

Certain statements contained herein may constitute projections, forecasts, and other forward-looking statements, which do not reflect actual results and are based primarily upon a hypothetical set of assumptions applied to certain historical financial information. Certain information has been provided by third-party sources, and, although believed to be reliable, it has not been independently verified, and its accuracy or completeness cannot be guaranteed.

Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this document and are subject to change.

There are inherent risks with equity investing. These risks include, but are not limited to, stock market, manager, or investment style. Stock markets tend to move in cycles, with periods of rising prices and periods of falling prices. Investing in international markets carries risks such as currency fluctuation, regulatory risks, and economic and political instability. Emerging markets involve heightened risks related to the same factors, as well as increased volatility, lower trading volume, and less liquidity. Emerging markets can have greater custodial and operational risks and less developed legal and accounting systems than developed markets.

Concentrating assets in the real estate sector or REITs may disproportionately subject a portfolio to the risks of that industry, including the loss of value because of adverse developments affecting the real estate industry and real property values. Investments in REITs may be subject to increased price volatility and liquidity risk; concentration risk is high.

Investments in Master Limited Partnerships (MLP) are susceptible to concentration risk, illiquidity, exposure to potential volatility, tax reporting complexity, fiscal policy, and market risk. Investors in MLPs are subject to increased tax reporting requirements. MLP investors typically receive a complicated schedule K-1 form rather than Form 1099. MLPs may not be appropriate investments for tax-advantaged accounts because of potential negative tax consequences (Unrelated Business Income Tax).

There are inherent risks with fixed-income investing. These risks may include interest rate, call, credit, market, inflation, government policy, liquidity, or junk bond. When interest rates rise, bond prices fall. This risk is heightened with investments in longer-duration fixed-income securities and during periods when prevailing interest rates are low or negative. The yields and market values of municipal securities may be more affected by changes in tax rates and policies than similar income-bearing taxable securities. Certain investors’ incomes may be subject to the Federal Alternative Minimum Tax (AMT), and taxable gains are also possible. Investments in below-investment-grade debt securities, which are usually called “high yield” or “junk bonds,” are typically in weaker financial health and such securities can be harder to value and sell, and their prices can be more volatile than more highly rated securities. While these securities generally have higher rates of interest, they also involve greater risk of default than do securities of a higher-quality rating.

Investments in emerging market bonds may be substantially more volatile, and substantially less liquid, than the bonds of governments, government agencies, and government-owned corporations located in more developed foreign markets. Emerging market bonds can have greater custodial and operational risks and less developed legal and accounting systems than developed markets.

As with any investment strategy, there is no guarantee that investment objectives will be met, and investors may lose money. Returns include the reinvestment of interest and dividends. Investing involves risk, including the loss of principal. Diversification may not protect against market loss or risk. Past performance is no guarantee of future performance.

Index Definitions

The Conference Board Leading Economic Index is an American economic leading indicator intended to forecast future economic activity. It is calculated by The Conference Board, a nongovernmental organization, which determines the value of the index from the values of ten key variables.

The Goldman Sachs Financial Conditions Index (GSFCI) is a weighted sum of a short-term bond yield, a long-term corporate yield, the exchange rate, and a stock market variable.

The Standard & Poor’s (S&P) 500 Index represents 500 large U.S. companies. The comparative market index is not directly investable and is not adjusted to reflect expenses that the SEC requires to be reflected in the fund’s performance.

Indices are unmanaged, and one cannot invest directly in an index. Index returns do not reflect a deduction for fees or expenses.

© City National Rochdale Investment Management