Third Quarter 2017 Market Review – Climbing The Wall of Worry

The third quarter of 2017 was highlighted by unfavorable seasonal effects and a steady stream of nerve wracking geopolitical developments, but despite a challenging environment world equity markets persistently fought off short-term jitters and closed out the quarter solidly in the green. Commodities markets also bounced back in the third quarter, and fixed income found a way to post positive returns as investors continued to demonstrate an appetite for both credit related yield and safe-haven plays to hedge portfolio risks.

Those who stayed invested during the third quarter were amply rewarded for doing so, but as markets climbed higher the risks of an overvalued market rose in tandem. With the fourth quarter looming, investors must decide if they should remain fully invested, or start to pull back after the unusually strong run this year.

Plenty to Worry About

Bull markets climb a wall of worry, and the current market run since February 2016 is no exception. In the U.S., the business cycle is now the third longest on record, which is leading investors to naturally question how long this expansion can persist. The Federal Reserve is slowly raising interest rates and some are beginning to wonder whether the economy is strong enough to withstand additional monetary tightening given that growth rates are still low and inflation seems non-existent after years of easy monetary policy. Geopolitical news flow has kept investors on edge all year given ongoing investigations into the Russian involvement in the U.S. election, constant infighting within the GOP, and intermittent saber rattling between the U.S. and North Korea. Severe hurricanes, poor seasonality, and ultra-low volatility in markets also served to heighten anxiety over the most recent quarter.

Within a sea of worries, perhaps the most fundamentally driven concern today is that stocks appear to be significantly overvalued from a broad index perspective. Valuation is often a terrible timing indicator, but has tended to be a very good predictor of longer-term market returns, so investors are right to wonder if the index driven bull market that has performed so brilliantly is poised to leave investors disappointed when looking out over the next five to ten years.

Scaling the Wall of Worry on Synchronized Cyclical Strength

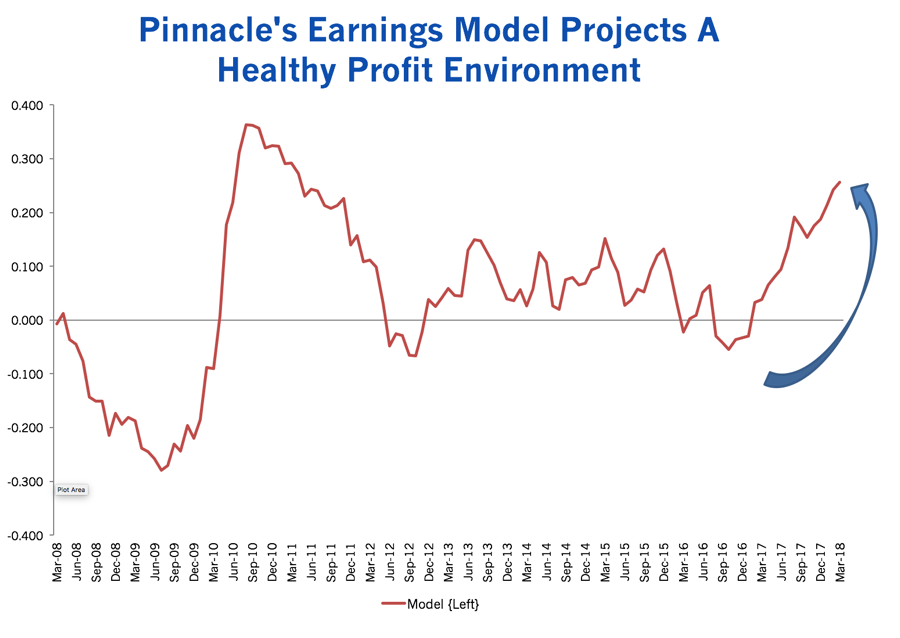

Despite numerous risks to the market, the good news is that there are some solid reasons to believe that the cyclical bull market is not ready to awaken the hibernating bear just yet. Perhaps the most encouraging reason is that the macro fundamentals have been firming, and for the first time in many years it appears that the global business cycle is in the midst of a synchronized upswing. In the U.S., the chronological age of the cycle is well advanced by normal standards, but at the same time, the low trajectory of growth in recent years means that the typical late cycle pressures that usually conspire to topple economic expansions have not yet materialized. Additionally, credit and financial conditions have been supportive and the rest of the world has firmed and is pushing growth in an upward direction (rather than dragging it down). In 2017, Europe, Japan, and many emerging market economies have enjoyed improving growth profiles all year, which has created a positive global feedback loop that is helping to support the aging U.S. expansion. The overall improvement in world growth fundamentals has also been accompanied by dormant inflation across the globe, which is allowing businesses worldwide to benefit from some improvements to top line growth without a commensurate hit to the bottom line that is usually associated with rising cost pressures.

The stable and improving growth profile combined with contained inflationary pressures has created a short-term goldilocks scenario for the profit cycle, which has fundamentally underpinned the rise in equity prices around much of the world. While some discount the latest move in stocks as nothing more than a bubble based on hope and hype, in our view there are plenty of sound fundamental reasons that are helping this cyclical bull market march on.

Furthermore, there are other reasons to continue to be cyclically constructive on markets. The possibility of tax reform/cuts in the U.S. is picking up, and if legislation passes and strongly resembles what has been initially proposed, that could be a game changer for many businesses that would see an immediate increase in after-tax profits. Despite poor valuation at the index level, we also feel there are still specific sectors and industries—and select countries globally—that still offer attractive relative value. Since our investment process provides the flexibility to seek out value where we find it across the globe, we believe there is still ample opportunity to enjoy this bull market while the fundamental backdrop supports being a participant.