Rick Rieder and Russ Brownback argue that while cramming for finals may have worked in college, it won’t with the winding down of the global central bank policy liquidity “semester.”

With autumn well underway, who doesn’t feel a nostalgic pining for the good old days of collegiate life? Crisp colorful afternoons, football games, fall festivals and, oh yeah, looming final exams and papers. For us there were one or two occasions where despite plenty of forewarning about the necessary rigor required for finals, we waited until the last minute to even begin the process. Sleepless, and caffeine-fueled, nights in the library, complete with ongoing panic attacks and sharply decreased odds of maximizing our GPA were the unsatisfactory result. On those few occasions, at best we endeavored to survive with a “gentleman’s C”. At worst? Well, let’s not even think about that.

With the benefit of hindsight it is glaringly obvious that delayed preparation was a dubious choice, with very little upside and the ultimate downside. Eventually, we learned to layer in the protection that proper preparation afforded. We find this a useful (if painful) recollection to put to use today: The “semester” of G3 (the Federal Reserve, European Central Bank and Bank of Japan) policy liquidity is winding down, and we are not waiting until the last minute to prepare.

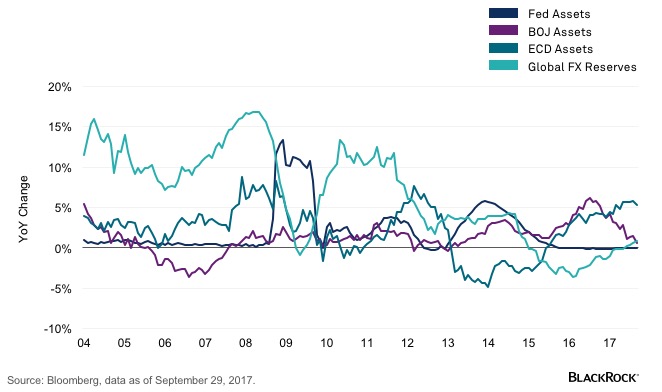

The coming months will likely usher in the first-ever contemporaneous draining of G3 policy liquidity, but we feel increasingly comfortable with the notion that an acceleration of real economy, growth-driven liquidity can provide a very timely substitute (see graph below). While there is no doubt that this regime change comes with a wider range of uncertainty relative to recent quarters, we are confident that expected monetary tightening will be well advertised and deliberate. Moreover, we are convinced that early stage acceleration of real economy velocity will ultimately take over from policy liquidity to facilitate more traditional credit growth through channels such as commercial and industrial loans, consumer credit, and real estate lending.

G3 Central Bank Policy Liquidity Set to Slowly Decline, But Growth-Driven Sources May Fill That Gap

We are highly impressed with the depth and breadth of the current global growth paradigm, and we’re certain that it’s this momentum that has given G3 policymakers the requisite confidence to begin to address the easy financial conditions that have been such a dominant theme during 2017. To be sure, global policy liquidity has played the lead role in pushing asset prices to new highs, with strong correlations across both risk-free and risky assets.

Considering these dynamics, we find duration (a measure of interest-rate risk) to be somewhat more concerning today than in recent memory and the prospects for risky assets will vary depending on how future duration moves are divided between breakevens and real rates. Our expectation is that gradually higher levels of inflation breakevens will result from firmer inflation data in the coming months, while a move higher in real rates will be virtuously tied to cyclical changes in real growth. So we like owning assets with the highest convexity to inflation, with an additional layer of expressions that will benefit from benign moves higher in real rates.

As always, we debate potential “tail risks” associated with our views. Accordingly, the change in central bank mentality provides reason to consider whether the supply/demand imbalance for yielding assets that we have talked about for years now faces an existential threat. While we think that risk is likely to be low, we will be on alert for the possibility that the powerful technical of central bank-driven demand flips to central bank-driven supply. If accompanied by a surprisingly large fiscal stimulus, this change could create a more challenging environment for bond investors. Other left-tail risks to our view include geopolitical disruptions, possible U.S. dollar strength or a complete breakdown in NAFTA negotiations that could dampen near-term sentiment for emerging markets (EM) assets. The right-tail risk is the possibility that the current bullish environment has more horsepower and stamina than we’re forecasting, which could push valuations to even greater extremes.

New disruptive forces will likely cap significant inflation acceleration

Finally, as always, we continue to hold a deep core belief in following cash flows to find opportunities in a world of continual disruption (much of it technologically or demographically inspired) and stronger global growth. Over the past several months, we have catalogued the incredible disruption taking place across a wide array of industries. We expect much more of this to come, and we are blown away by how fast these trends are ripping into the fabric of economy-wide and industry-specific frameworks. While we anticipate that some of these deflationary influences could level off, there are emerging new disruptive forces that will likely cap significant inflation acceleration. The question is which industries will be impacted and at what pace.

We’re preparing for modestly higher developed market rates

We’re preparing for modestly higher developed market (DM) rates and choose to express duration through Treasuries over German Bunds or Japanese Government Bonds. Stronger inflation data over comings months will be the main catalyst for rising DM rates, so breakevens are a convex expression of this theme. We’re positioned in U.S. credit, as it offers more spread-per-unit-of-leverage than sovereign DM alternatives, and with volatility so low, upside equity convexity remains very attractively priced in our view. We continue to like EM, as benign leverage, calming inflation and relatively attractive real yields in selected local rates markets are compelling opportunities. Ultimately, we think the autumn 2017 semester of policy liquidity is getting long in the tooth. School spirit revelry and other amusing diversions are ever present, but we’ve learned from our youthful errors and we’re studying hard for final exams. Our straight A’s will have come in the form of building a portfolio around high-quality and predictable carry, coupled with assets defined by attractive price characteristics. We hope to provide a “stellar report card” for our clients.

Rick Rieder, Managing Director, is BlackRock’s Chief Investment Officer of Global Fixed Income and is a regular contributor to The Blog. Russell Brownback, Managing Director, is a member of the Corporate Credit Group within BlackRock Fundamental Fixed Income and contributed to this post.

Investing involves risks including possible loss of principal.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of October 2017 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

©2017 BlackRock, Inc. All rights reserved. BLACKROCK is a registered trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

287099

© BlackRock

Read more commentaries by BlackRock