The Bank of England (BoE) has bitten the bullet and hiked the base interest rate from 0.25% to 0.5%, but in a dovish turn also provided forward guidance that outlines a very gradual path for future hikes. This was a close call with compelling arguments in favor and against. We are in the against camp and looking ahead, we expect the BoE will have to stand down. We expect that a one-and-done rate hike against such a dovish forward guidance background will only briefly impact markets, pushing down gilt yields and the pound and supporting equities.

Arguments in favor of the rise

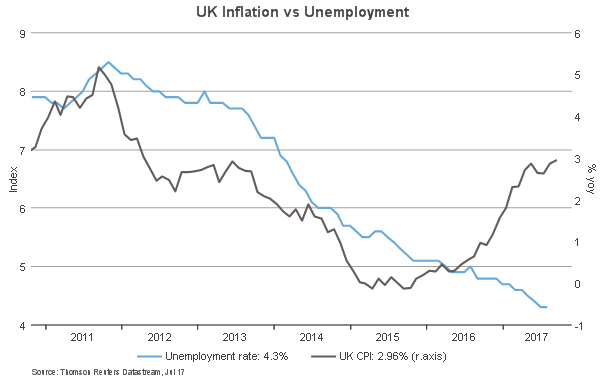

The arguments in favor of the interest rate hike start with the rise in inflation to 3% year-on-year. This is putting pressure on the BoE to tighten monetary policy. However, because the rise in inflation is mainly caused by a fall in the pound, it is not the main reason. After all, the inflationary impact of a lower pound is transitory and will slowly dissipate in 2018. More important for the BoE is the tight labor market. The unemployment rate is at its lowest level since 1975 and the BoE worries this will drive future wage growth up. Finally, economic growth in the UK has held up better than expected since the Brexit vote. This undermines the case behind the BoE’s emergency measures, including its rate cut at the time.

Arguments against the rise

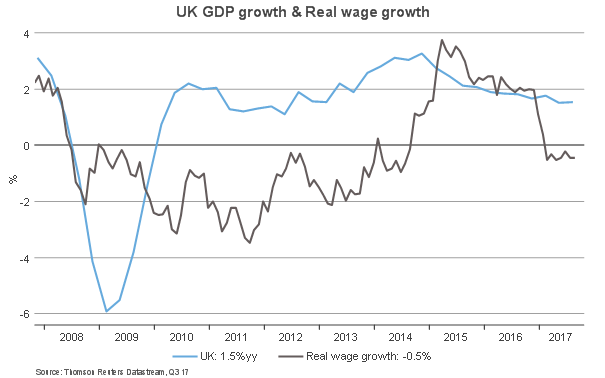

Although the arguments in favor are compelling, we are of the opinion that the arguments against are more so. As stated before, concerns around inflation need to be tempered considering the transitory impact of a weaker pound. And although wage growth might indeed pick up in the future, as of late it has been rather sluggish. In fact, in real terms wage growth has dipped into negative territory, putting pressure on UK consumers. And because the consumer has been the engine of economic growth since the Brexit vote, it follows that risks to the economy are tilted to the downside. In an environment where economic growth is already slowing down notably and the important housing market is wobbly, we disagree with the BoE decision to add to those risks.

But risks are not just emanating from the UK consumer and housing. Political risk is also on the rise. The Brexit negotiations are not going well and Prime Minister Theresa May’s position is rather weak. The uncertainty this brings is weighing on producer confidence and will deepen the economic slowdown.

Given these circumstances, we expect the BoE will stand down over the next twelve months and leave interest rates unchanged. In fact, the BoE itself has already indicated as much in its very dovish forward guidance. And because this dovish surprise is more market relevant, the reaction today has been one of lower Gilt yields, a lower pound and rising equities. We don’t expect these moves to last long, and in case they do, we will use it as a trading opportunity in the opposite direction.

Investor impact

We asked our investment experts based in EMEA for their thoughts about how the hike will impact investors both locally and afar.

Spotlight on consumption and housing from CIO Gerard Fitzpatrick

“Once central banks start moving in a certain direction, they seldom fully stop. We believe this rate hike will be moderately negative to the UK’s economic outlook, especially to the consumption and housing sectors, and this could become a headwind factor for UK equities.”

Spotlight on pension funds from David Rae, Managing Director of Client Strategy and Research

“Base rate changes almost always precipitate a rash of questions about the optimal liability hedging position and whether a fundamental review of policy is required. The reality is that today’s decision will have a very limited impact on liability valuations. The big question remains whether the Bank of England and other central banks are able to successfully avoid a policy error that destabilizes economic growth. The focus should remain on the risks within the asset portfolio and the risks associated with any potential economic slowdown.”

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page.

Investing involves risk and principal loss is possible.

Past performance does not guarantee future performance.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

This material is not an offer, solicitation or recommendation to purchase any security. Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type.

The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional. The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Please remember that all investments carry some level of risk. Although steps can be taken to help reduce risk it cannot be completely removed. They do no not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Investments that are allocated across multiple types of securities may be exposed to a variety of risks based on the asset classes, investment styles, market sectors, and size of companies preferred by the investment managers. Investors should consider how the combined risks impact their total investment portfolio and understand that different risks can lead to varying financial consequences, including loss of principal. Please see a prospectus for further details.

Indexes are unmanaged and cannot be invested in directly.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments' management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

Copyright © Russell Investments Group LLC 2017. All rights reserved.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

UNI-11162