The lack of wage growth in the U.S. labor market has been a frequent topic during our global multi-asset investment calls. Typically at this point in the economic cycle (mid-to-late cycle), wages are growing at a 4%+ pace. However, wage growth has been very modest over the past few years (2%-3% growth), puzzling many investors and frustrating many workers who have expected larger increases. This has also been a significant puzzle to the Federal Reserve, with Chair Janet Yellen calling the recent low levels of inflation (including wage growth) a “quandry.” Adding to the uncertainty in recent months has been the impact of hurricanes on U.S. economic data.

So will wages finally show some stronger upward pressure or are there structural factors at work that will continue to exert downward pressure? In the below, we argue that: a) wages are growing more strongly than many realize and b) there are some compelling reasons why wage growth in this cycle has been lower than past experience.

It All Depends What You’re Looking At

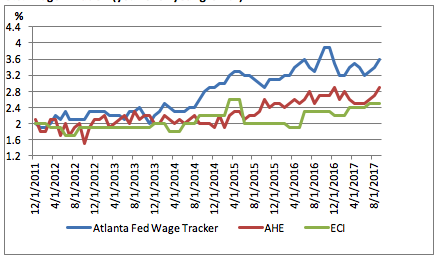

There are many different measures of wage inflation in the U.S. Average Hourly Earnings (AHE) receives the most headlines and measure average wages per worker in the economy in one period compared with an earlier period. While easy to understand, it has a number of weaknesses including its inability to account for changes in the composition of jobs or changes in the composition of labor force. Another measure is the Employment Cost Index (ECI). The ECI has the advantage that it holds the composition of jobs constant. It is designed to calculate the change in total cost of compensation, including not only wages and salaries (70% of index) but also benefits (30% of index). Finally, there is the Atlanta Fed Wage Tracker, which focuses on the continuously employed and therefore has bias toward older, more educated workers. It is this measure that has shown the strongest reading of wage growth over the past few years.

U.S. Wage Inflation (year-over-year growth)

Sources: Federal Reserve Bank of Atlanta, Bureau of Labor Statistics, BMO Global Asset Management

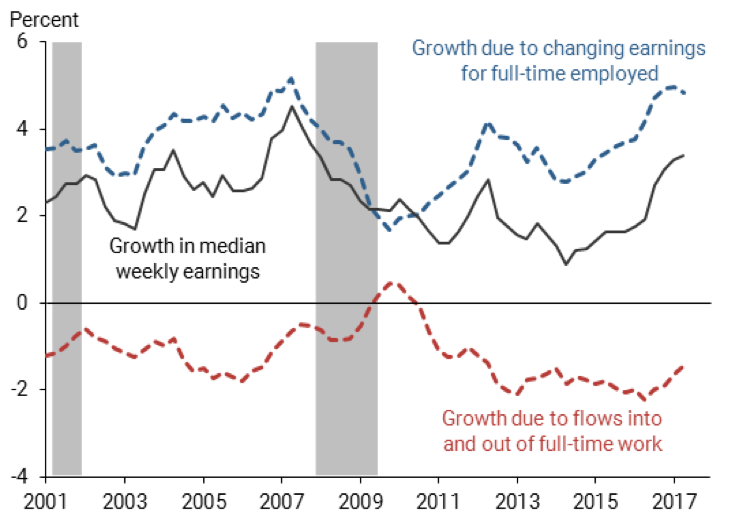

So what explains the differences in wage inflation measures? Changes in the workforce due to demographics are partially at work here. New workers entering the work force (i.e. Millenials) may have lower wages than existing workers (i.e. Baby Boomers). The San Francisco Fed has done quite a bit of research on this topic and has concluded that these so called “composition effects” (the red line in the chart below) have reduced wage growth by 2% per year in recent years.

Median weekly earnings growth, overall and by full-time status

Source: Federal Reserve Bank of San Francisco

There are many other plausible theories of why wage inflation has not been stronger in recent years. These include: globalization exerting downward pressure on wages, an economy that has transitioned away from highly productive manufacturing towards lower productivity services jobs, the impact of a strengthening U.S dollar and inflation expectations (inflation has been low, so employers and workers extrapolate this trend). We feel that all of these factors have merit, though it is difficult to measure the precise impact of each one.

Concluding Thoughts:

Wage growth and the broader inflation outlook in general will be a key area of focus for us in the coming months, given its impact on the reaction function of central banks as well as risk assets. As we expect global growth to continue to broaden out, our bias is for inflation to pick up modestly. This is part of the rationale for our underweight stance to US core fixed income relative to an overweight to global equities.

Unless otherwise noted, all data is as of the date of publication. You should consider the Fund’s investment objectives, risks, charges and expenses carefully before investing. For a prospectus, which contains this and other information about the BMO Funds, call 1-800-236-3863. Please read it carefully before investing.

BMO Asset Management Corp. is the investment adviser to the BMO Funds. BMO Investment Distributors, LLC is the distributor for the BMO Funds. Member FINRA/SIPC. BMO Funds are not marketed or sold outside of the United States.

This is not intended to serve as a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect our judgment at this date and are subject to change. Information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy. This presentation may contain forward-looking statements. “Forward-looking statements,” can be identified by the use of forward-looking terminology such as “may”, “should”, “expect”, “anticipate”, “outlook”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof, or variations thereon, or other comparable terminology. Investors are cautioned not to place undue reliance on such statements, as actual results could differ materially due to various risks and uncertainties. This publication is prepared for general information only. This material does not constitute investment advice and is not intended as an endorsement of any specific investment. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors should seek advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investment involves risk. Market conditions and trends will fluctuate. The value of an investment as well as income associated with investments may rise or fall. Accordingly, investors may receive back less than originally invested.

Past performance is not necessarily a guide to future performance.

BMO Global Asset Management is the brand name for various affiliated entities of BMO Financial Group that provide investment management and trust and custody services. Certain of the products and services offered under the brand name BMO Global Asset Management are designed specifically for various categories of investors in a number of different countries and regions and may not be available to all investors. Products and services are only offered to such investors in those countries and regions in accordance with applicable laws and regulations. BMO Financial Group is a service mark of Bank of Montreal (BMO).

BMO Asset Management Corp., BMO Investment Distributors, LLC, BMO Private Bank, BMO Harris Bank N.A. and BMO Harris Financial Advisors, Inc. are affiliated companies. BMO Private Bank is a brand name used in the United States by BMO Harris Bank N.A. BMO Harris Financial Advisors, Inc. is a member FINRA/SIPC, an SEC registered investment adviser and offers advisory services and insurance products. Not all products and services are available in every state and/or location.

All investments involve risk, including the possible loss of principal.

Securities, investment advisory and insurance products are: Not FDIC Insured – No Bank Guarantee – May Lose Value.

© BMO Financial Corp. (6287347, 11/17)