State of the world

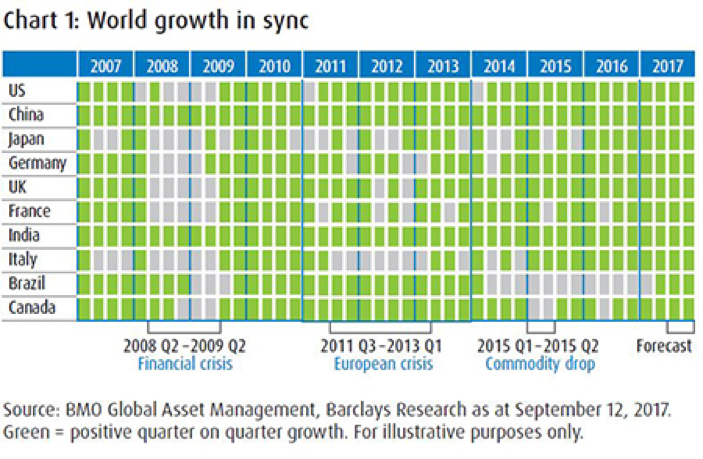

The world economy has reached an unusual state of stability. Almost every country is seeing positive growth – shown as a green square in Chart 1 – but nowhere is growth booming out of control. Inflation is also firmly in ‘goldilocks’ territory.

Goldilocks rules

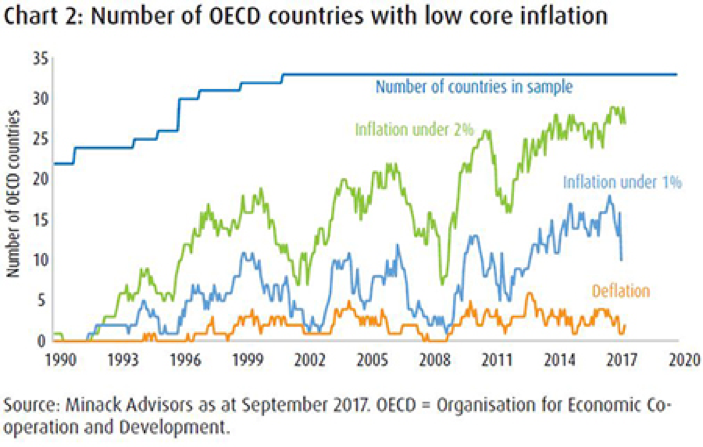

With the exception of those countries, such as the UK, which have suffered significant currency weakness, inflation is low throughout the world but the number of countries in or close to deflation is low and falling. Inflation, like growth, is neither too hot nor too cold. In addition, there are few financial imbalances within or between the major economies. Geopolitics remains a worry but the immediate economic threats to the world economy are few and far between.

What does this environment mean for investors? Analysis of similar scenarios over the last 50 years suggests that a ‘Goldilocks’ backdrop favors risk-on investing, particularly in equities. Bonds, both government and corporate alike, typically fare less well. However, there are always risks in projecting past performance trends forward.

Currently, the rate of expansion in the U.S. stands at around 2%, but longer term, there’s an argument that secular themes could depress growth to around 1.5%. First, technology-related gains in productivity are moderating. Second, lower birth rates are combining with an aging demographic to reduce the size of the working population.

Regional perspectives

We are now well into the Trump presidency and he has found the process of transferring his pre-election rhetoric into policy reality to be a challenging task. Tax cuts were among his commitments and they remain firmly on the agenda. The likelihood of tax reform has increased in recent months, but if a bill is eventually passed, the size and scope of it may look underwhelming after it has made its way through Congress.

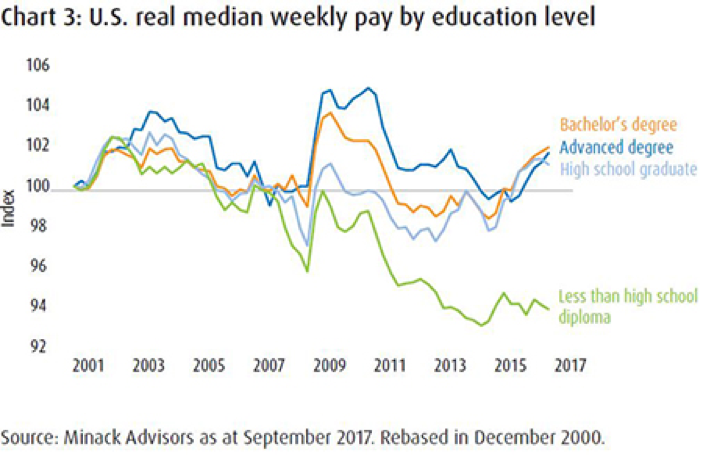

Of course, cutting corporate taxes may have positive economic implications down the road but they don’t fundamentally tackle the challenge faced by a sizable section of the U.S. population – a segment to which Trump owes much of his support. As shown in Chart 3, those who failed to graduate from high school have experienced a significant fall in real incomes over the last decade. The causes of this wage stagnation are numerous – outsourcing due to globalization, technological changes in manufacturing, transition to a services economy, just to name a few – and the solutions are broadly long-term structural changes rather than short-term fixes.

Overall, the U.S. economy is in reasonable shape and inflation remains relatively subdued, particularly as rents – which comprise over a third of the core consumer price index – have stabilized. This, combined with gently rising wages, means that the Federal Reserve is likely to continue to gradually raise interest rates. This is a headwind for markets but for our central scenario, where inflation pressures are moderate, it is more of a gentle breeze than a disruptive gale.

China has its challenges: the trend growth rate is slowing and credit growth is excessive, as we discuss in our central scenario. Yet persistent forecasts of a hard landing have not materialized and China looks set to ‘muddle through’.

Even in a world of synchronized growth, the improvement in Europe’s economies stands out. The reasons behind the upturn are self-evident. The era of fiscal austerity in Europe is over and this, alongside massive monetary expansion, is feeding through into a sustained economic upswing. Italy’s election next spring and key wage negotiations in Germany loom on the horizon but we do not foresee either derailing Europe’s cyclical upturn.

There is, of course, one notable outlier in Europe – and that’s the UK. Negotiations around its withdrawal from the European Union (EU) are proving difficult and whatever the outcome, the country faces a challenging period of readjustment to life outside the single market. More immediately, the pound is still weak but to date it hasn’t done much to enhance the UK’s trading position. It has, however, reduced real incomes and squeezed consumption investment. Ironically, the UK is benefiting from the strength of the eurozone economy and its proximity to it! In fact, without Europe’s recent pick-up, it is likely that the UK would be flirting with recession.

Investments cannot be made in an index.

This presentation may contain targeted returns and forward-looking statements. “Forward-looking statements,” can be identified by the use of forward-looking terminology such as “may,” “should,” “expect,” “anticipate,” “outlook,” “project,” “estimate,” “intend,” “continue” or “believe” or the negatives thereof, or variations thereon, or other comparable terminology. Investors are cautioned not to place undue reliance on such returns and statements, as actual returns and results could differ materially due to various risks and uncertainties. This material does not constitute investment advice. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors should seek advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investment involves risk. Market conditions and trends will fluctuate. The value of an investment as well as income associated with investments may rise or fall. Accordingly, investors may receive back less than originally invested.

The analysis and views expressed in this report reflect personal views about the subject and not related to any specific recommendations. The information and statistics in this report have been obtained from sources we believe are reliable but we do not warrant their accuracy or completeness. We do not undertake to advise the reader as to changes of our views in the future. This is not a solicitation of an order to buy or sell any specific securities.

Foreign investing involves special risks due to factors such as increased volatility, currency fluctuation and political uncertainties.

Investing in alternative investments presents the opportunity for significant losses, including the possible loss of your total investment. Such strategies have the potential for heightened volatility and in general, are not suitable for all investors.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. All of these factors can subject the funds to increased loss of principal.

Past performance is not necessarily a guide to future performance. BMO Global Asset Management is the brand name for various affiliated entities of BMO Financial Group that provide investment management and trust and custody services. Certain of the products and services offered under the brand name BMO Global Asset Management are designed specifically for various categories of investors in a number of different countries and regions and may not be available to all investors. Products and services are only offered to such investors in those countries and regions in accordance with applicable laws and regulations. BMO Financial Group is a service mark of Bank of Montreal (BMO). BMO Asset Management Corp., BMO Investment Distributors, LLC, BMO Private Bank, BMO Harris Bank N.A. and BMO Harris Financial Advisors, Inc. are affiliated companies. BMO Private Bank is a brand name used in the United States by BMO Harris Bank N.A. The information provided herein does not constitute a solicitation of an offer to buy, or an offer to sell securities nor should the information be relied upon as investment advice.

Investment products are: NOT FDIC INSURED — NOT BANK GUARANTEED — MAY LOSE VALUE.

© 2017 BMO Financial Corp. (6281062, 11/17)

U.S. version – 11/17