GMO Quarterly Letter

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWhat Happened to Inflation?

And What Happens If It Comes Back?

Ben Inker

A year ago, the US economy seemed poised for a significant shift. On one hand, inflation was running at the Fed’s target level, unemployment hovered around most estimates of full employment, and a new president was coming in promising a fiscal boost and policies designed to increase economic growth. On the other hand, after close to a decade of doing everything it could to boost the economy, the Federal Reserve was promising to, if not take away the punchbowl, at least begin diluting the alcohol content. Something looked likely to give, in a way that would give us a significant clue as to whether interest rates would ever be able to go back to the levels that we all used to think of as normal. The year has actually turned out to be more confusing than expected, playing out in a way that did not align with either of our scenarios. This leaves us with continued uncertainty about where interest rates will wind up. But it also leaves me, at least, increasingly convinced that a significant inflation shock would be just about the worst thing that could happen to today’s investment portfolios. Unlike most of history, it seems plausible that a meaningful inflation increase from here would impose worse losses on portfolios than a depression would. Depressions are bad for risk assets and good for high quality bonds. Inflation is very bad for high quality bonds and modestly bad for stocks. Today, not only would bonds do particularly badly given their very low real yields, but stocks could get hit worse than you’d otherwise expect given their high valuations. The saving grace from inflation-driven losses is that they would primarily come from a fall in valuations, not impairments to future cash flows. As a result, we wouldn’t be all that much poorer if we judge by the amount of future spending a portfolio could sustainably support. But the loss of paper wealth could be massive. This doesn’t mean such an inflation surge is inevitable, or even particularly probable. It is, however, something that investors should have in the forefront of their minds when they think about what could go wrong for their portfolios.

What have we learned about Purgatory and Hell?

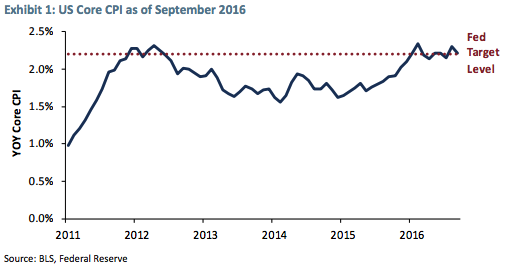

I believed that we were going to learn a good deal about the probabilities of Purgatory and Hell because the recovery from the financial crisis seemed to finally be over. The US economy was around full employment, inflation was at the Federal Reserve’s preferred level, and the Fed was preparing to embark on a significant tightening cycle for the first time in over a decade. In the years when the economy was still stumbling through its slow recovery from the crisis, it was hard to really get a good feel for how close the economy was to its potential and how quickly inflation would return once spare capacity had been used up. But with the unemployment rate below 5% and inflation creeping up, it seemed we had worked our way through the lingering effects of the crisis. Exhibit 1 shows the core CPI as of the end of 2016, against an estimate of the Fed’s target level.1

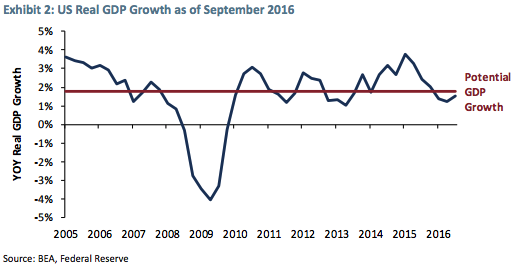

After a long period of lower than target inflation, we seemed to be getting back on track. Similarly, GDP growth seemed to be in line with target levels, although perhaps trending a little soft versus the Fed’s estimate of potential GDP, as we can see in Exhibit 2.

We had been running slightly under the Fed’s 1.8% estimate of potential GDP growth. For a secular stagnationist, this could have been seen as evidence that the economy was beginning to soften again, presaging a dip into recession if the Federal Reserve were to go ahead with its plan to raise rates.

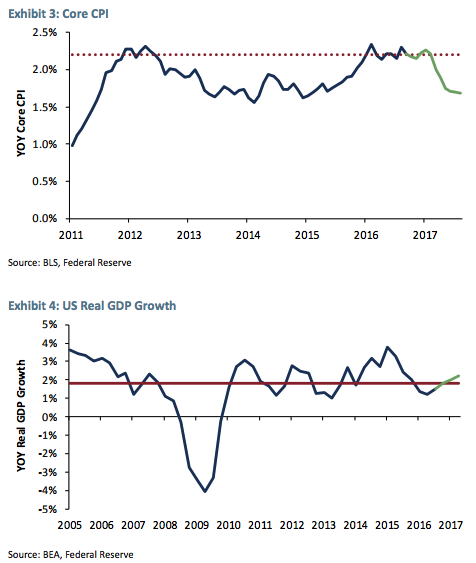

Once you threw in the election and promises by the Trump administration for a large fiscal stimulus, it really did seem like a lot was going to become clearer pretty quickly. Exhibits 3 and 4 show what has happened to core CPI and GDP growth since last fall.

The Federal Reserve did indeed go ahead with its expected rate increases in December, March, and June. GDP growth, rather than soften as might have been expected if secular stagnation were correct, mildly strengthened. On the other hand, we would have expected inflation to either stay the same or rise, given GDP growth of around potential or better. The fall from 2.2% to 1.7% instead is somewhat mysterious.

Under most circumstances we wouldn’t care a lot about changes in inflation of this magnitude. Unless inflation becomes a real problem, we don’t believe that it materially impacts the future real cash flows available from most financial assets, so its impact on fair value is minor. Today, however, it has taken on a more central role in our thinking. When the economy was in recovery mode from the financial crisis, the secular stagnation versus gradual healing scenarios for the economy was a slightly academic argument, as it was hard to determine which was more accurate from the evidence we had. From now on, however, the role of inflation seems utterly crucial to determining if we are in Purgatory or Hell. If, for whatever reason, inflation is permanently quiescent in the modern economy, the rationale for meaningfully higher interest rates is thin. Yes, higher real interest rates would give central banks more ammunition to fight future recessions, but we’ve seen from recent events that the zero bound, which economists assumed put a limit on how easy monetary policy could get, is more porous than we thought. A central bank primarily concerned with keeping inflation on an even keel, let alone one that desires to encourage maximum employment given tame inflation, will tend to keep rates very low as long as it believes that inflation is not a threat. So whether inflation starts to rise again is extremely important for helping us determine whether short-term interest rates ever come back up to the good old days of perhaps 1% to 1.5% above inflation. Rising inflation does not have to mean an inflation problem. If inflation were to push up to 2.5% to 3.0% in response to an economy continuing to grow steadily with low unemployment, this would not come as a shock to economists or the Federal Reserve. It would mean, however, that after a number of years of sub-normal inflation, the traditional rules of the economy still seem to hold and the Fed would have to raise rates at least in line with their current forecasts, or possibly a little higher. This would push up bond rates, and, I believe, push down the general level of P/Es for stocks as well as valuations for real estate, infrastructure, private equity deals, and the like.

I have to admit that this is speculation on my part. Historically, there has not been a strong relationship between interest rates and valuations for real assets, and while inflation has impacted stock market P/Es, the impact has been modest for smaller changes in inflation. Using the model that Jeremy Grantham and I built years ago for explaining the Shiller P/E of the US stock market over time, an increase in inflation to around 2.5% would actually cause the valuation of the stock market to increase, not decrease. When we built the original “Investor Comfort” model in the late 1990s, I solved for the market’s ideal level of inflation. It turned out to be 2.5% – any deviation from that level, whether up or down, caused the market to trade at a lower valuation.

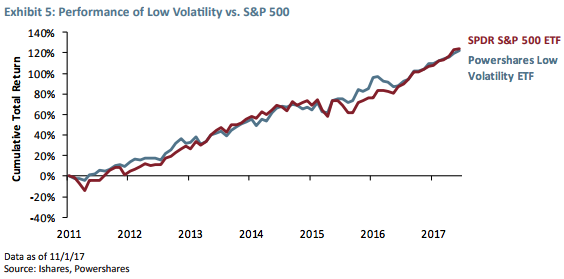

My guess is that this is no longer the case. I’m not sure who coined the term “TINA” stock market, short for “There Is No Alternative,” but it does really feel as if that is a decent description for what is animating today’s stock market. Absent the excitement over the FAANG2 stocks, this seems to be about the least enthusiastic bull market in history. There is no equivalent to the “great moderation” of the mid-2000s when investors seemed to truly believe that recessions were a thing of the past, nor the grand excitement about the internet driving away the clouds of ignorance as Alan Greenspan suggested during the late 1990s bull market. Apart from the FAANGs, there appears to be a sense that we all have to be invested in something and bonds and cash at current yields are more or less unownable. The strong performance in recent years of low volatility stocks is consistent with my guess, as they have managed to keep up with S&P 500 despite the fact that they are neither exciting nor growthy, and have quite a low beta. They are, in short, exactly the type of group of stocks that should be expected to underperform in a bull market driven by excitement for the future or even a nice cyclical recovery. Their performance is shown in Exhibit 5.

To be clear, this is in no way a recommendation for this ETF or low volatility portfolios in general. Low volatility stocks look relatively expensive to us – significantly pricier versus the market than they were on average during the decades before low volatility became fashionable. My point is simply that this is not a group that would be expected to keep up in an excitement-driven bull market, but might well hang in in a market driven by investors feeling forced into equities despite a lack of enthusiasm.

Jeremy Grantham looks at this environment and argues that we should be on the lookout for an actual excitement-style bubble to form now, and he may well be right. But the flip side is that an event that would not have particularly troubled an excitement-driven bull market – a modest rise in the expected return on low-risk assets – could have a more significant effect today. The transition from the TINA market to the TIAOA market – “There Is An Okay Alternative” might well be more problematic than our old model suggests.

What happens if there’s an inflation problem?

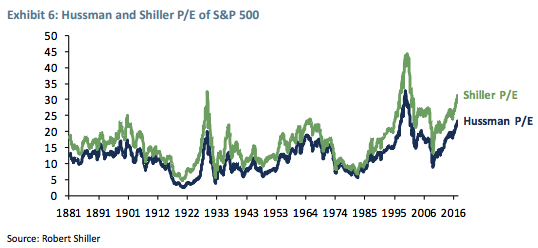

This all happens without an actual inflation “problem.” If inflation were to actually become a problem and head to, say, 4% to 6%, the Federal Reserve would have to raise rates much more aggressively. While such an event would be devastating to bonds under any circumstances and would be normally expected to hit stocks moderately as well, the potential pain today seems significantly greater. We then go from the TINA market to the TIAPDGA market as well as the DKAMATEAITID market – the “There Is A Pretty Darn Good Alternative” market and the “Don’t Know As Much About The Economy As I Thought I Did” market.3 The combination of bonds and cash suddenly yielding quite a bit in both nominal and real terms as well as much higher uncertainty about the future path of the economy seems likely to be utterly devastating to today’s high valuations. One simple way of thinking about that is asking what would be the fall in the S&P 500 if valuations were to fall to long-term median levels. Our favorite simple measure of value is Shiller P/E, but for those concerned about a “false” impact on valuations from the write-downs in the financial crisis, we can also look at the “Hussman P/E,” which compares real stock prices to the highest historical real earnings of the index (Exhibit 6).4

Relative to traditional P/Es, Shiller P/E is biased high because earnings tend to grow over time and a 10-year average earnings figure will be, on average, lower than last year’s earnings. Hussman P/E is biased low, since it is always comparing the market to the highest earnings figure we’ve ever seen. But versus their long-term medians, both are telling precisely the same story – the S&P 500 is trading at about a 93% premium to the long-run median. Falling to median therefore involves a 48% fall.

That long-run median doesn’t feel like it has a lot of relevance these days. In the last 25 years, the S&P has spent somewhere between 6 and 13 months trading at or below the long-term median, depending on which version of normalized P/E you are looking at. That’s between 2% and 4% of the time, which sure doesn’t make it feel like a relevant median any more. Historically, the three things that have dragged the market lower than median have been major wars, economic crises, and inflation spikes. Holding aside the major war category, which I hope is not a meaningful risk even if some days it seems more plausible than I’d like, that leaves us with two categories of events that might blow a hole in your portfolio. Ordinarily, I would consider that of the two remaining, the economic crisis is the worse by a significant margin. It is only in a depression-like scenario that material numbers of companies go bankrupt and investors suffer meaningful permanent dilution.

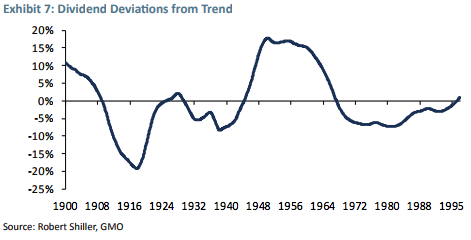

The funny thing is that, from here, dilution may not be the worst thing that can happen to investor brokerage statements. Exhibit 7 shows the 10-year deviations from trend dividends for each year starting in 1900 for the S&P 500. Turns out that the worst thing that ever happened on that measure wasn’t actually the Great Depression, but rather World War I and the depression that followed it.

Even in the worst event, the loss was about 20% of expected dividends over a decade, which isn’t truly catastrophic. It means significantly less than a 20% loss of economic value – maybe 5% to 10% depending on whether you assume there will be a “catch-up” in dividends at some point in the future.

And the positive side of an economic crisis occurring is that we know damn well what central bankers would do in the event. A modern central bank would immediately bring interest rates to zero or below and hold them there for not merely the duration of the crisis but for as long after as circumstances will allow. So let’s imagine the results of an economic crisis. Imagine first that the economic value of the stock market falls by a full 15% – worse than anything we have seen in the US since stock market records began. That knocks the S&P 500 down from 2600 to 2080 before we account for any change in valuation. Let us assume further that the crisis disabuses investors of any notion that stocks aren’t risky, and therefore investors demand a full 4% equity risk premium over cash to compensate. On the flip side, what would investors expect cash rates to be in the future? Given that in the 18 years since the end of 1999, T-Bills have averaged a real yield of -0.6%, let’s be conservative and say that long-term cash estimates would be 0% real. That means the required return to stocks would be 4% real and the Shiller P/E of the market that would be consistent with that is around 23. If we combine the 15% loss of value with the required fall in valuations, we are talking about a market drop to a little over 1600 – although I could argue that it might be somewhat worse than that since the last 10 years really do look like they have been extraordinary from a profits/GDP perspective. Let’s say profits really do go back to their old relationship with GDP. This would knock another 15% off of the market, dropping us to 1360. A very nasty shock to investors, to be sure. On the other hand, this is exactly the kind of scenario that bonds are in your portfolio for. If, at the same time this happened, the yield on US bonds went to the yields we see today in the eurozone, a bond portfolio with equivalent duration to the US Aggregate5 would experience a windfall of 14%. An old fashioned 60% stock/40% bond portfolio would lose somewhere between 18% to 23% from the event.

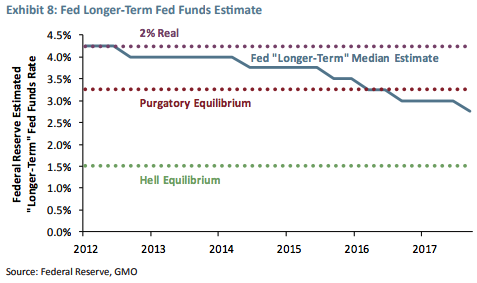

Let’s imagine instead that rather than a depression, we found ourselves with a moderate inflation problem with expected real cash rates moving to 2% real – a level exactly in line with the Fed’s “Dot Plot” as recently as 2012, as we can see in Exhibit 8.

There are three horizontal lines on this chart. The top one is the 2% real line of the “inflation is an issue” scenario, the middle line is our standard “Purgatory” assumption, and the lowest is the “Hell” assumption. As of 2012, the Fed’s official long-term view was in keeping with the 2% real cash, although today they are between Purgatory and Hell in their assumption.

Let’s imagine we get to 2% real cash rates as equilibrium. From a corporate cash flow perspective, the real cost of debt will be significantly higher, so earnings accruing to shareholders will likely drop. Given the pretty high leverage of the market and very low current interest costs, let’s conservatively imagine that sustainable earnings for shareholders fall by 7.5%. This takes the market from 2600 to 2340. The much bigger issue is that if the stock market has to deliver 6% real to give an adequate risk premium over the healthy cash rate, the fair Shiller P/E is probably about 16. The combination of falling earnings and valuations takes the market down to about 1200 on the S&P 500.

At the same time, bonds would be taking it on the chin as well. If the yield on the US Aggregate rose to 7%, which was merely its average yield for the decade of the 1990s, a bond portfolio would be expected to lose around 25%. The 60/40 portfolio that lost 18% to 23% in the depression scenario loses 42% in this one. This is far from a worst-case scenario for inflation. If we imagined something that caused inflation expectations to rise to 5% and real rates to rise to 3%, the fall for the 60/40 portfolio goes to 52%.6 As a reminder, these losses are not to the worst trough level for the market, but the fair value that the stock and bond markets should oscillate around.

Could other assets save you?

Unfortunately, it’s not entirely clear what other assets would save your portfolio in this event. Real estate and infrastructure form a big chunk of investors’ “inflation hedging” portfolios, but it’s hard to see how they help a lot here. While real cash flows from the underlying assets would be expected to keep up with inflation, these assets are usually held in a levered form. Rising real rates would hurt cash flows for holders similarly (or worse) to what we modeled for equities. The big driver of the losses in equities was not cash flow problems but falling valuations, and the same logic applies for these assets as well. Natural resources have a possibly better claim as protectors, as they have the potential for an increase in real cash flows. However, this is really only true in a particular kind of inflation – one that is driven by a spike in resource prices that is greater than that of prices in the rest of the economy. Should such a commodity spike happen, commodity futures have the potential for a windfall7 and resource stocks would certainly hold up much better than other equities. But if resource prices were to rise only in line with other prices, that protection would be minimal.

Okay, but can it happen?

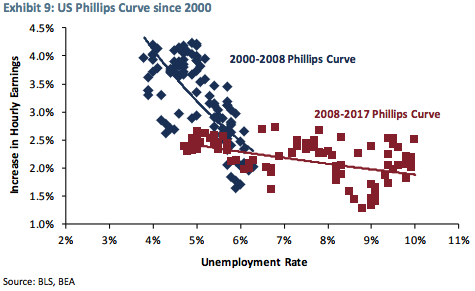

The hypothetical inflation case is a scary one, but inflation is far from people’s minds as a big risk. In the past decade we’ve actually seen two different commodity price spikes that didn’t lead to any significant inflation, and the relationship between unemployment and inflation seems to have gone completely flat. Exhibit 9 shows the relationship between wage growth and unemployment in the US for the periods 2000-2008 and 2008-2017.

Prior to the financial crisis, the relationship between unemployment and wage growth was what economists expect – when unemployment gets low, wages heat up. Since then, the relationship has been much more muted, with 80% less slope than the older relationship. So perhaps something has really changed. On the other hand, 2008 wasn’t all that long ago. Maybe the current situation is temporary and we will go back to the old rules. And maybe the Fed will be slow to catch on to the shift and wind up behind the curve, allowing inflation expectations to rise significantly. Is it my base case? No. But it doesn’t seem like an entirely implausible one, either.

So what can we do?

The basic trouble with the rising inflation environment on investor portfolios is that it hits every asset class with significant duration. Stocks, bonds, real estate, private equity, infrastructure, all should take a hit. And there are few, if any, assets that reliably do well in the event of unanticipated inflation. TIPS outperform traditional bonds, but certainly would lose money. Resource stocks should beat traditional stocks by a large margin if there is a meaningful commodity component to the inflation. But as they are also a long-duration asset, whether they would make money in absolute terms is less clear.

There is on e security that is more or less guaranteed to pay off in the event of unanticipated inflation – an inflation swap. If inflation is higher than expected, such a contract will give a windfall gain, exactly what we’d want to cushion a portfolio. The trouble with buying an inflation swap is that if we imagine a scenario in which inflation surprises significantly to the downside, it is the depression scenario – the other way portfolios get hit pretty hard. So we can reliably protect against the inflation scenario at the cost of almost certainly worsening the depression scenario. That might be the right trade, but it is hardly a lay-up.

In our benchmark-free portfolios, our primary defense against the inflation threat has been shortening the duration of our assets. This is straightforward in fixed income. We own some duration in the form of TIPS, which are at least less acutely vulnerable to inflation than traditional bonds, but most of our fixed income portfolio has a duration of two years or less. In the risky part of the portfolio, we have moved significant amounts of money to liquid alternatives, and I have written at length how we believe liquid alts are a significantly shorter-duration way of taking depression risk than equities.

There is a final, somewhat speculative piece of comfort I take in our equity portfolios. Significant inflation would certainly come as a nasty shock to equity investors in general. But if there is one group of equities that deals with inflation on a pretty much continuous basis, it is emerging equities. Emerging markets usually have a decently high beta in down markets. But it is not so far-fetched to imagine that if the catalyst for the fall were rising inflation, the stock markets where inflation was never absent in the first place might be better able to shrug it off. To be clear, our fondness for emerging equities today is driven overwhelmingly by their cheaper valuations, not a speculative belief in their resilience against an event that has not occurred since emerging became an institutionally buyable asset class. But if worse did come to worst and inflation flared up, owning a good chunk of the only equities that remember what inflation is like seems like a decent idea.

1 The Fed’s preferred measure of inflation is the Personal Consumption Expenditure deflator, which averages a couple of tenths lower than CPI. Their target is 2%, so 2.2% on CPI is pretty much exactly on target.

2 Facebook, Amazon, Apple, Netflix, and Google (now Alphabet).

3 There may well be a reason why no one has ever picked up on my financial market acronyms to date.

4 The Hussman P/E was invented by John Hussman, an extremely prolific writer on markets as well as the founder of Hussman Funds. He did not name it after himself, just as Shiller did not actually name CAPE after himself.

5 While I still think of this as the “Lehman” Aggregate, apparently the full name now is the Bloomberg/Barclays US Aggregate Bond Index. I have to admit the name has a bit of alliteration on its side, but I find it far from mellifluous.

6 And it should go without saying that this is far from the worst outcome one could imagine with regard to inflation. Long-term inflation expectations got to 7% in the 1970s in the US, and real yields peaked far above 3%.

7 As long as the forward curve of commodity prices wasn’t pricing it in. Given the way commodity futures indices have underperformed spot commodities over the last 15 years, that’s a decently big if.

Ben Inker. Mr. Inker is head of GMO’s Asset Allocation team and a member of the GMO Board of Directors. He joined GMO in 1992 following the completion of his B.A. in Economics from Yale University. In his years at GMO, Mr. Inker has served as an analyst for the Quantitative Equity and Asset Allocation teams, as a portfolio manager of several equity and asset allocation portfolios, as co-head of International Quantitative Equities, and as CIO of Quantitative Developed Equities. He is a CFA charterholder.

Disclaimer: The views expressed are the views of Ben Inker through the period ending December 2017, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Copyright © 2017 by GMO LLC. All rights reserved

Career Risk and Stalin’s Pension Fund:

Investing in a World of Overpriced Assets (With a Single Reasonably-Priced Asset)

Jeremy Grantham

Summary

■ Inside GMO there are three different views on whether and how rapidly the market will revert to its pre-1998 normal: James Montier feels it will be business as usual and revert within 7 years. Ben Inker also holds out for a 7 year period, but includes a 33% chance it will revert to a higher average valuation (the “Hell” scenario). I believe that the reversion on valuations will take 20 years, and that profit margins will probably only revert two-thirds of the way back to the old normal.

■ All three outcomes are quite possible. This creates a difficult investment challenge.

■ My proposition, though, is that there is an optimal investment for all three outcomes: a heavy emphasis on Emerging Market (EM) equities, especially relative to the US.

■ The next difficulty lies in deciding how much to emphasize this investment, which is perceived as riskier than most, and can of course fail.

■ I firmly believe that asset allocation advice should not be offered unless you are willing, on rare occasions, to make major bets and accept a big dose of career and business risk. Otherwise asset allocation should be indexed.

■ In contrast, a traditional, diversified 65% stock/35% fixed income portfolio today, designed to control typical 2-year career risk, I believe is likely to produce a return over 10 years in the 1% to 3% real range – a near disaster for pension funds.

■ To concentrate the mind, I fantasize about managing Stalin’s pension fund where the penalty for failing to deliver 4.5% real per year over 10 years is death. I believe only a very large investment in EM equities will give an excellent chance of survival.

■ Since February 2016, EM equities have already moved 11% relative to the US. But their three earlier moves since 1968 were at least 3.6x the developed world markets!1 Absolutely, at around 16x Shiller P/E, EM equities can keep you alive.

■ Even a quite successful attempt to leap out of the market and back in, although likely to beat the conventional approach, is unlikely to beat a very heavy EM equities portfolio.

■ Conclusion. Be brave. It is only at extreme times like this that asset allocation can earn its keep with non-traditional behavior. I believe a conventional diversified approach is nearly certain to fail.

Background: A Rapid Market Fall Back to the Old Trend or a 20-Year Slow Retreat?

At GMO these days we argue over three very different pathways to a similar dismal 20-year outlook for pension fund returns. James Montier thinks it is likely that we will have a very sharp market break in the near future, back to the old pre-1998 levels of value and that we will stay there, with the last 20-year block becoming an interesting historical oddity. Ben Inker – the boss – also believes things will revert over 7 years, but considers it plausible that the valuation level the market will revert to has changed, leaving near-term returns better than James’ view, but the 20-year return largely the same. I represent a third view, that the trend line will regress back toward the old normal but at a substantially slower rate than normal because some of the reasons for major differences in the last 20 years are structural and will be slow to change. Factors such as an increase in political influence and monopoly power of corporations; the style of central bank management, which pushes down on interest rates; the aging of the population; greater income inequality; slower innovation and lower productivity and GDP growth would be possible or even probable examples. Therefore, I argue that even in 20 years these factors will only be two-thirds of the way back to the old normal of pre-1998. This still leaves returns over the 20-year period significantly sub-par. Another sharp drop in prices, the third in this new 20-year era, will not change this outcome in my opinion, as prices will bounce back a third time.

These differences of assumptions produce very different outcomes in the near and intermediate term. Near-term major declines suggest a much-increased value of cash reserves and a greater haven benefit from high-rated bonds.

My assumption of slow regression produces an expectation of a dismal 2.5% real for the S&P and 3.5% to 5% for other global equities over 20 years, but also a best guess of approximately the same over 7 years. This upgrades the significance of the positive gap between stocks and cash and downgrades the virtues of cash optionality and long bond havens. This much is clear.

What is not so intuitively obvious is how similar all three estimates are for 20 years. All three are within the range of 2.5% to 3% real return for the US – a dismal outlook for pension funds and others – and within nickels and dimes for other assets.

A problem for investors following GMO’s writing is which of these three alternatives to choose. It is pretty clear to me that all three are possible. Ben Inker, our head of Asset Allocation, has tried hard to make our clients’ portfolios relatively robust to either a very bad medium-term outcome (the James scenario) or a relatively benign outcome (my scenario). I am going to attempt something much simpler here – some might say oversimplified, but I hope not – of asking which investments are appealing in all three outcomes, but particularly the 7-year and 20-year versions. My conclusion is straightforward: heavily overweight EM equities, own some EAFE, and avoid US equities. The next question is how brave to be in this type of situation, where there is only one asset that is reasonably priced in a generally very high-priced world. This is the topic I want to emphasize this quarter.

What is the point of asset allocation?

Making good-sized bets and winning. If you mean to offer a useful asset allocation service to institutions, one that is designed to beat benchmarks and add value as well as lower risk, then you must make bets. And when there are great opportunities, which is all too often not the case, you must make big bets. If you mean only to tickle the allocation with slight moves, you may have a good framework for coffee time conversation with clients but you are not going to make a difference. Ever. If you are not prepared to put considerable career or business risk units on the table (and be prepared to persuade the clients’ managers to do the same!), for example, in a classic equity bubble like 2000, or a classic housing bubble with associated junk mortgage paper in 2007, then you should not offer the service. Let the client index the allocation, as many do. Given plenty of company they can at least sleep well, knowing that if they run off a cliff, which they will do every 10 or 15 years, they will not be noticed in the herd. Keynes explained career risk (and how it encouraged momentum investing) first and still best in Chapter 12 of The General Theory in 1936: Never, ever be wrong on your own. If you are “you will not receive much mercy.” Yet, he also pointed out earlier in 1923 that for advice to be useful it needs to rise above faith in long-run regression to normal. “This long run,” he famously said, “is a misleading guide to current affairs. In the long run we are all dead. Economists [and market gurus] set themselves too easy, too useless a task, if in tempestuous times [such as bull markets] they can only tell us that when this storm is past the ocean is flat again.” And this unusual “tempest” of way over old-normal prices has lasted for 20 years and still continues.

The Catch 22 of asset allocation: career risk (and clients’ patience)

The Catch 22 of trying to give useful asset allocation advice is that you cannot expect to be right all the time. You will make mistakes, mostly in timing, but possibly also in analysis, and you will pay a price. Your objective is to be as aggressive as you can be and just not lose too much business. Some cycles are well-behaved and sometimes most of us, anyway, get lucky. But once in a dreaded while opportunities that were already brilliant become incredibly brilliant just as early 1998 broke out above the previous record P/E on the S&P of 21x in 1929 and then went on to 35x! So there is no easy answer. You can know in your bones what to do but still not have enough career risk units up your sleeve, or the natural risktaking tolerance to do it. That is, as we like to say, why these opportunities get to exist in the first place. It would certainly help if your firm is designed to withstand some considerable career and business risk. Independence is good. Looking back, 1999 seemed to prove that no large investment house felt that it could afford the client loss of exiting the market early. Overwhelmingly they rode the market up and rode it down. And the one notable outlier changed its mind at the 11th hour and moved money into growth stocks from a very value-based approach. None of them was in that sense offering useful asset allocation advice. The proof of the pudding was in the degree to which the severe 50% losses in 2000-02 and in 2008-09 were avoided or not. Ingenious client communication and preparation on such occasions will certainly reduce the commercial pain of an error, but will by no means remove it.

Stocks are getting more efficiently priced…asset classes are absolutely not

Long ago, in the good old days, if you bought a company with obvious extreme financial or marketing problems and it did not work out, you were considered an absolute idiot – every sane person (clients would say) knew to avoid such folly. Since they represented dangerous career threats, these companies became that much cheaper to own; although some would fail and hurt you, the average return would be handsome. Thus a portfolio of “dogs” as we called them, with the lowest P/Es and lowest price-tobook ratios, would regularly outperform the blue chip favorites – universally recommended then by established banks – by five or six points a year.

Then, into this story perhaps too good to last, came an army of quants and more highly-trained analysts than had been normal at least in the pre-1990 era. The price-to-book effect was easily modelled as were an increasingly sophisticated army of measurements of out-of-favor stocks. Simultaneously, clients were advised by academics and practitioners alike that sophisticated investors looked at the bottom line – the portfolio performance as a whole – and did not obsess about individual stock successes or failures. Thus the career risk of picking down-and-out companies dropped away, and with it, not surprisingly, much of the extra performance for buying them. Buying “dogs” had become reasonable and prudent, even on occasion trendy – who would want more overtly successful companies when cheap companies had a 4% edge, or 3% or 2% or even 1%? And so the big easy wins of “cheap stocks” got on the boat with Tolkien’s elves and sailed off, to be remembered as a golden era. Even a moderate edge now required more sophisticated, more accurate measures of true economic value. The army of quants and the influx of talented people had done the damage – who needs to be building fusion or fission plants when they could be making multiples of their salary helping build models and trading in nanoseconds (to pick on that least socially useful tax on institutions)?

But the severe market breaks of 2000 and 2007 showed one thing very clearly: that at the asset class level there was not even a hint of increased efficiency. The peak of 2000 offered perhaps the all-time best packet of mispriced asset classes – one versus another. Value and small cap had never been cheaper compared to growth and large cap. Small cap looked as if it could rally 70 percentage points to catch back up, which it duly did. Even more remarkably, perhaps, US REITs yielded 9.1% at the very top of the market against the all-time low yield on the S&P 500 of 1.5% – all to be justified by a 1% per year faster growth in dividends! By the time the S&P was down 50%, the REIT index was up close to 30% (and small cap value was up 1% or 2%, also not bad). The new long real bonds, or TIPS, yielded 4.3% and regular long bonds yielded 5% or 3.5% real. All amazing. Then more recently in 2007-08 there was the broadest overpricing across all countries, over 1 standard deviation, than there had ever been. So, major opportunities at the asset class level have been alive and well in this period of the last 20 years and compare, for once, favorably to the “good old days.” Why?

Why asset classes are still inefficiently priced

In contrast to the increased acceptability and lowered career risk that had narrowed the value opportunities at the micro level, there was still nowhere to hide at the asset class level. You go to cash too soon and your business or career melts away, you stay too long and you are seen as useless. In short, investing at the asset class level remains dangerous to career and profits and is, hence, inefficient, thereby allowing for occasional great opportunities with the old attendant caveats.

The inefficiencies today: EM and EAFE vs. US equities

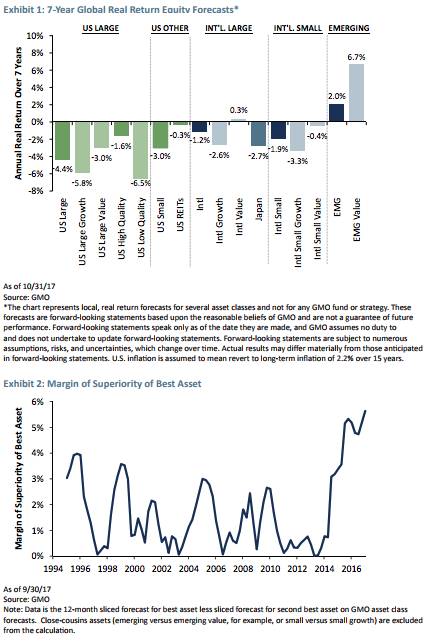

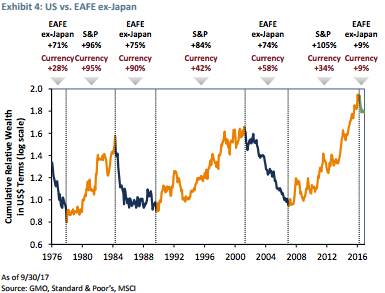

Which brings us to today and Exhibit 1, which is GMO’s 7-year forecast, including that for EM Value stocks. Exhibit 2 shows how remarkable the estimated gain is for EM Value relative to the next best asset on our data, compared to the greatest gaps available over recent years. But, Exhibit 3, from Minack and Associates in Sydney, suggests that GMO’s forecast may still be understating the opportunities in EM equities. It plots the straightforward measure of Shiller P/E (price over 10 years of average real earnings after inflation). My using an outside source is deliberate: to cross-reference and also to suggest that GMO’s estimates, in the interests of safety, are conservative (discussed later). Note that at the recent low in February 2016 (Point 1), the multiple on EM equities was lower than after the crash in 2009! Remarkable. Meanwhile (Point 2), the multiple on the US had gone from 12 to 22, an almost 100-percentage-point spread in favor of the US in just 7 years. The Emerging index had sold at 38x in late 2007 (Point 3), a very substantial premium (52%) by any standard over the 25x of the US index. It had sold again at a premium as recently as 2011 after the crash. And early last year, the US was at a 120% premium the other way. When you see the absolute and relative volatility of these three indices in Exhibit 3, doesn’t it suggest money to be made and pain to be avoided, even with less than perfect predictive power? It certainly indicates an old-fashioned level of extreme market inefficiency at the asset class level.

On an absolute basis also notice two additional things from Exhibit 3: 1) developed ex-US is well below its 20-year average and 40% below the US; and 2) Emerging is 65% below its high in 2007. What it was doing at such a colossal level back then in 2007 is of course another question, but that it was indeed there illustrates quite nicely my point about chaotic asset class pricing.

I have been walking through this quite slowly in order to underline my point that 18 months ago EM equities offered a good absolute return and a rare excellent relative advantage to the US. I will discuss later how much of that is left today. But first, let’s address the key question: How brave should one be when only one asset is cheap?

How brave to be in asset allocation when Emerging is the only cheap asset

Having hopefully sucked you in by now on the general idea, let me close the trap. How many of you institutions had 10% in EM equities in the spring of last year, or, for that matter, by year-end? My anecdotal survey results from four regional conferences suggest 10% to 20% of you. So, how many had over 20%? Survey results suggest very few. Perhaps 5% or less. And given the opportunity then and the scarcity of opportunities elsewhere, how much should we at GMO and you have had then in EM equities? And how much today? Well, today in our Benchmark-Free Allocation Strategy we have 25% plus 3% in Emerging Country Debt, which is very similar (say, two-thirds equivalent), so let’s say 27%.

t this point let me tell you a story. In mid-December last year, I told my colleagues in asset allocation that I was putting up to 50% of my sister’s and children’s pension funds into Emerging. (I didn’t mention this in the Quarterly Letter then only because it was pre-empted by “The Road to Trumpsville,” which had suddenly become much more topical. I’m sad because the move to Emerging was timely as it turned out, but everything has a price. I did, however, describe this approach at our annual client conference last November as “The Kamikaze Portfolio.”) Obviously, “up to 50%” is a lot more than 27%. (My sister and children are at about 55% today. Why it was not 100% back then, however, is a good and very difficult question to answer. Failure of nerve, I suspect.) But here is the problem: A lot of reasonable and experienced people, some at GMO and some on the client side, have increasingly feared an imminent major market downturn, even a crash. Now let us imagine that this year had been the start of an 18-month decline of 40% in the S&P 500 and Emerging, with its higher beta, was on its way to a decline of 50%, as many would expect in such a situation. What would happen, in that case, to a manager who put 40% in Emerging? Nothing pleasant shall we say. A 40% bet would not even be seen (especially in hindsight) as prudent, which characteristic is defined as what a substantial majority of investment people think is normal behavior. Whereas my sister, who knows nothing about investing, would wait it out happily enough in ignorance – a perfect example of what a difference is made by absolute freedom from career risk.

Stalin’s pension fund management: the ultimate career risk

This is where Stalin’s pension fund comes in. Joe Stalin has appointed you to a well-paid cushy job looking after his substantial pension fund. Do well enough and you will receive Black Sea privileges, a dacha outside Moscow, and a good pension. Do badly and you will discover that Stalin has a nasty temper. In fact, you will be shot. Conveniently, Stalin, who likes precision, has defined a very precise benchmark: 4.5% real for 10 years. (He understands that 4.7% real is considered the “normal” return to a 65% equity/35% fixed income portfolio and is being, atypically, a little friendly by rounding down.) And in this parallel universe you have only GMO’s current 7-year forecast (Exhibit 1) with the understanding that: a) we have had some success in ranking asset returns; but b) have been about 2% on average too low when measured today, although measured at the market low in 2009 we had averaged 1% too high. (Of our current 2% average, 2.25% of the underestimate was caused by ending at higher equity and long bond prices than we had expected from long-term data; 1% per year was caused by higher profit margins than before or than anticipated; and +1.25%, in the opposite direction, by having yields be 1.25% less because of higher prices.) Looking at this data, you now have to make a decision on which your life depends. Now that is real risk! And I should help you by pointing out that Exhibit 3 indicates that our EM and EAFE numbers at GMO might be conservative even by our average standards, perhaps because I bequeathed a tradition to our asset allocation unit long ago that when we love one asset and hate another that we be a little mean to the one we love and a little generous to the one we hate to build in a bit of that old Ben Grahamite margin of safety. Not a bad principle, but when your life depends on it you better understand all the subtleties. Here’s the problem: If you invest to keep your normal 2-year career risk under control by doing what normal investors think is normal and produce a typically diversified 65% stock/35% fixed income portfolio with the 65% in equity divided, say, 37% in the US, 17% in EAFE, and 11% in EM and do it on a buy-and-hold basis for 10 years, you will surely die. On our numbers, it totals today to a grand cumulative return of 8.2%, or under 1% a year! Even adding the full 2% to allow for our conservatism – which is probably an unreasonably large adjustment when measured so high into a market cycle – gets you to just +3%. No, you basically have no realistic chance of survival, not even 15%.2 So what would you actually do in real life? I know what I would do. If only the standard asset classes on our list were available to me, I would invest 100% in EM equities, with two-thirds tilted to Value, and I would probably get to live. From our GMO forecast (Exhibit 1), the blended annualized real rate over 10 years would be 5.7%. Plus, add a little for our conservatism. From Minack’s current 14.5x Shiller P/E, for all Emerging you get an earnings yield of 6.9% (100/14.5), let’s say minus the usual slippage of 1%, or almost 6% real. (Now admittedly the last 10 years’ profit margins embedded in Shiller P/E are much higher than average for the US, but that is not so clearly the case for Emerging. So, adjusting for abnormally high current earnings moves the relative value even further to EM.) Thus, the total commitment to EM would give me, I estimate, at least a 70% chance of survival. So, what would you do? Let me guess: You would do pretty much the same, I think, under these conditions. But luckily your life does not depend on the outcome of the next 10 years. So, two-year career management rules the day – as usual – with the need to be normally diversified or superficially “prudent.” With the consequence that pension funds should brace themselves for a disastrous 1% to 3% return in the next 10 years – but it’s a useful experiment, I think, to imagine that your life depends on the outcome.

Comparison of a big EM bet to a policy of an extreme move to cash

A different attempt at staying alive might be to jump out of the market and wait for better times. The only sound reason to ever hold lots of cash like this at negative real rates would be that: a) you were confident of a crash fairly soon; and b) you were also confident in your abilities to reinvest in a timely way and execute a sound strategy for the remaining time, all of which is not easy. Well, let’s assume you are not clairvoyant so that you miss a last 18-month gain in the market before it breaks (we missed 2.5 years from late 1997). Then let’s say it takes 2 years to decline (it took 1 year in 2008 and 3 years in 2000) and then you miss only 6 months before investing for the final 6 years at the old-normal returns – I’ll even give you half the invested return for the 6 months. In my opinion, that set of assumptions requires above-average talent, some steely nerves, and a bit of good fortune. The bad news is that after this 4-year phase-in, fully investing for only the last 6 years of the 10-year test, in a normal diversified manner and even at pre-1998 average prices and returns, you will not reach a 4.5% average return for the whole 10 years, but just over 3%. (Admittedly, 3% is a lot better than the under 1% a year earned from combining the GMO 7-year forecast followed by three old-fashioned good years. But still not enough for Stalin.)

To summarize: The return from getting out and back in with skill and experience – say +3% real a year – will very probably beat a typically diversified portfolio (1% to 3% real a year), but is very likely to fail to beat a portfolio prepared today to invest heavily in a single decent asset class – EM equities with its 5.5% estimated return (particularly if tilted to Value).

Likely performance of EM equities in a down market: relative value also matters

Let me add a point on the performance of EM equities in a major market break. Everyone expects that these assets would drop like a stone, worse than their US counterparts. But historically that is not how it works. Yes, beta is very important in a bear market or any market when explaining relative performance, but so is value. Let me give you an example. Back in 2000 we were saying that we were very bearish on the US but also very confident that small caps would outperform. The client response was either bewilderment or shock at our inconsistency. The partial antidote for clients was a historical review of small cap behavior in all previous down markets divided into three groups. When small was in its most relative expensive third, these stocks fell on average well over their 1.2 beta. In the middle third they indeed delivered the expected extra downside performance. But on average, when small caps were in the best third of being relatively cheap against large caps, they went down less than the market. And in 2000 they were co-equally the cheapest they had ever been (with 1973). The 2000 crash, which was made to order for allocation, once again proved this point with small cap at the low being down less than 40% of large cap and small cap value actually up absolutely by a nose (plus 2% or 3%) versus minus 50% for the S&P 500! Looking back at the performance of EM equities, they were relatively very expensive indeed in 2008 and fell like a very large stone, probably the most rapid decline of that magnitude for any broad index ever – over 60% in 4 months. Back in 2000, although Emerging was absolutely high-priced, it was still considerably cheaper than the US and beat it slightly in the decline. In major rapid declines, relative (and absolute) value indeed plays a very large role alongside beta. Thus, today it is possible that EM equities would decline more than the US in a major decline, but I believe it is improbable.

Recent relative performance of EM equities and its relevance

Since hitting a multi-year low in February last year, at 11x Shiller P/E, the MSCI Emerging Index has beaten the US market by 11% in total return when measured in dollars, with the outperformance driven mostly by currency. The relative P/E has moved less than 5%. It is always irritating to miss the low, but to put this performance in perspective we should look at the relative outperformance in previous cycles. From 1968 to 1980 Emerging won by over 300%. Next, from 1987 to 1994 it again trounced the US by over 300%, and most recently from 1999 to 2011 it returned 3.6x the US. And in between, of course, it loses impressively. Investing when Emerging is at a premium is definitely bad for financial health. In the very long run it appears to have won by 0.5% a year, with more than all of this excess return coming from being cheaper and yielding more. Just let’s summarize by agreeing that the +11% is in this context trivial.

Recent valuation on Shiller P/E is around 14.5x, suggesting a 5.9% real embedded return (after slippage). On GMO’s adjusted basis, a Shiller P/E is more like 16x, with an earnings yield of 6.25% and, net of 1% slippage, 5.25%. GMO also likes to emphasize relative values ex-Banking and Resources, which makes Emerging look less attractive as these markets have substantially larger shares in these two currently cheaper areas. My view on Resources is that the cycle has turned, global economies are doing quite well by recent standards, and oil prices are likely to rise for three years or so.

There is no denying, however, that Resources is an unpopular group. But because of this these stocks have outperformed a little. I have no complaint with the idea that EM equities should therefore be cheaper. Comparing the whole index with the US should reflect an average discount, which it does. And comparing a long history of comparisons, for all of which Emerging carries more Banking and Resources, we are today in the cheapest 10% to 20% in favor of Emerging.

Conclusion

Be as brave as you can on the EM front. Be willing to cash in some career risk units. Bravery counts for so much more when there are very few good or even decent alternatives.

Postscript 1: EAFE vs. US is probably a better bet than you think

Exhibit 3 already showed how relatively well EAFE (or developed ex-US) is positioned on Shiller P/E compared to its 20-year average and how much cheaper it is than the US. But now I have an excuse to introduce Exhibit 4, one of my all-time favorite exhibits that I first used almost 15 years ago. It shows the relative moves over the last 45 years between the S&P and EAFE ex-Japan. (Japan’s bubble back then ruined all historical series so we took it out and left it out, although Japan today is likely comparable to EAFE ex-Japan.) Just look at the length and depth of the moves and how these waves roll across the page, +84% for the US, then +74% for EAFE ex-Japan, and so on. Culminating in the grandest cycle of all was the +105% for the S&P. As I like to ask in my stump speech to institutions: Which direction will you bet on for the next 50% move? I think the answer is clear: The odds must be 5 or 10 to 1 in favor of EAFE ex-Japan. I have a real weakness for these cruder than usual exhibits. They seem somehow rough, but tough and confidence-inspiring. And what a testimonial to the inefficiency of pricing between asset classes. And what a good illustration of the point that these inefficiencies are still very much alive and well at the asset class level, with the biggest move of all right now, and which could of course still go higher. Looking at this exhibit, it is easy to imagine, though, that EAFE ex-Japan could reasonably be expected to make a very big move relative to the US. GMO’s 7-year forecast is for a substantial 28% swing in EAFE’s favor. But our forecasts do not consider currency, and the keen-eyed reader will notice that in every cycle the currency has moved in the same direction as the overall move. (The value effect says that a strong currency will hurt exporters’ volume and reduce foreign earnings restated into dollars. And both effects do occur. But the momentum effect has foreigners saying “look at the US market go, let’s buy some” and in so doing they invest in dollars and push the currency up. And here the momentum effect clearly dominates the more intuitively obvious and more talked about value effect.)

So let’s say in addition to the 28% GMO predicted move in stocks, there is an incremental positive move of 8% in EAFE currency – which we at GMO indeed consider modestly cheap relative to the dollar. These effects multiply out so we get 128 x 108 = 38%. But Exhibit 4 also shows that each cycle passes through fair value and out the other side, from cheap to equally expensive, so a +38% move becomes a +76% move, which, coincidentally or not, is the same as the last two EAFE ex-Japan moves. Now we are really talking turkey. This being the case, should we reconsider the 100% Emerging Stalin portfolio and make it perhaps 80% Emerging/20% EAFE? I think both are reasonable survival portfolios for Stalin’s pension fund. I can conclude by noticing that zero career risk – say managing your own money – and ultimate career risk – your life is at stake – both produce the same, or very similar, results. In contrast, normal two-year career management produces something very different – the need to look normal – which I believe in our current situation is dangerously counterproductive.

Postscript 2: Early-stage venture capital may be the best bet (if you have good access)

Just a word on the very heavy use of early-stage venture capital (VC) in my Foundation (45% of our total). To be honest, if I had the choice of VC in the Stalin fantasy I would definitely keep two-thirds of my money in early-stage VC and put the final third in EM equities. The animal spirits of the US capitalist system are lower than they used to be. There are only half the number of people working for new companies – one or two years old – as a share of the workforce as there were in 1970. Despite the emphasis we give to Amazon and a handful of others, we are simply not as adventurous as we once were, but are now more careful of protecting margins, less willing to capital spend, and simply more monopolistic, as reflected by the high concentration of large firms in every industry. In this changed world, I believe that early-stage VC, and only early-stage, has become the last bastion of enterprise and, though it may be overpriced as a class compared to long ago, it seems less overpriced than everything else.

Jeremy Grantham. Mr. Grantham co-founded GMO in 1977 and is a member of GMO’s Asset Allocation team, serving as the firm’s chief investment strategist. Prior to GMO’s founding, Mr. Grantham was co-founder of Batterymarch Financial Management in 1969 where he recommended commercial indexing in 1971, one of several claims to being first. He began his investment career as an economist with Royal Dutch Shell. He is a member of the GMO Board of Directors and has also served on the investment boards of several non-profit organizations. He earned his undergraduate degree from the University of Sheffield (U.K.) and an MBA from Harvard Business School.

Disclaimer: The views expressed are the views of Jeremy Grantham through the period ending December 2017, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2017 by GMO LLC. All rights reserved.

© GMO

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits