Heading into 2018, we remain positive on global equities and believe the outperformance of international risk assets can continue, despite the strong year-to-date returns in global markets.

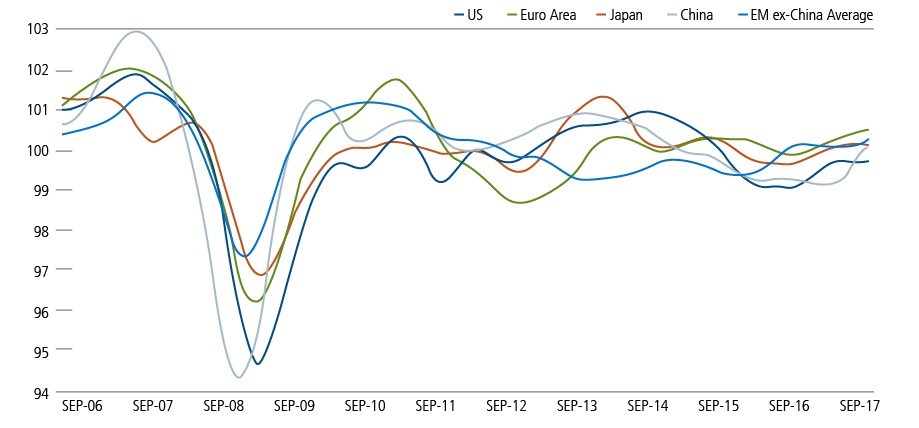

In the years following the Global Financial Crisis, uneven global growth created headwinds for risk assets outside the US. Typically, one or two regions would show improvement, while other regions decelerated. Over this period, the US economy was the relative leader, and the dollar strengthened. However, since early 2016, global growth has begun to accelerate fairly uniformly against a backdrop of still-highly accommodative central bank policies and recently implemented economic reforms (Figure 1). With non-US economies in earlier-stage recoveries, we expect supportive conditions for international risk assets to remain in place.

FIGURE 1. SYNCHRONIZED GLOBAL GROWTH SUPPORTS OVERSEAS ASSETS Leading Indicators (OECD Main Economic Indicators)

Source: Macrobond, using OECD, Composite Leading Indicators, seasonally adjusted.

Dollar Weakness Provides a Tailwind to International Risk Assets

In addition to improving global growth and attractive relative valuations, non-US equities are positioned to benefit from a US dollar that is at least 20% overvalued and appears to be entering a period of prolonged weakness. We may be seeing the earlier stages of this trend, as the dollar is on track for the worst year since 2003, down approximately 7% year to date.

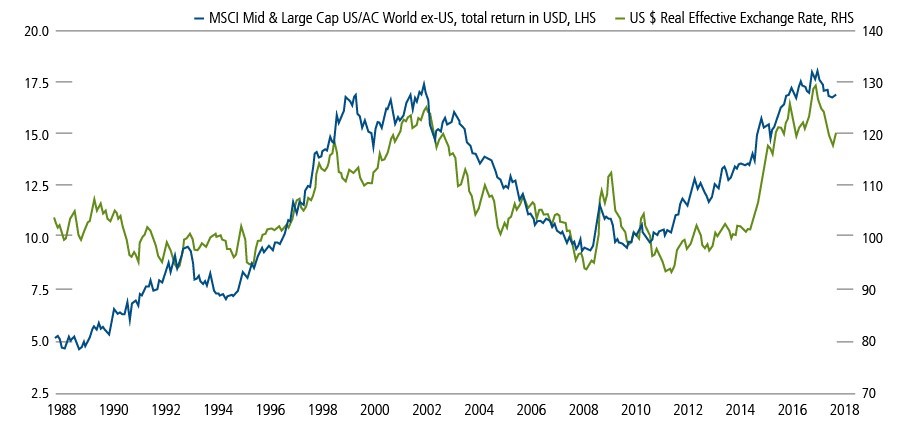

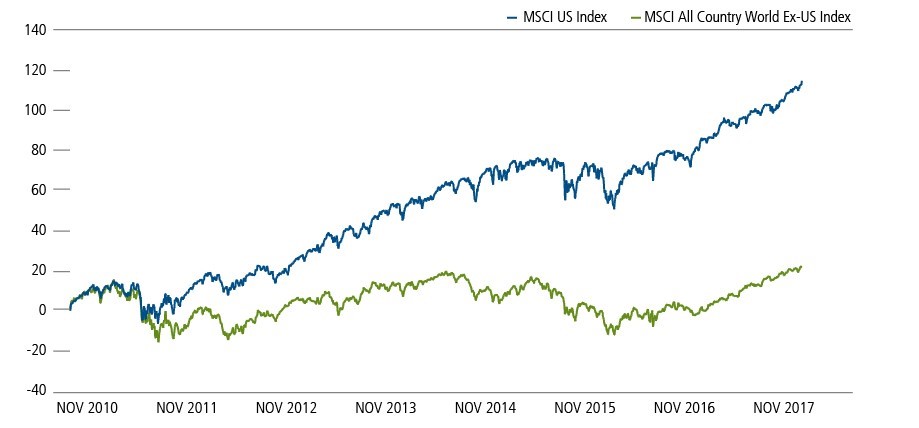

The path of the dollar will continue to be a key variable for overseas markets. As Figure 2 shows, the returns of non-US equities have been highly correlated. Historically, as the dollar has weakened, we’ve seen an outperformance of foreign equities greater than the currency return differential. We believe the dollar is likely to weaken further versus the trade-weighted basket, which would support continued outperformance in foreign equities. Figure 2 also illustrates that regime changes (strong-dollar-to-weak-dollar) have historically been multi-year phases.

FIGURE 2. US DOLLAR DEPRECIATION AND NON-US EQUITY OUTPERFORMANCE HAVE BEEN CORRELATED US Dollar and MSCI US Index Versus MSCI All Country World ex-US Index

Past performance is no guarantee of future results. Source: Macrobond.

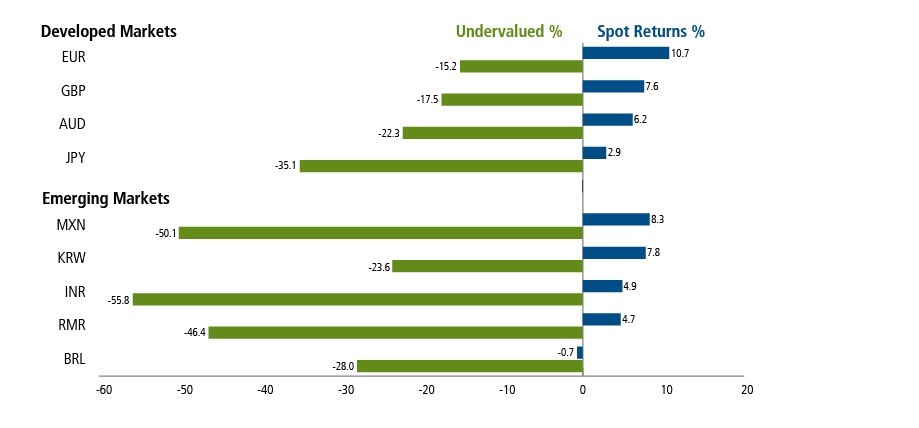

Despite the strong year-to-date performance of many developed market and emerging market currencies, they remain 15% to 30% undervalued (Figure 3). Currencies can remain over/undervalued for prolonged periods, but are ultimately mean-reverting. Given the recent improvement in growth and technical trends, we expect these valuations to converge over the next several years and support higher total return potential in international equities.

FIGURE 3. BROAD UNDERVALUATION IN NON-US CURRENCIES Purchasing Power Parity

Source: Bloomberg. Data from 12/30/16 through 10/31/17

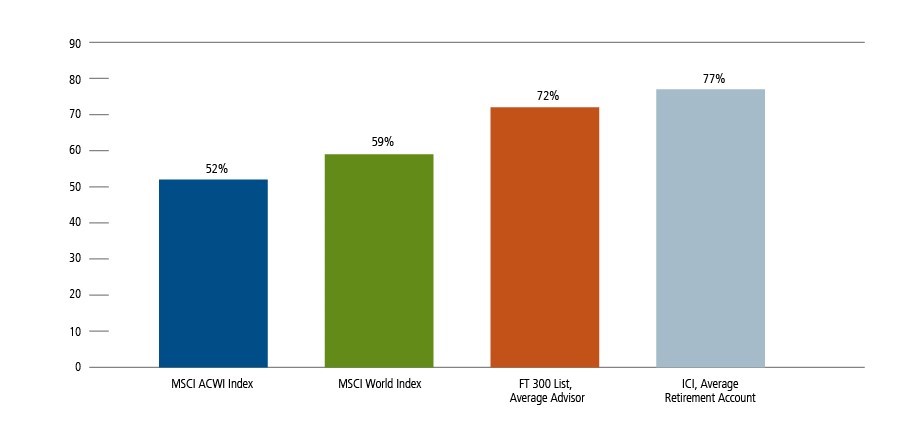

For many US investors, there’s still been no place like home. Almost half the global equity market resides outside the US, yet the average financial advisor and individual retirement account allocate 72 to 77% of equities inside the US. We expect that over the next several years, investors will take profits in US equities and allocate overseas, where they can take advantage of attractive growth, valuations, and secular tailwinds. Thus, this current underinvestment can provide additional support for an extended outperformance cycle.

FIGURE 4. US INVESTORS HAVE OVERLOOKED NON-US OPPORTUNITIES % Invested in US Equities, Index Weights Versus Investor Allocations

Source: Financial Times, June 22, 2017, FT 300 Advisor Study June 2017, MSCI Inc. Oct 2017, ICI Factbook 2017

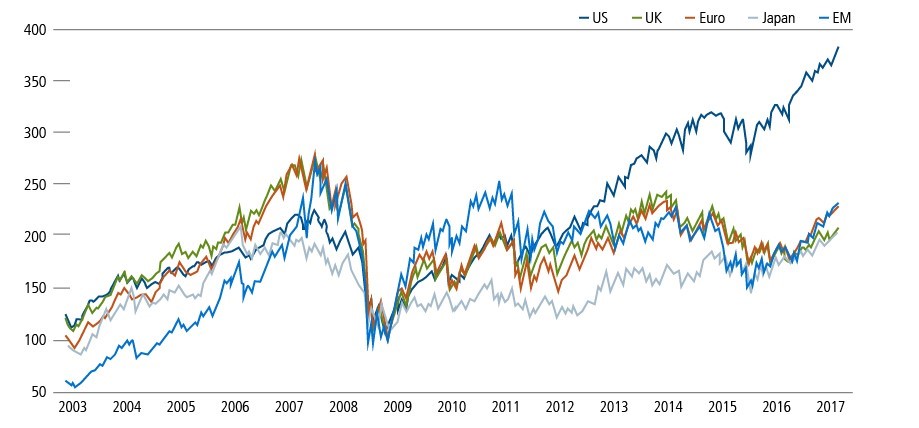

Coming out of the Global Financial Crisis, emerging market equities led the initial recovery, but after a period of consolidation, US equities significantly outperformed other regions, which has contributed to the overweight bias many investors have in their portfolios. Despite the year-to-date rally in non-U.S. assets, a significant divergence in returns remains. We expect these returns to mean-revert over time.

FIGURE 5. US EXCEPTIONALISM IN PERSPECTIVE US Versus Rest of World, Equity Returns Over Seven Years

Past performance is no guarantee of future results. Source: Bloomberg.

Global Equity Returns

Past performance is no guarantee of future results. Source: Gavekal Research, “London Seminar,” Anatole Kaletsky, Chen Long, Cedric Gemehl and Charles Gave, October 2017 using GaveKal Data/Macrobond (in USD terms)

Valuations Enhance the Appeal of International Assets

Relative valuations further the case for investing outside the U.S. As Figure 6 shows, Japan, Europe and emerging markets offer better prospects for growth and lower P/E multiples.

FIGURE 6. GLOBAL VALUATIONS, AS OF 10/31/17

Past performance is no guarantee of future results. Source: Bloomberg. Data in USD terms.

Conclusion

A combination of factors provides a highly supportive backdrop for non-U.S. risk assets going into 2018. In our view, the strong performance of international equities in 2017 can be sustained in an environment of synchronized global growth, earlier-stage recoveries in key overseas economies, an overvalued dollar and the likelihood for an extended period of dollar weakness, lower levels of US investment exposure to international stocks, and attractive valuations. However, country, industry and company selection will still be important differentiators. Fundamental research and risk management matter as much as ever in an environment of heightened geopolitical uncertainty.

--

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be suitable for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations. As a result of political or economic instability in foreign countries, there can be special risks associated with investing in foreign securities, including fluctuations in currency exchange rates, increased price volatility and difficulty obtaining information. In addition, emerging markets may present additional risk due to potential for greater economic and political instability in less developed countries.

Indexes are unmanaged, do not include fees or expenses and are not available for direct investment. The MSCI US Index is a measure of the U.S. equity market. The MSCI All Country World ex-US index measures the performance of global equities, excluding the US. The MSCI All Country World Index measures the performance of global equities. The MSCI World Index measures the performance of developed market equities. The US $ Real Effective Exchange Rate measures the value of the US dollar, adjusted for inflation, versus other currencies.

Earnings per share (EPS) is a company’s profit divided by its number of common outstanding shares. Price-to-earnings ratio (P/E) is a valuation ratio of a company’s current share price compared to its per-share earnings; forward P/Es are based on forecasted earnings. CAGR, or compounded annual growth rate measures year-over-year growth.

18168 1217O C

© Calamos Investments

© Calamos Investments

Read more commentaries by Calamos Investments