2018 Global Economic and Market Outlook

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsU.S. stock market indices continue to reach new highs and major global economies are growing in sync for the first time in a decade. Corporate earnings have reached record levels, business confidence indicators are climbing while inflation remains in check. There is the real possibility of tax reform, business deregulation is gaining traction and a new look for the U.S. Federal Reserve is on the horizon. What might it all mean for the markets and investors in 2018?

U.S. economic activity surges

Already buoyed by rising business and consumer confidence, a series of record-setting stock market rallies and an improving labor market – the U.S. economy may further accelerate in 2018.

“Based on our analysis, we project U.S. gross domestic product (GDP) growth in 2018 at 2.9%, up from 2017’s forecast growth of 2.3%,” says Derek Hamilton, Ivy Global Economist.

Overall business optimism is a key component of the U.S. economy and continues trending upward. Heading into 2018, small business owners have lofty expectations on increasing sales and adding headcount, and believe it’s a good time for expansion, according to the Small Business Optimism Index. In November, the index soared to its highest mark since 1983, and the second-highest reading in the index’s 44 years of existence.

Small business optimism still rising

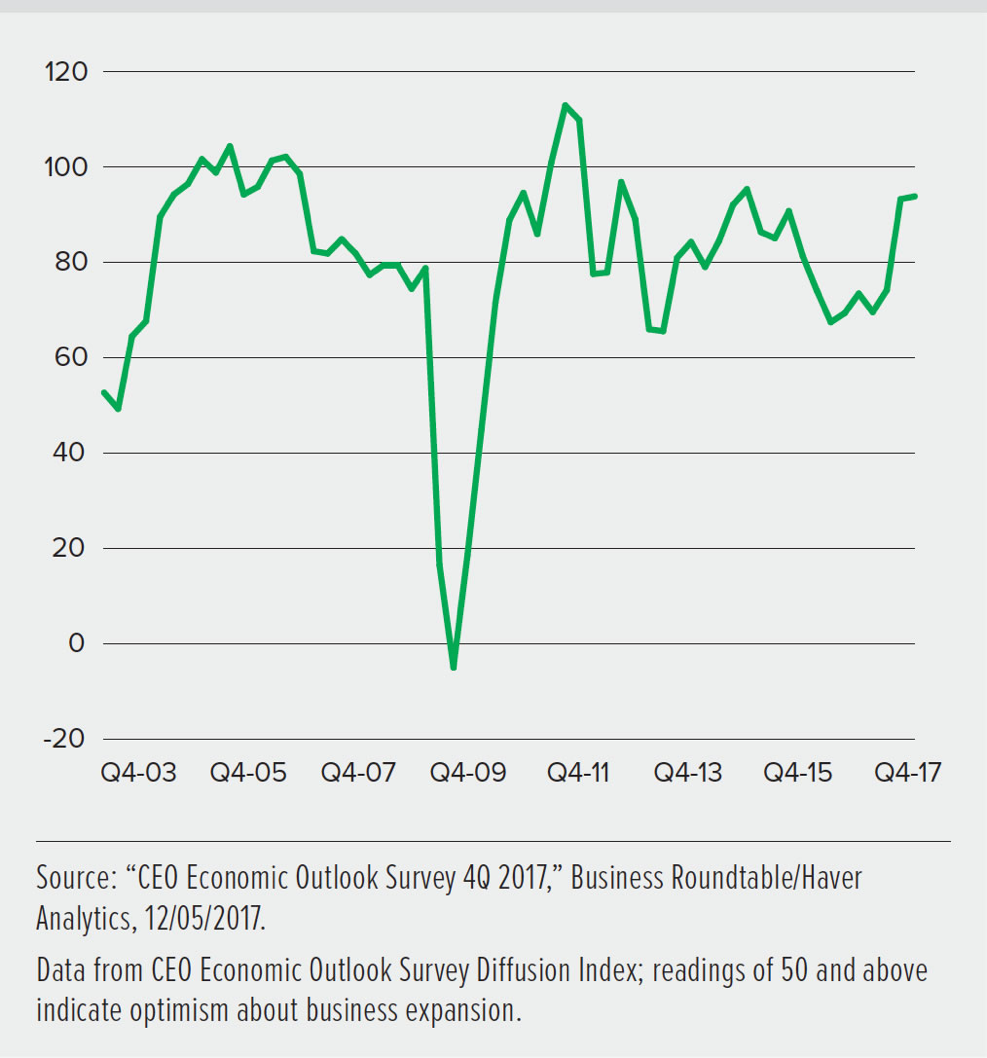

Large companies are equally confident as indicated by the CEO Economic Outlook Index, a composite of corporate executives’ sales projections, capital spending forecasts and hiring plans over the next six months. In December, the index reached its highest level in six years.

We think this confidence will continue to grow in 2018, especially if the U.S. Congress can complete its overhaul of U.S. tax policy, which many executives view as critical to greater global competitiveness for U.S. business.1

Large companies have growing optimism

Although the U.S. labor market is improving, wage growth has been sluggish at best. We believe wage growth could start to increase at some point in 2018. As always, we are keeping a watchful eye on any signs of an uptick in inflation, which remains below the central bank targets in many countries. In the current environment, with markets accustomed to very low inflation rates, any surprises that could trigger a surge in inflation would be disruptive.

"The stock market has responded positively this year to the fundamentals of global economic growth, strong corporate earnings and relatively benign inflation," says Phil Sanders, CFA, CEO of Waddell and Reed Financial, Inc. and CIO of Ivy Investment Management Company. "What makes this run remarkable is that it has been relatively impervious to investor anxieties emanating from political dysfunction in Washington, D.C., and geopolitical concerns across the globe. While expanding valuations, as well as corporate earnings growth, have been a key driver to the market advance, we believe continued earnings growth will have to carry more of the burden going forward," says Sanders.

Synchronized global growth continues

Part of the story is the remarkably synchronized global growth currently underway. We forecast global economic growth of 3.9% in 2018, up from 2017’s forecast of 3.7%.

Global GDP generally higher in 2018

We believe GDP growth in China, the world’s second-largest economy, may slow slightly next year as President Xi Jinping moves to balance the growth rate with the introduction of several reform programs. These include slowing the pace of debt accumulation and improving the country’s less-than-stellar record on environmental issues. Even if these reforms are successfully enacted, we forecast China’s growth rate still will reach 6.6%.

Growth in the eurozone appears to be on the same pace as 2017. We forecast its economy will grow around 2.3%. However, we anticipate GDP expansion in the U.K. may not reach that level. While both the European Union (EU) and U.K. economies have improved since the 2008 global recession, the ongoing “Brexit” negotiations have cast a pall of economic uncertainty over the region. The negotiations for the U.K.’s exit from the EU, which is slated to occur in 2019, are likely to continue through much of the year, adding to business anxiety about what comes next.

Emerging market countries are likely to continue to play a prominent role in global economic growth in the coming year. They hold the dominant share of the world’s resources, including land and total population. Additionally, Brazil and Russia are showing positive economic activity after multi-year recessions, complementing the positive economic outlook of larger emerging markets like India.

U.S. tax reform takes center stage

President Donald Trump has a mixed record of political wins so far in his term. Accomplishments like the easy and early confirmation of U.S. Supreme Court Justice Neil Gorsuch and more than 50 executive orders have been countered by several notable setbacks, including two failed attempts to repeal and replace the Affordable Care Act (ACA) and the unfulfilled campaign promises to impose more stringent immigration policies and deliver an infrastructure plan.

Trump seeks to achieve his first major legislative victory with the most sweeping overhaul of U.S. tax policy in more than 30 years. Taxes are a popular issue with his political base and many in the business community, and Trump – along with the Republican majorities in both houses of Congress – wants this win badly.

GOP leaders in Congress have long championed large-scale tax reform and have developed bills that permanently reduce the federal corporate tax rate to 20% from the current rate of 35%. They argue slashing the tax burden on U.S. companies will allow them to become more competitive, boost the economy, create more jobs and spur wage growth.

Plans in both the U.S. House of Representatives and Senate would repeal the state and local tax deduction while increasing the standard deduction amounts for both single and married households, as well as the child tax credit. Both bills also modify the current tax structure on the deferred foreign profits of U.S. multinational corporations to include a one-time tax levied against the profits of U.S. companies held overseas, which is estimated at $2.6 trillion.

While we believe a plan that reduces corporate tax rates is a positive move for markets, the two proposed tax bills also offer a number of differing provisions designed to further reform the complex tax code.

The House-approved proposal would consolidate individual and family tax brackets from seven to four. It would repeal the Alternative Minimum Tax and estate tax while phasing out or reducing several popular tax deductions, including limiting the mortgage interest deductible on newly purchased homes and interest on college student loans.

The Senate framework offers temporary reductions to individual income tax rates that would sunset after 2025. The Senate bill maintains the current number of tax brackets and includes a provision that would scrap the individual mandate penalty of the ACA. Finally, the Senate bill would delay the corporate tax cut until 2019, a caveat that triggered a significant market sell off when it was announced.

The next step is for the two very different bills to be hashed out in conference committee before sending a final version to the White House. Given the tight timeline and all the pitfalls this overhaul presents, the final bill is likely to see revisions and compromises. However, we are optimistic that some version of tax reform will be signed into law.

A new year, a new Fed

For the third time in 2017, the U.S. Federal Reserve (Fed) raised interest rates by 0.25 percentage point in December to put the key federal funds in a target range of 1.25–1.50%. This increase was widely expected by market participants and was the latest step in the Fed’s effort to normalize rates. We think the Fed may be more active on interest rates in 2018 with three and maybe four rate hikes, based on tax stimulus.

This slightly more aggressive stance on interest rates isn’t the only change at the Fed, which will be under new leadership in 2018.

In November, President Trump chose not to rename Janet Yellen as Fed chair, instead nominating Jerome Powell to the post. Powell, a Republican member of the Fed’s Board of Governors nominated by President Barack Obama, has a career spanning law, private equity and the Treasury Department under President George H.W. Bush.

Powell has earned a reputation as a non-ideological and pragmatic policy maker. He has voted for every Fed policy decision since 2012, including its four interest rate increases and the gradual unwinding of the Fed’s stimulus campaign. “Jerome Powell is philosophically similar to Yellen,” says Hamilton. “The Fed under Yellen has been very transparent in its expectations of future monetary policy. While we believe this practice should continue under Powell, we will be watchful for signs of increasing volatility as the Fed moves further away from its policies of quantitative easing and near-zero interest rates.”

While he has a dovish history of monetary policy making decisions, it appears Powell favors regulatory relief for banks.

“Powell wants fewer regulatory burdens, which he feels inhibit economic growth,” says Mark Beischel, Ivy’s Global Director of Fixed Income. “That would seem to indicate the potential for some unwinding of regulation in 2018.”

If Powell receives Senate approval, he will be taking the helm of the Fed in the midst of a substantial makeover. Three top policy makers, including Yellen, who led the normalization efforts currently underway have either left or will leave their posts in the new year. This gives Powell – and Trump – the tremendous opportunity to leave an imprint on Fed policies, including financial regulations.

New attitudes on monetary policy?

While the "new" Fed's postion on monetary policy is not anticipated to change, it’s a different story for central banks around the world as they exit their 2008 crisis-induced policies.

The European Central Bank (ECB) is scheduled to ease its Asset Purchase Program to 30 billion euros per month from its current rate of 60 billion euros per month starting in January. We believe inflation will be strong enough to allow this policy to conclude in the third quarter, and an interest rate hike could come as early as the fourth quarter of 2018. Conversely, we think the Bank of England will act cautiously on tightening its monetary policy in 2018 as it continues the complex Brexit negotiations with the EU. China’s recently established oversight body, the Financial Stability and Development Committee, has vowed to fend off systemic risks like rising debt and housing bubbles. As such, we believe the People’s Bank of China will maintain its prudent monetary policy in the coming year. We also believe the Bank of Japan is likely to continue to lag the rest of the world in removing its accommodative monetary policy taking little action on short-term rates, yet possibly allowing long-term rates to rise.

A look at the investment landscape

Despite a number of wild cards that could possibly trigger investor anxiety – Washington’s ongoing dysfunction, North Korea’s undeterred quest to join the league of nuclear powers and the deepening investigations into Russian election meddling, to name a few – investors remain focused on remarkably strong economic fundamentals. U.S. equities have continued their upward momentum and outperformed any other asset class in recent quarters. Overall, growth stocks have significantly outperformed value stocks for some time. This trend has been supported by the prolonged low-growth, low-interestrate environment that has pervaded since the financial crisis. Essentially, any growth has looked attractive, so investors have been willing to pay for it.

Credit spreads in the bond markets are tighter now than in the recent past. As of late November, the spread between investment grade and high yield was down to just over 400 basis points, a small margin for such a varying degree of risk. As central banks begin to normalize interest rates, it may be time to begin taking a more defensive position in fixed-income holdings by moving up in quality, according to Beischel.

“Investors need to ask themselves,” says Beischel, “‘Am I being compensated for the risk I’m taking on?’”

We think emerging market equities in many cases still offer attractive valuations versus developed markets. When coupled with potential rebounds in energy and commodity prices, we believe emerging markets are poised for further growth in 2018.

Key sectors to watch

The main catalyst of upward market activity for much of 2017, technology, could remain an area of focus in the new year while financials and health care stand to benefit from potentially more lenient regulatory environments.

Technology

The impact of the technology sector continues to be noteworthy with a weight in the S&P 500 Index approaching 25% in the fourth quarter of 2017. We believe this sector – led by the FAANG stocks (Facebook, Apple, Amazon, Netflix and Google-parent Alphabet) – could continue to see gains in 2018. We believe three trends could provide support to the sector in 2018:

- The growth of public cloud computing services, which allow companies to rent infrastructure to power all types of enterprises from online storefronts to gaming apps.

- The evolution of e-commerce retail as companies integrate more consumer interactions through online experiential design.

- The growing demand for ubiquitous connectivity in the “Internet of things” – everything from devices and automobiles to household appliances – may fuel demand for semiconductors.

While the sector has seen its share of growth over the last year, we believe pockets of opportunity still remain as technology companies stand to be key beneficiaries of the ongoing efforts to improve corporate productivity. Growing confidence in the economy and optimism within many companies’ management teams is likely to drive further corporate investment and may lead to renewed topline revenue growth.

Financials

The financials sector saw sluggish, but steady gains throughout 2017. We believe further investment opportunities are possible next year as these stocks stand to improve based on three drivers: controlled interest rate expansion, a more relaxed regulatory stance and tax reform. As previously mentioned, if the Fed‘s new leadership takes a more business-friendly stance on regulation, any progress on deregulation could improve operating and capital flexibility, especially for banks. Lastly, since most financial stocks operate largely in the U.S., enactment of tax reform that significantly lowers the current corporate rate could have a disproportionately positive effect on the sector.

Health care

While the health care sector was marked with volatility toward the end of 2017, we maintain an optimistic view for the year to come. There are a few macro factors driving our perspective. Biotechnology advances are on the cusp of revolutionizing standards of care and driving more positive outcomes in complex diseases. Leadership at the U.S. Food and Drug Administration has shifted toward more and quicker new drug approvals. This bodes well for innovative companies with healthy development pipelines that are well positioned to bring products to market at a faster rate than in years past. Biotechnology and pharmaceutical companies remain relatively inexpensive by historical standards in comparison to the market. This combination of factors may provide attractive investment opportunities in 2018.

Energy

Worldwide oil inventories continued to fall in 2017 and demand was stronger than originally forecast – a combination that supported oil prices. The Organization of Petroleum Exporting Countries has decided to extend its quota agreement through 2018, and we think inventories will continue to fall and prices will get further support. In general, we also expect steady global economic growth to continue in 2018, further contributing to the growth in oil demand. The market is likely to be heavily influenced by the supply fluctuation of U.S. shale oil, which can come online more quickly than other production methods.

We also believe that rising oil prices will be a tailwind to revenue growth for energy companies during the year. In addition to these fundamental factors, the market will contend with unpredictable factors that could affect global supply and prices. These include:

- Saudi Arabia: An anti-corruption purge led by the heir to the throne that may signal a consolidation of royal power, a planned initial public offering of Saudi Aramco shares in late 2018, and escalating tensions with Iran and Shiite rebels in Yemen.

- Nigeria: The threat of renewed terrorist attacks on facilities in the main oil-producing region of the country with a resulting loss of market supply.

- Venezuela: A worsening economic crisis that has resulted in a default on two bond issues, increasingly authoritarian leadership and a steady decline in crude oil output and revenue.

Other areas to watch

Past performance is not a guarantee of future results.

Investment return and principal value will fluctuate, and it is possible to lose money by investing. International investing involves additional risks, including currency fluctuations, political or economic conditions affecting the foreign country, and differences in accounting standards and foreign regulations. These risks are magnified in emerging markets. Investing in the energy sector can be riskier than other types of investment activities because of a range of factors, including price fluctuation caused by real and perceived inflationary trends and political developments, and the cost assumed by energy companies in complying with environmental safety regulations. These and other risks are more fully described in a Fund’s prospectus.

The opinions expressed are those of Ivy Investment Management Company, are current through December 2017 and are subject to change at any time based on market and other current conditions. No forecasts can be guaranteed. This information is not a recommendation to purchase, sell or hold any specific fund or security mentioned or to engage in any investment strategy. Funds or securities discussed may not be suitable for all investors.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All