Few things in this world can be predicted with accuracy over multiyear periods and fewer still over multidecade spans. One exception is population demographics. Based on data today, we have a good idea how populations will develop through 2050. For some countries, demographics will provide a tailwind toward possibly robust economic growth in the coming years. Others, such as the United States, face a headwind, but not an insurmountable one. For one unfortunate group, however, demographics will disrupt current conditions and present myriad challenges to policy makers. Interestingly, challenges can arise from a rapidly growing population as well as from a shrinking one. In this note we will examine the potential disruption from population changes in Japan and the Middle East.

Make That the Setting Sun

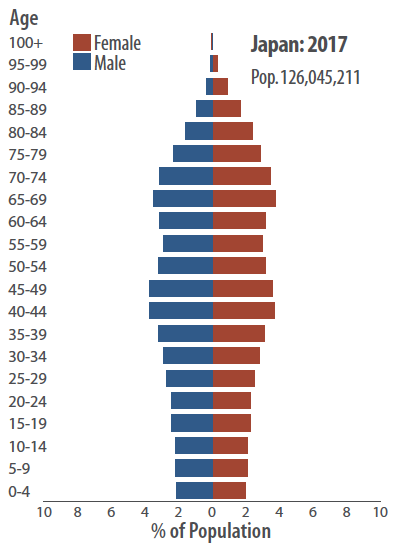

Japan and Europe feature aging populations that will decline over the coming decades. For example, in 2016 Finland experienced the lowest number of live births in 148 years, since the end of the great famine of 1866-1868, which reduced the population by 15%.1 While a remarkable and disconcerting statistic, Japan is the poster geriatric for this phenomenon. Its population is estimated to have peaked at 128.5 million in 2010 and, as of September 2017, had fallen to 127 million, shrinking at an annual rate of -0.21%.2 The Japanese government projects the population will decline to 117 million by 2030 and 97 million by 2050.3 As a result of the distribution of Japan's age cohorts, its population "pyramid" is anything but.4

There are two significant issues arising from Japan's population structure. First, consistent economic growth becomes difficult to sustain, being a function of labor force and productivity. The latter would have to increase dramatically to overcome population declines averaging -0.8% annually and an even faster erosion of the working age population. Second, Japan's dependency ratio will soar as fewer workers are available to support a growing number of retirees. The scale of the problem dwarfs anything the US faces with Social Security. Through 2050 the US population is anticipated to expand 19% to 388 million, while Japan's population shrinks 23%! When we consider that Japan already labors under a public debt burden equivalent to 235% of its GDP,5 by far the largest in the world, one rightly wonders how the country can ever dig itself out of this mess.

Two potential solutions are often suggested, with the first being increased participation of Japanese women in the labor force. The talents of Japanese women are irrefutably underutilized in the economy, and the female labor participation rate of 49% stands below the 56% rate in the US. Still, it's just below the 50% rate seen in the euro area6 so we cannot expect too much help there. Immigration is often suggested as another solution, but in ethnically and culturally homogenous Japan, "Immigration remains deeply unpopular…according to public opinion polls."7 In 2012, Japan introduced a Highly Skilled Foreign Professional (HSFP) visa program, but the 2,642 visas issued in 20158 will hardly address the issue. Japan is probably the one country in the world where labor-replacing automation is seen as a positive. It is definitely seen as preferable to large increases in immigration.

Given these developments, it appears obvious that certain industries will be disadvantaged. Any company involved in domestic retail, processed foods, or consumer goods will have difficulty maintaining sales in an environment of ever fewer consumers. How do telecommunications companies grow revenue when the number of people speaking on the phone, sending text messages, or streaming video declines by one million annually over the next three decades? Equally, it’s hard to imagine real estate providing attractive returns. Ignoring the potential disruptions of automated driving and the sharing economy, the automotive companies will face challenges. In the financial year ended March 2017, Toyota derived 25% of its sales and, due to high margins, 60% of its operating income from Japanese activities.9 Admittedly, a portion of the sales and income were generated by exports. Regardless, Toyota holds a 46% share in the Japanese car market (excluding mini vehicles)10 and is captive to reductions in market size.

Silver linings? Anyone seeking employment will have little difficulty finding it. Certain industries, such as health care, may benefit. Japan’s population is aging more quickly than it’s shrinking, so health care expenditures will rise with a large bulge in the 65-75 age cohort. Eventually, they will depart the scene, but Japan’s largest group is in the 40-50 cohort, and their spending will start to increase just as it’s ending for the earlier group.

As alluded to above, industrial automation companies are another potential beneficiary. Japan’s unemployment rate already stands at a low 2.8%.11 With the accelerating labor force decline, any innovation that replaces a human worker will be readily embraced.

Perhaps the greatest mystery is what will happen to the currency; an important point given that the Japanese stock market has shown an inverse correlation with the strength of the yen over the past several years. One would normally consider a shrinking population and minimal economic growth to be a recipe for deflation. On the other hand, staggering debt levels and a need for the Bank of Japan (BoJ) to create money out of thin air to support the growing raft of retirees implies inflationary pressure. Despite the deflationary real environment, we have not been able to wrap our minds around how the BoJ and the Japanese government can continue to operate unless they ultimately absolve trillions of US dollars' worth of government debt while printing money — and not have those actions lead to currency depreciation and concomitant domestic inflation. Interestingly, Japanese homogeneity and the fact that nearly all of the debt is held domestically may provide an avenue for netting off exposures and containing the problem.

Now for Something Completely Different

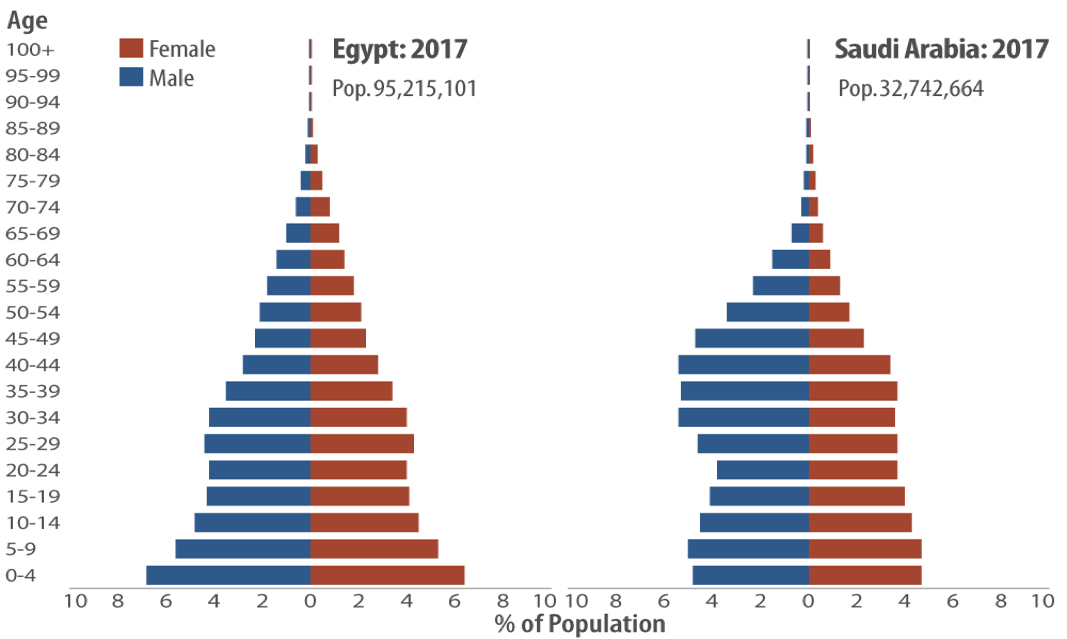

While Japan grapples with its emptying isles, other parts of the world are experiencing explosive population growth, notably the Middle East. Below we provide the population pyramids for Egypt and Saudi Arabia. Through 2050 their populations are anticipated to grow 59%, and 41%, respectively. In some circumstances, such a demographic outlook would be cause for celebration, with a rapidly expanding labor force and a tiny pool of retirees. Unfortunately, Saudi Arabia depends on a single commodity to drive economic activity and fill government coffers, while Egypt has been a study in economic mismanagement. Let’s start there.

Last November the International Monetary Fund (IMF) approved a $12 billion bailout for an Egyptian economy that "...faces both urgent and long-standing structural challenges."12 Apart from the IMF contribution, Egypt relies on significant aid from a variety of countries, including the US and Saudi Arabia. Not only does Egypt import money, it also imports a significant quantity of its food, with much of it coming from Turkey. Indeed, Egypt is among the countries most dependent on food imports. Egypt also suffers from budget deficits as high as 12% of GDP, a public debt to GDP ratio of 103% and an unemployment rate of 13%.13

The Egyptian government has made efforts to respond to its economic challenges. In 2015 an expansion of the Suez Canal was completed with the expectation that it would lead to a significant increase in revenue over the roughly $5 billion the canal had been earning previously. Unfortunately, that has not been the case to date and revenue has hardly changed. Despite the slow progress, the Suez Canal expansion was a reasonable investment. Less impressive, in August the Egyptian government announced a plan to establish a new space agency so that the country can launch satellites to search for resources in the Egyptian desert.14 There’s nothing wrong with developing a space capability. In the 1960s the US effort to land a man on the moon spurred the development of multiple industries. In the US, however, the space race was powered by an army of scientists, engineers, and technical personnel supplied by a highly developed education system. In the 2016-2017 Global Competitiveness Report, Egypt ranked 112th out of 138 in higher education and training and 115th in overall competitiveness.15 The point here is not to denigrate Egypt. Rather, it's to demonstrate a country ill-prepared to absorb the 20-40 million people (depending on female participation) entering the labor force over the next 20 years, as much as 40% of the current population.

Absent a sea change in the quality of the authoritarian military leadership, the outlook appears cloudy. We can take comfort from Egypt's ancient history and strong sense of nationhood, unlike several other Middle Eastern countries that emerged after World War I as a result of the Sykes-Picot Agreement.16 Still, the risks are considerable in a country that has already seen two changes of government, including a military coup, since the Arab Spring in 2011.

The investment themes that arise from the challenges facing Egypt are tangential rather than direct. Egypt is not a major oil producer, and disruption in the country would not affect production but could affect transport and pricing given the importance of the Suez Canal. Failure by the Egyptian government to meet the needs of its rapidly growing population could lead to a breakdown similar to Syria. At 96 million, however, Egypt's population is roughly five times the size of Syria's. What could that mean in terms of refugee pressure on Europe and the potential for a dramatic strengthening of rightist political parties there?

We are also reminded of the importance of the environmental factor in ESG investing. Many issues contributed to the emergence of the Arab Spring but among them were sharply higher food prices resulting from poor harvests. A rising global temperature is nothing but bad news for the Middle East, potentially exacerbating Egypt's food import requirements. There’s a reason the Pentagon issued a report identifying the specific climate change and environment-related threats facing the various geographic combatant commands.

Saudi Arabia faces a different challenge from Egypt; arguably more cultural than economic. The country is fabulously wealthy with a GDP per capita comparable to the US, but oil contributes 90% of government revenue,17 unemployment among Saudi nationals hovers at a high 12%, and employment opportunities are limited, from a psychological if not practical perspective. Roughly two-thirds of Saudi nationals work for the government in positions that are often little more than sinecures. The good news for Saudi Arabia is that in the private sector some 85% of employees are foreign nationals.18 These people assume jobs Saudis are not willing or qualified to take. Demographic reality may change that calculation in future. Saudi Arabia's advantage is that it recognizes the challenge and has the resources to take action. Crown Prince Mohammad bin Salman (MBS), has initiated a program, Vision 2030, designed to develop sectors of the economy that can absorb employment and replace oil as the Kingdom’s economic driver. Managing such a transition will be difficult, as illustrated by a government decision to reverse budget cuts and reductions in salary and benefits for government employees at the same time as announcing that the 31-year-old MBS was replacing his 57-year-old and more senior uncle as Crown Prince.

Weaning the Saudi economy from oil, changing the domestic population's mindset regarding private sector work, navigating religious objections, and developing a modern, diversified economy will be mind-bogglingly difficult, but Saudi Arabia has identified the goal and has the resources to pursue it. Does it have the will? It sounds insignificant and certainly anachronistic, but the announcement in early October that it will permit women to drive is an intriguing first step. More dramatic were the recent moves by the government to place a number of high-ranking Saudi officials, members of the royal family and business tycoons under "house arrest," if it can be called that when you're reportedly being held at the Ritz-Carlton Hotel. Whether aggressive or reckless (Saudi actions in Yemen, Qatar, and Lebanon — all part of the struggle between Saudi Arabia and Iran to dominate the region — argue for the later), MBS is staking his claim to consolidate power and achieve a free hand in the remaking of the Saudi economy and society. Succeed or fail, we are witnessing a seminal moment in modern Saudi history.

From an investment perspective, Saudi Arabia's moves to wean itself from oil represent sensible diversification but also tell us something about their own view of the outlook for oil; a view supported by the planned, although delayed, listing of a portion of Saudi Aramco, the national oil company. Exogenous shocks aside, it's possibly the top of the market. American shale oil and natural gas production are holding down prices. The Paris Agreement, signed by every nation in the world except the United States, will strive to lower carbon emissions, which implies lower fossil fuel consumption. Wind and solar power are becoming more price competitive, while improved batteries address the issues of calm days and dark nights. Countries are setting deadlines for the phaseout of internal combustion engines, and all vehicle manufacturers are developing alternative drive train — mostly electric — vehicles. The Saudis may be making the clearest argument yet about the long-term outlook for oil.

---------

Footnotes

¹ Tiessalo, Raine. Finland's Welfare State Has a Massive Baby Problem. Bloomberg, September 18, 2017. https://www.bloomberg.com/news/articles/2017-09-19/finland-s-welfare-state-has-a-massive-baby-problem

² Japan Population, Worldometers.com http://www.worldometers.info/world-population/japan-population/

³ Traphagan, John W. Japan’s Demographic Disaster, The Diplomat, February 3, 2013. http://thediplomat.com/2013/02/japans-demographic-disaster/

4 Japan 2017, PopulationPyramid.net. https://www.populationpyramid.net/japan/2017/

5 Public Debt, Country Comparison to the World, The World Factbook, Central Intelligence Agency. https://www.cia.gov/library/publications/the-world-factbook/fields/2186.html#ja

6 Labor force participation rate, female (% of female population ages 15+), International Labour Organization, ILOSTAT database, The World Bank. https://data.worldbank.org/indicator/SL.TLF.CACT.FE.ZS

7 Green, David. As Its Population Ages, Japan Quietly Turns to Immigration, Migration Information Source, March 28, 2017. http://www.migrationpolicy.org/article/its-population-ages-japan-quietly-turns-immigration

8 Ibid.

9 Toyota Motor Corporation Fiscal Year 2017 Financial Results, May 10, 2017. http://www.toyota-global.com/pages/ contents/investors/financial_result/2017/pdf/q4/presentation.pdf

10 Japan – Flash report, Sales volume, 2016, MarkLines Information Platform. https://www.marklines.com/en/statistics/ flash_sales/salesfig_japan_2016

11 Japan Unemployment Rate 1953-2017, Trading Economics. https://tradingeconomics.com/japan/unemploymentrate

12 A Chance for Change: IMF Agreement to Help Bring Egypt’s Economy to Its Full Potential, IMF News, International Monetary Fund, November 11, 2016.

13 Egypt Economic Outlook, Focus Economics, October 3, 2017. http://www.focus-conomics.com/countries/egypt

14 Michaelson, Ruth. Egypt’s Economy Is in Crisis. So Why Is the Government Spending Millions on a Fancy New Space Agency?, Newsweek, February 28, 2017. http://www.newsweek.com/2017/03/10/egypts-economy-crisis-government-spending-millions-new-space-agency-561743.html

15 Schwab, Klaus. The Global Competitiveness Report 2016-2017, World Economic Forum. http://www3.weforum.org/docs/GCR2016-2017/05FullReport/TheGlobalCompetitivenessReport2016-2017_FINAL.pdf

16 Muir, Jim. Sykes-Picot: The map that spawned a century of resentment, BBC News, May 16, 2016. http://www.bbc. com/news/world-middle-east-36300224

17 Dorfman, Jeffrey. Saudi Government Proves Basic Income Is No Solution To Slow Economic Growth, Forbes, October 3, 2016. https://www.forbes.com/sites/jeffreydorfman/2016/10/03/saudi-government-budget-cuts-prove-basicincome-is-no-solution-to-slow-economic-growth/#7604e7424bbe

18 38% drop in private sector Saudi employment, Arab News, January 16, 2016. http://www.arabnews.com/featured/news/865861

Important Disclaimers and Disclosures

Investing involves risk, including the risk that you may lose money. Active investing does not assure a profit in a rising market or protect against a loss in a declining market. Please consider an investment’s objectives, risks, charges, and expenses carefully before investing. For this and other important information about Saturna's funds, please obtain and carefully read a free prospectus or summary prospectus from your financial adviser, at www.saturna.com, or by calling toll-free 1-800-728-8762.

This material is for general information only and is not a research report or commentary on any investment products offered by Saturna Capital. This material should not be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. To the extent that it includes references to securities, those references do not constitute a recommendation to buy, sell or hold such security, and the information may not be current. Accounts managed by Saturna Capital may or may not hold the securities discussed in this material.

We do not provide tax, accounting, or legal advice to our clients, and all investors are advised to consult with their tax, accounting, or legal advisers regarding any potential investment. Investors should not assume that investments in the securities and/or sectors described were or will be profitable. This document is prepared based on information Saturna Capital deems reliable; however, Saturna Capital does not warrant the accuracy or completeness of the information. Investors should consult with a financial adviser prior to making an investment decision. The views and information discussed in this commentary are at a specific point in time, are subject to change, and may not reflect the views of the firm as a whole.

It should be noted that ESG or socially responsible investing is not without risk. Like any investment, the prices of securities that score well in ESG or sustainability metrics can fluctuate, sometimes significantly, for a broad variety of reasons. By limiting the universe of investment options through both positive and negative screening, it is possible to miss out on the performance of certain sectors, industries, or securities – and this can be outperformance or underperformance.

Any data on past performance, modelling or back-testing contained herein is not necessarily indicative of future results. All levels, prices and spreads are historical and do not represent current market levels, prices or spreads, some or all of which may have changed. The information referenced herein or any of the results derived from any analytic tools or reports referenced herein are not intended to predict actual results and no assurances are given with respect thereto. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity).

All material presented in this publication, unless specifically indicated otherwise, is under copyright to Saturna. No part of this publication may be altered in any way, copied, or distributed without the prior express written permission of Saturna.

Copyright 2017 Saturna Capital Corporation and/or its affiliates. All rights reserved.

Read more commentaries by Saturna Capital