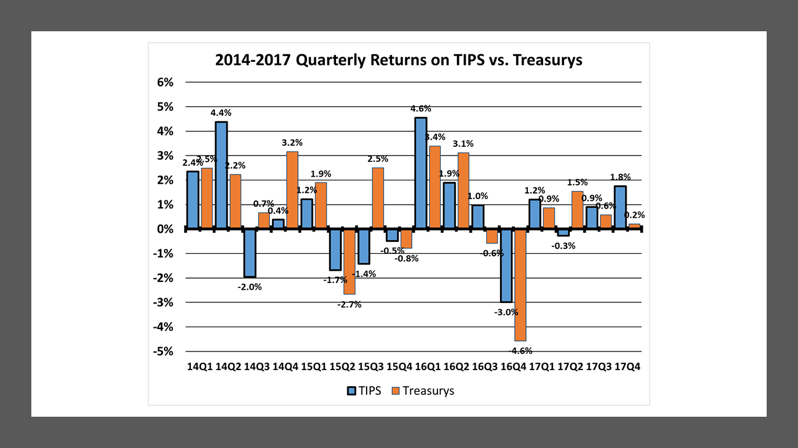

TIPS Outperform Straight Treasurys in the 2017 Fourth Quarter

TIPS finished the year with a very strong performance, their best since the 2016 second quarter. For the 2017 fourth quarter, TIPS posted a total return of 1.8%, much better than the 0.2% on comparable maturity straight Treasurys. This was also TIPS’ strongest quarterly performance of the year. During 2017, TIPS posted gains in three of the four quarters, recording a loss of 0.3% only in the 2017 second quarter.

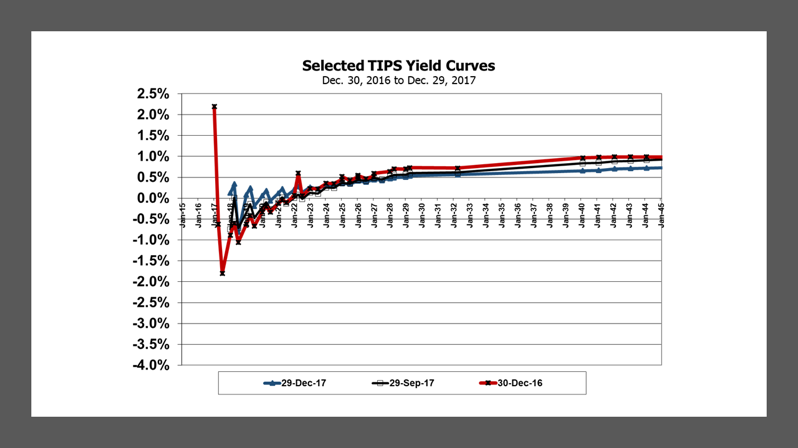

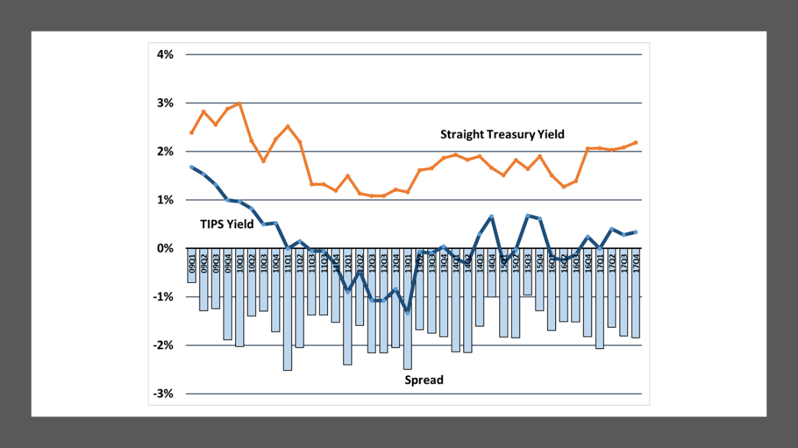

As with straight Treasurys, the TIPS yield curve flattened in 2017. Short-maturity TIPS increased in yield, rising from negative to positive levels. Longer maturity TIPS, meanwhile, declined in yield. In fact, the decline in long maturity TIPS drove 2017 fourth quarter returns and was the primary reason for TIPS’ outperformance in the fourth quarter.

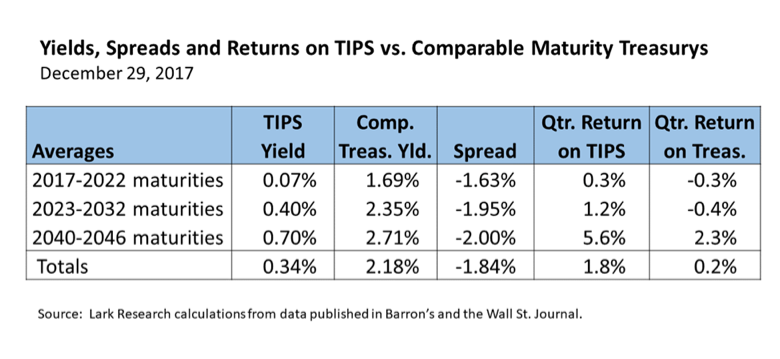

2017 Fourth Quarter Returns. From the 2017 third to fourth quarters, the average TIPS yield (across) all maturities increased by seven basis points from 0.27% to 0.34%, while the average yield on comparable maturity Treasury securities increased ten basis points from 2.08% to 2.18%. As a result, the average breakeven spread widened by three basis points to 184 basis points.

The change in TIPS yields varied across maturities. Short-term TIPS yields increased by 28 basis points from -0.21% to +0.07%. Intermediate-term TIPS yields were little changed at 0.40%. But long-maturity TIPS yields declined by 19 basis points to 0.70%. That decline in long maturity TIPS yields helped drive a 5.6% annualized return on long maturity TIPS for the quarter, which was the primary catalyst in the asset class’s superior performance (vs. straight Treasurys).

Meanwhile, comparable maturity straight Treasurys posted negative returns in the short- and intermediate-term maturities. But like TIPS, long-term Treasury securities posted solid gains – with annualized returns of 2.3% for the 2017 fourth quarter. That helped straight Treasurys post a positive return of 0.2% in the quarter. Without the strong performance in long-term Treasurys, returns for straight Treasurys would have been negative in the quarter.

As noted the increase in the yield spread between TIPS and straight Treasury was modest and the spread remained well within recent historical averages. The current spread is perhaps a sign of expectations that inflation will remain below 2% for the foreseeable future. Investors who believe that CPI inflation will turn out to be lower than the current average spread of 184 basis points would earn higher returns by holding comparable maturity straight Treasurys.

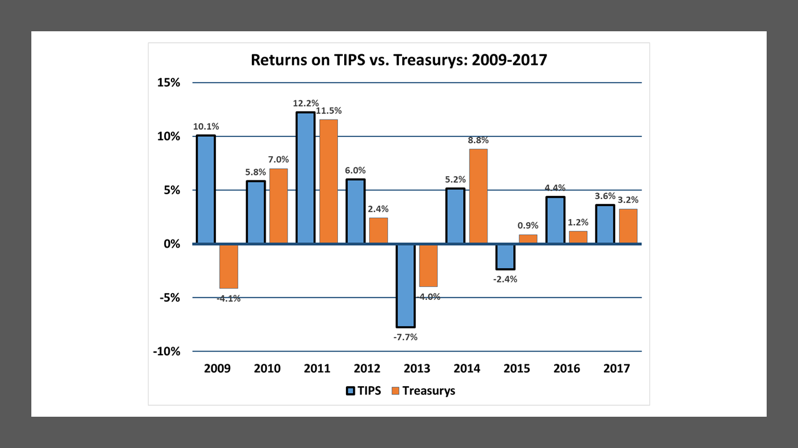

TIPS vs. Treasurys: Annual Returns for 2016. Despite the strong 2017 fourth quarter returns, total returns for TIPS were lower in 2017 than in 2016. For the full year, TIPS returns were 3.6% in 2017, down from 4.4% in 2016. On the other hand, total returns on comparable maturity straight Treasury securities increased from 1.2% in 2016 to 3.2% in 2017. Most of the returns for straight Treasurys were realized in the first half of the year. TIPS outperformed straight Treasurys for the second consecutive year.

Outlook. The spread between the 10-year Treasury Notes yield and the 2-Year Treasure Note yield narrowed from 128 basis point when the Fed began normalizing interest rates in December 2015 to only 51 basis points at the end of 2017. However, the 10-year Treasury note yield has increased by 15 basis points so far in 2018, and the 10-year-to-2-year spread has widened to 57 basis points. Unless long-term Treasury yields continue to rise, the Federal Reserve may slow down the pace of interest rate normalization (as long as inflation remains at or below its target 2% rate) out of concern of inverting the U.S. Treasury yield curve.

If, on the other hand, a rise in long-term interest rates is accompanied by a pick-up in inflation, TIPS will likely outperform straight Treasurys again in 2018; but TIPS total returns may be low or even negative, especially if the pace of increase in straight Treasury yields picks up.

Stephen P. Percoco

Lark Research

839 Dewitt Street Linden, New Jersey 07036 (908) 448-2246

[email protected]

www.larkresearch.com

Lark Research is an independent investment research provider founded by Stephen P. Percoco in 1991. Research coverage includes stocks and bond in industries such as real estate, utilities, oil & gas, telecommunications, industrials, consumer goods and materials. Prior to founding Lark Research, Steve served as Vice President in High Yield Corporate Bond Research at Salomon Brothers and as an investment officer at Bank of Boston. He is a graduate of Bowdoin College and Harvard Business School.

© Lark Research

Read more commentaries by Lark Research