As we approached the holiday season (which seems to start even before Thanksgiving now), I did a quick survey around the office to confirm what I already expected, there were no must-have, stand-in-line, drive hours to buy toys in play this holiday season. I breathed a sigh of relief knowing that there would be no standoffs for a GI-Joe with Kung-Fu grip or shouldering aside someone’s grandmother for the last Nintendo Wii.

These consumer crazes happen every few years and are not, as some may expect, always a sign of booming times. In fact, some appeared at the direst moments for consumers. Shirley Temple dolls and Monopoly boards flew off the shelves during the great depression in the 1930s while Chatty Cathy dolls were all the talk during the recession of 1960.

Investment fads, like consumption fads, are also sometimes asynchronous with the economic landscape. These mini-manias pop up all the time but they tend to grab our attention more when there are echoes of past bubbles in the ether. The most baffling side of these manias is not the validity of the underlying idea, but the market reaction to immaterial cosmetic nuance. Case-in-point, company names. Many are aware of the phenomenon during the dot-com era of companies adding “.com” or “internet” to their name (that had nothing to do with web) and immediately getting a share price bump. What many do not know is that companies also got the same type of share price bump from removing “.com” or “internet” from their names during the subsequent burst.

Recently we have had a few examples (we quickly reference blockchain here but will be writing a more extensive piece in the coming weeks):

- Ripple, another burgeoning cryptocurrency, rose from 23 cents per coin to nearly $3 in a matter of one month, making its founder temporarily richer (on paper) than Mark Zuckerberg (and number five on the Forbes top billionaires).

- Long-Island Ice Tea Corporation added “blockchain” to their name and stock jumped nearly 500%.

- Kodak (yes, the 130-year-old photo company) announced they will use KodakCoin (its own cryptocurrency) and the stock immediately rose 60%.

- Canadian miner Kairos Capital (which already had lithium assets) sent out a proxy to change its name to Lithium Chile and stock rose nearly 100% in a week.

But as we mentioned earlier, these mini-manias pop up all the time. Leveraged closed-end municipal bond funds were all the rage in the early 1990s, but investors forgot to pay attention to premiums to net asset value and lost billions.

Solar and rare-earth metal companies were the darlings of Wall Street and amongst the select few industries which could access capital markets immediately after the great recession. Many an IPO or renaming began to include "solar" in the name. Within five years, there was a sizable bust for a large portion of the operators. For context, the MAC Global Solar Energy Index is down more than 75% from 2010 through 2017, while the MVIS Global Rare-Earth Metals Index is down 33% over the same period.

Pokémon GO anyone? For a period, this fad resulted in sometimes tragic consequences for people not watching where they were going. Nintendo’s stock rose more than 50% in very short order because investors believed in the phenomenon. Unfortunately, many did not read the small print in that Nintendo only had a minority ownership stake in the game and had already accounted for those revenues in its latest assumptions (stock fell 30% in short order). The up and down of Nintendo moved more money than all the stocks which recently decided to add "blockchain" to their name combined.

What is important is that mini-manias do not invalidate the fundamentals of the underlying idea, that is only evident in hindsight.

- “Fooling around with alternating current (AC) is just a waste of time. Nobody will use it, ever.” — Thomas Edison, 1889

- "Television won't be able to hold on to any market it captures after the first six months. People will soon get tired of staring at a plywood box every night." - Darryl Zanuck, 20th Century Fox, 1946

- “There’s no chance that the iPhone is going to get any significant market share.” — Steve Ballmer, Microsoft CEO, 2007

It is important to separate mini-manias from true bubbles. Unfortunately, the difference is mostly the amount of money chasing the folly. Millions and even billions of dollars lost (and thousands of jobs) equate to fads, while trillions of dollars lost (and rampant unemployment and recessions) are bubbles.

Economic historian and author Charles Kindleberger spent a great deal of time studying the anatomy of these types of events, from the Dutch Tulip frenzy, to the South China Sea Bubble, to Japanese Real Estate, and many more. Kindleberger’s work, along with economist Hyman Minsky’s financial instability hypothesis, yield an anatomy of a true market bubble. It starts with displacement, then boom, euphoria, crisis, and finally, revulsion.

- Displacement occurs when investors get excited about something new (invention, war, economic policy, monetary policy, trade policy, etc.). It is based on something disruptive such as railroads, telegraphs, automobiles, planes, fiberoptic lines, internet, etc. It should be noted that when displacement is driven by true fundamental factors, there are tangible benefits to the economy post boom-bust. For example, we grow into overbuilt infrastructure.

- Boom is after narrative forms around displacement, where price becomes a secondary consideration. This is often met with significant leverage/borrowing, and loose lending practices.

- Euphoria is when everyone jumps in; prices rise exponentially.

- Crisis begins when original investors begin to trim/sell, prices decline, leading to pessimism and subsequently a crash.

- Revulsion occurs when prices overshoot to the downside and through the fundamental value.

There are signs of some of these characteristics in many of the mini-manias of today. However, they must be understood in context. Manias of the 1600s, 1700s, 1800s, early 1900s are quite relevant from a behavioral standpoint, but should also be viewed with a “what if?” mindset. One consideration is what Kindleberger and others called the Hegemonic Stability Theory. It postulates that bubbles are less likely to generate prolonged destruction when there is a single nation-state able to act as a backstop. In the world today, the hegemon is a coordinated and global central banking system. In that context, what if there was a Fed, before the great depression, that flooded the system with money rather than let deflation run amuck. Would it have taken us a decade to get out of the great depression? The more recent bubbles (housing, .com, etc.) are better examples of the possibilities, but after each one, the backstop has gotten taller. We would note that we are not proponents of the moral hazard created by the ever-growing safety net, which incentivizes inappropriate risk-taking behavior. Yet, at least for now, a better alternative has not been accepted by world economies.

Markets

Source: Morningstar, Bloomberg

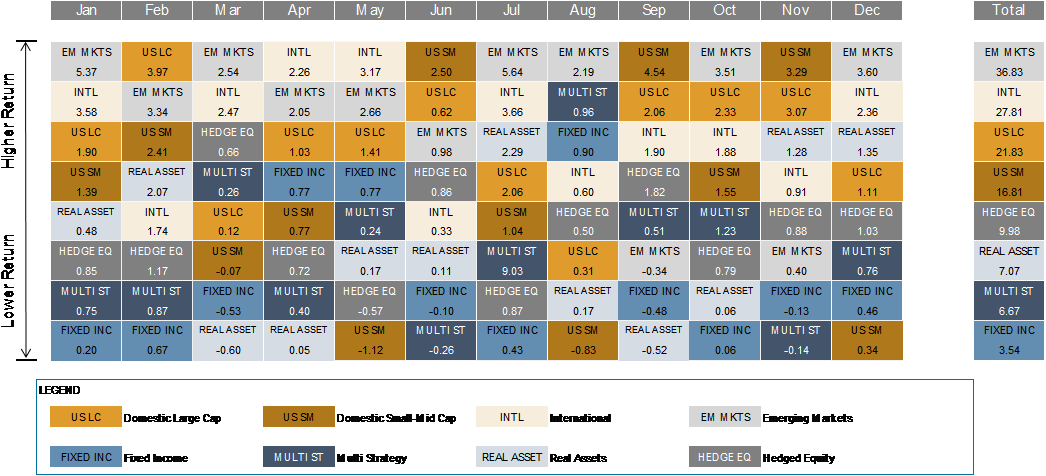

Geopolitical headlines did little to deter investors in Q4 and for the entirety of 2017. The world economy grew at 3% in 2017, the highest since 2011. Earnings rose strongly across the globe, helping equities generate double digit returns. In the US, the trend of growth beating value and low dividend yield beating high continued. US dollar weakness supported non-US assets for most of the year, with the dollar declining roughly 9% in 2017.

US large company stocks (represented by the S&P 500 Index) rose 6.6% for the quarter. US small-mid company stocks (represented by the Russell 2500 Index) rose 5.2%. International stocks (represented by the MSCI ACWI ex US IMI Index) also rose 5.2% and Emerging Market stocks (represented by the MSCI EM IMI Index) rose 7.7%. No developed nation fell by more than 5% in Q4, and all rose by more than 10% for the year.

The Fed raised interest rates three times in 2017 and expectations are for another three in 2018, helping savers finally generate some return on their cash. The Barclays Capital US Aggregate Bond Index rose 0.4% in Q4, bringing YTD returns to 3.5%. The yield on the 10-Year Treasury rose only slightly in Q4, and finished the year 4 bps below the starting point. Municipal bonds (represented by the Barclays Muni 1-10 Year Index) fell 0.2% for the quarter, thanks in part to significant issuance ahead of the tax bill, but still finished up 3.5% for the year.

Alternatives continued to plod along in Q4. Multi-strategy funds (represented by the HFRI FoF Diversified Index) rose 1.9% for the quarter. Hedged equity managers (represented by the HFRX Equity Hedge Index) rose 2.7%. REITs in the US finished up 1.5%, but abroad they rose more than 6.4%. Global Infrastructure returned 0.3%, thanks again to strong performance in Europe and Japan, though a negative return in US energy infrastructure was a headwind. Commodities posted a very strong 4.7%, bringing calendar year returns into positive territory, thanks to strong performance from industrial metals and select petroleum derivatives.

Looking Ahead

- January – World Economic Forum in Davos, Switzerland

- February – Janet Yellen’s term as Fed Chair ends; Winter Olympics begin in Peyongchang, South Korea

- March – First round of Russian elections (Putin expected to run for 4th term, and even without any US collusion, he will win)

- April – Bank of Japan Governor Haruhiko Kuroda’s term to end, though many expect he will serve again

- May – Italy to hold general election

- June – World Cup begins in Russia

- July – Mexico to hold general election

- August – Greece’s bailout expires; Malaysia and Pakistan to hold general elections

- September – United Nation General Assembly to be held in New York

- October – EU’s target date to complete Brexit deal (UK expected departure in 2019); Brazil to hold general election

- November – US midterm election with 435 House seats and 33 Senate seats up for grabs

- December – SpaceX plans first private citizen flight; Finland will experiment with Universal Basic Income (will pay 2,000 citizens roughly $665 per month)

Bronfman E.L. Rothschild is a registered investment advisor (dba Bronfman Rothschild). Securities, when offered, are offered through an affiliate, Bronfman E.L. Rothschild Capital, LLC (dba BELR Capital, LLC), member FINRA/SIPC.

This information should not be construed as a recommendation, offer to sell, or solicitation of an offer to buy a particular security or investment strategy. The commentary provided is for informational purposes only and should not be relied upon for accounting, legal, or tax advice. While the information is deemed reliable, Bronfman Rothschild cannot guarantee its accuracy, completeness, or suitability for any purpose, and makes no warranties with regard to the results to be obtained from its use. Past performance does not guarantee future results.

© 2018 Bronfman Rothschild

Read more commentaries by Bronfman E.L. Rothschild