What a difference a year makes. It is hard to recall but at the turn of calendar to 2017 investors were debating whether stronger economic growth would ever return, largely because it had been so weak for much of late 2015 and 2016. Indeed, even as consumer and business confidence surveys were pointing to a brighter future, many investors were losing patience waiting for them to be reflected in strong “actual” economic growth. Indeed, the debate on Wall Street became whether the historical link between “soft” survey or feelings based data and actual “hard” bean-counting economic growth (Gross Domestic Product -GDP) was broken.

We expressed our belief that soft data surveys had earned the right to be called leading economic indicators because they had historically lead the hard data. Put more simply, before you “actually” act, you must “feel” confident first. And right on cue economic growth over the past three quarters has accelerated. After back to back 3% plus quarter over quarter real economic growth in Q2 and Q3, the U.S. economy looks set to post 3% plus Q4 growth. This would mark the first time since late 2004 that the U.S. economy has posted three consecutive 3% plus quarters in a row.

And this growth expansion has occurred before tax reform has taken hold. While much of the current tax reform chatter revolves around the intermediate to longer term outcome, we believe that argument is highly subjective because the economic models that are being used to moderate the discussion, have high margins of errors. Allow us to focus on the more precise, nearer term effects of this bill. Put simply, it is fiscal stimulus. And this stimulus is occurring at a time when future indicators of growth already look rather robust.

If the return of stronger economic growth was the big surprise story of 2017 after a period of weakness in the prior years led many to doubt its return, we believe the return of inflationary pressures that will eventually result from this growth will become the big surprise story of 2018; again, against a substantial wall of doubt.

What are inflation indicators telling us?

While many economic variables behaved consistent with rising economic growth in 2017, the one variable that has defied logic has been inflation. Indeed, after spending 2016 recovering from its oil/commodities induced fall, surprisingly core measures of consumer price inflation (CPI) have fallen for much of 2017. This has led many to question whether inflation is a relic of the past and that this time is different.

Forgive if we are having a bit of Deja vu. We believe this debate feels a lot like last year’s economic growth argument. We note that many leading measures of inflation are currently pointing to a high likelihood of rising price pressures in 2018. However, due to the lack of its arrival in the actual hard data measures of inflation (think actual CPI) many are growing impatient and suggesting the link is broken. Allow to again express our disagreement.

Inflation is a lagging indicator. Today’s overall inflation levels tell you a story of what happened 12-18 months ago; a period when the global economy was just emerging from a weak period of growth caused by a supply driven oil war that knocked manufacturing and trade into near recession like conditions. Now with U.S. and global manufacturing rapidly accelerating, global trade humming and the U.S. and global consumer remaining strong, we believe that future inflation looks set to move higher.

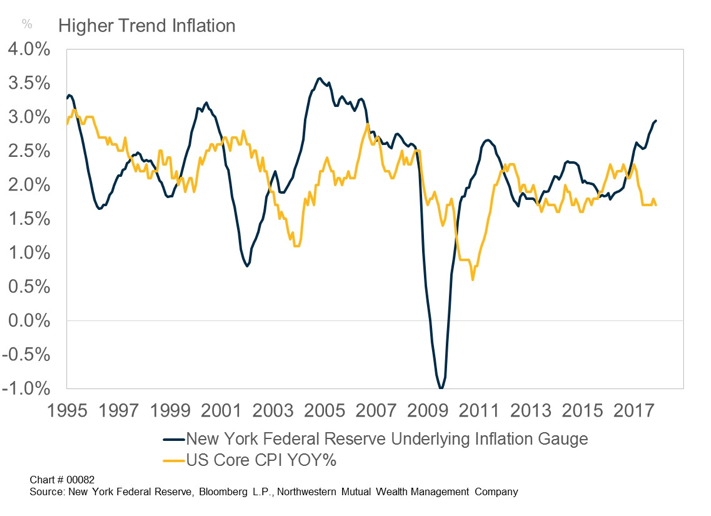

Inflation is a volatile data series and economists are interested in separating shorter-term noise from intermediate term trend. With this goal in mind, The Federal Reserve Bank of New York has built an Underlying Inflation Gauge (UIG) that contains many leading indicators of trend inflation. And despite the overall declining inflation in 2017, the UIG continued to moved higher throughout the year and rose to a post Great Recession high. Based upon its past relationship that shows its leads Core CPI – the UIG points to rising future inflation in 2018.

Is this Cycle Unique?

While many continue to state that this expansion is extremely unique, we believe they are ignoring history. Indeed, a review of the 1960’s reveals many similarities to today’s environment. Most importantly, inflation in the early 1960’s was extremely low. From 12/1958 to 2/1966 on every measured month, Consumer Price Inflation (CPI) was below 2%. The Federal Reserve responded to this first with low short-term interest rates and then in 1961 they embarked on Operation Twist (Quantitative Easing) with a goal of pushing long term rates low.

As a result, U.S. bond yields resided at low levels and stocks were priced at high price to earnings multiples. In 1965 realized equity market volatility in hit all time low levels. Further reflecting complacency, according to a research paper written by Harvard Professor Paul Schmelzing, “observers in 1965 were trapped in a lower for longer inflation rate consensus belief”.

If that sound similar it should. For much of the past eight years the Fed has missed their 2% inflation target. Responding to this, the Federal Reserve has held down short-term interest rates and performed numerous iterations of Quantitative Easing, including Operation Twist II, to push down long term rates. Thus, bond yields reside at low levels (on some measures not seen since the early 1960’s) and equity markets trade at high price to earnings multiples. Realized equity market volatility during the 4th quarter hit the lowest level since you guess it -1965. Furthermore, the difference between the high and low 10- year Treasury yield was the narrowest in 2017 in any given year going back to 1962. And importantly, the current conventional wisdom, almost to the point of absolute certainty, remains lower for longer with regards to inflation and interest rates.

What happened next you ask? Inflation finally arrive in early 1966. This caused a bond market hiccup that lead to a short but sharp equity market correction. Indeed, after a 20% drop during the summer of 1966, the equity market shifted coursed and recovered all its loses by the spring of 1967. And much like we would forecast today, the equity market kept making new highs until the summer of 1969, right before the economic cycle finally drew to a close in early1970 with a recession.

Conclusion

We continue to have a relatively positive outlook in the intermediate term because we continue to believe the US economy has further room to run. However, we believe conditions are ripe for the long-awaited bond market correction in 2018. And because all asset classes trade on a relative valuation basis, we worry that this will likely cause a stock market correction. In other words, the reason U.S. stocks are currently expensive is because bond yields are so low. And we worry that if bond yields rise, equity markets will likely reprice lower as valuations contract. Putting it in the context of our title, we believe that today is more akin to 1966 not 1969 and we would encourage investors to look through any potential market correction.

However, we reiterate our call that portfolios should be broadly diversified as we move nearer to the end of this economic and market cycle. And we believe that this mix should include commodities as an (increasing) part of that mix. Why? Because they historically have a high correlation with inflation and may serve as an important asset class to help ballast any potential stock and bond market decline.

Happy New Year

© Northwestern Mutual Wealth Management Company

© Northwestern Mutual Wealth Management

Read more commentaries by Northwestern Mutual Wealth Management