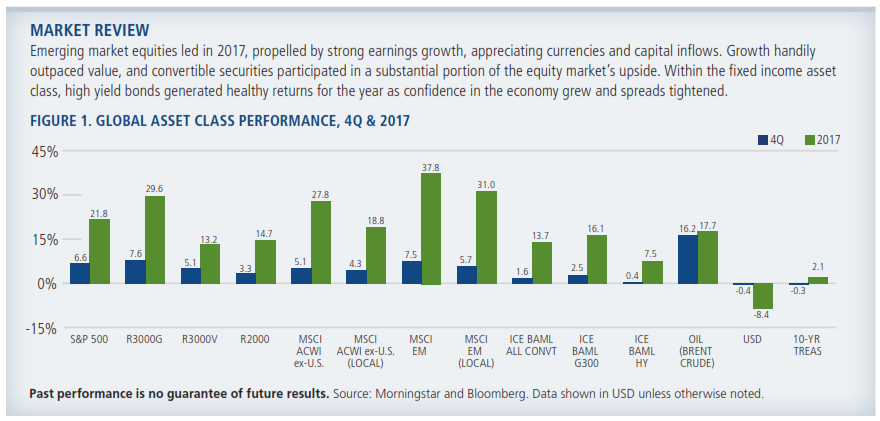

Global economic growth and benign inflation provided an extremely supportive environment for risk assets in 2017. As the year progressed, deregulation and anticipation of tax reform in the U.S. brightened investor sentiment even more. Although the Federal Reserve continued to raise short-term interest rates, its gradual course and the accommodative policies of other global central banks helped keep long-term rates in check, resulting in a flattening of the yield curve.

Our current positioning reflects the following beliefs:

- Many of 2017’s positive economic tailwinds should continue in 2018, setting the stage for additional upside in stocks and other equity-sensitive assets, including convertible securities and high yield bonds.

- Global economic expansion is on track, and the risk of recession in the U.S. and other major economies is low.

- Volatility will begin a slow return to its longer-term trend, but this is likely to be gradual so long as central bank accommodation remains intact. We may also see significant shifts in leadership in this maturing bull market.

- In a rotational and more volatile environment, the benefits of active, risk-aware management will be pronounced.

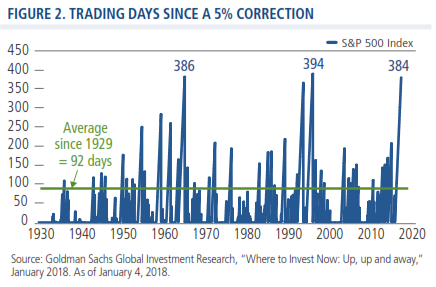

- Investors should not be surprised if the stock market experiences a modest downturn in 2018 before resuming its advance. In fact, the absence of recent corrections has been remarkable (Figure 2).

- As 2018 progresses, there may be a slight pick-up in inflation, but the expansion narrative should remain intact. Central banks are likely to become less accommodative as the year progresses, but we expect monetary policy to evolve in a gradual and deliberate manner.

- The most significant potential risks in the current environment include an unexpectedly rapid rise in inflation, significant shifts in central bank policies, and a boiling over of geopolitical conflicts (e.g., North Korea). U.S. mid-term elections may also stoke volatility, as could elections in Italy, Mexico and Brazil.

United States

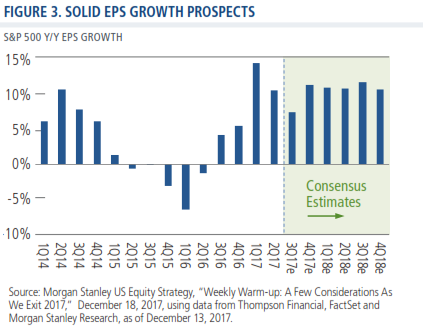

Lower corporate taxes, reduced regulations, job growth and consumer activity are among the factors that can sustain a “long-cycle” U.S. expansion in the coming year. Tighter labor markets and tax incentives should catalyze capex spending. With more cash to spend thanks to tax law changes, corporations may ramp up merger-and-acquisition activity. Small business optimism has surged and consumer confidence has also risen. Household balance sheets are sound, and lower-end consumers—absent for the first years of the recovery—are breathing new life into the expansion. In this late-cycle phase, solid corporate earnings growth can continue through 2018 (Figure 3), with synchronized global GDP growth and tax reform underpinning U.S. sales and profit growth.

Within the U.S. equity market, our teams continue to invest in cyclical areas (including financials, industrials and consumer discretionary names) as well as growth areas (such as technology). We remain underweight to more defensive “stable growth” areas. Given our expectation for rotational markets and potential drawdowns, we are vigilant to valuations across sectors.

Global and International

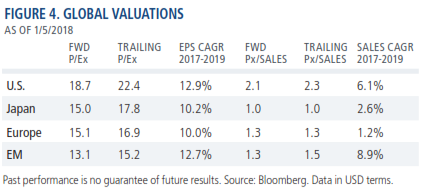

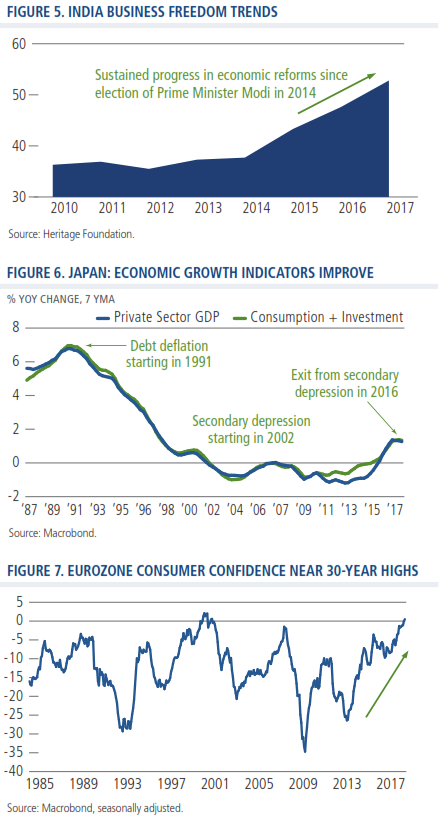

We expect broad improvements in economic fundamentals, accommodative monetary policy (especially the European Central Bank and the Bank of Japan), and a well-behaved U.S. dollar to drive additional upside in the global equity markets in 2018. Valuations and growth characteristics in emerging markets are especially attractive on a relative basis (Figure 4). Our positioning in emerging markets currently favors emerging Asia, and particularly China and India. In China, economic data indicates healthy domestic demand, increased exports and positive trends in industrials. We have invested in technology and consumer companies, balancing our secular growth positions with meaningful exposure to financials and industrials. In India, significant progress in economic reforms (Figure 5) provides a powerful secular tailwind for growth and has also led to a credit-rating upgrade. While valuations reflect some of this optimism, there remains significant upside, in our view.

In the developed markets, we have become increasingly constructive on Japan, where improving macro fundamentals (Figure 6), corporate efficiency and operating leverage are among the factors driving significant improvement in profits. Equities have rallied since the summer without a commensurate weakening of the yen, breaking the pattern of the past several years. Although valuations of some growth-oriented names have become stretched, the Japanese equity market remains attractively valued on the whole. We have also invested in a variety of European companies, where there is significant headroom for margins and profits to improve against the backdrop of an earlier- stage recovery supported by global growth, muted inflation, and high confidence levels for both consumers (Figure 7) and businesses.

Fixed Income

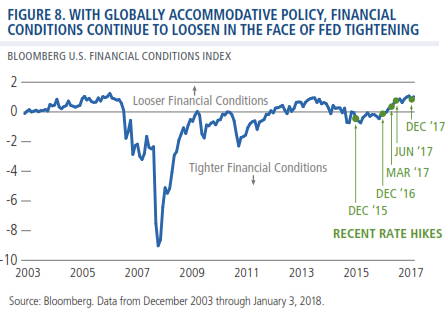

There are number of factors that can support positive fixed income returns in 2018, with active managers best positioned to exploit the opportunities. Inflation remains contained and below the Fed’s target and financial conditions have loosened rather than tightened with recent increases to short-term rates (Figure 8). Provided that global central banks move gradually (our base case), U.S. long-term rates should continue to be well behaved. Additionally, tax reform provides a broad-based, long-term tailwind to corporate issuers. Although interest rate deductibility caps eventually may pressure highly levered companies, provisions for deductibility and capital expenditures support corporate deleveraging over time.

We believe incoming Chair Jerome Powell will maintain the gradual and well-communicated course of recent years. As the U.S. economy expands, we expect the Fed will raise short-term interest rates three times this year, with a “Chairman’s choice” for a fourth hike in December. However, long-term rates will likely rise gently, resulting in a continued flattening of the yield curve. As we have noted in the past, parallel shifts in long-term and short-term rates have historically been the exception, not the rule.

Within the fixed income asset class, our outlook on high yield is constructive. We expect defaults to trend along the current benign path. However, given the narrowness of spreads, this is an environment where fundamental research and a bond-by-bond approach will shine. We have found idiosyncratic opportunities in a range of sectors, including out-of-favor areas of the market, including retail, pharmaceuticals, and telecommunications.

Convertible Securities

Global convertible issuance for 2017 totaled $74.5 billion, slightly lower than 2016 levels but still healthy. We anticipate attractive issuance trends in 2018, as appetite for risk assets remains high and companies seek new capital growth in an expanding economy. In the U.S., supply is likely to get a further boost as interest deductibility caps encourage companies to issue convertibles rather than non-convertible structures. Convertible securities combine attributes of equities and fixed income securities, and these hybrid characteristics will be advantageous given our belief that stock market has more upside but volatility is likely to pick up with the potential for short-term corrections. Issues in the U.S. may also benefit if tax reform spurs M&A activity.

We continue to emphasize convertible securities with well-balanced attributes, consistent with our aim of providing both upside participation and downside protection. We have invested in companies that can benefit from long-term themes, which we believe provide resilience during choppier markets. From a sector standpoint, information technology companies are well represented, as are businesses tied to the consumer. We remain underweight to defensive sectors of the market, such as staples and utilities. Additionally, we have identified companies across the capitalization spectrum that we believe are best positioned to benefit from lower corporate tax rates and a healthy U.S. economy. In our global portfolios, we currently favor Europe, where positive top-down economic trends frame many bottom-up opportunities.

Conclusion

There are many reasons to be optimistic about investing in 2018, with compelling prospects across asset classes. The U.S. economy is in a late-cycle but not end-of-cycle phase, Europe and Japan are in earlier stage recoveries, and economic data is trending favorable in a number of emerging economies. While we see the bull market continuing, a correction would not come as a surprise. We encourage readers to remember that brief corrections are typical and even healthy for the markets, and can provide buying opportunities for those who have maintained appropriate levels of liquidity and diversification. We believe this market environment sets up well for active, experienced managers with tested risk-management disciplines.

Indexes are unmanaged, not available for direct investment and do not include fees and expenses. The U.S. Dollar Index measures the value of the U.S. dollar relative to a basket of foreign currencies, including Euro Area, Canada, Japan, United Kingdom, Switzerland, Australia, and Sweden. The Russell 3000 Growth Index and Russell 3000 Value Index measure U.S. growth and value equities, respectively. The Russell 2000 Index measures U.S. small cap stock performance. The S&P 500 Index is considered generally representative of the U.S. equity market. The MSCI All Country ex U.S. Index represents the performance of global equities, excluding the U.S. The MSCI Emerging Markets Index is a measure of the performance of emerging market equities. The ICE BofAML U.S. High Yield Index is an unmanaged index of U.S. high yield debt securities. The ICE BofAML All U.S. Convertible Index (VXA0) is a measure of the U.S. convertible market. The ICE BofAML G300 Index measures the performance of 300 global convertibles. Oil is represented by current pipeline export quality Brent blend. ICE Data: Source ICE Data Indices, LLC, used with permission. ICE permits use of the ICE BofAML indices and related data on an `as is’ basis, makes no warranties regarding same, does not guarantee the suitability, quality, accuracy, timeliness, and/or completeness of the ICE BofAML Indices or data included in, related to, or derived therefrom, assumes no liability in connection with the use of the foregoing and does not sponsor, endorse or recommend Calamos Advisors LLC or any of its products or services. Earnings per share (EPS) is a company’s profit divided by its number of outstanding shares. Price-to-earnings ratio (P/E) is a valuation ratio of a company’s current share price compared to its per-share earnings; forward P/Es are based on forecasted earnings. CAGR, or compounded annual growth rate measures year-over-year growth. Price-to-sales ratio measures a company’s stock price versus its revenues. Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be suitable for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

Calamos Investments LLC

2020 Calamos Court | Naperville, IL 60563-2787

800.582.6959 | www.calamos.com | [email protected]

Calamos Investments LLP

62 Threadneedle Street | London EC2R 8HP

Tel: +44 (0)20 3744 7010 | www.calamos.com/global

©2018 Calamos Investments LLC. All Rights Reserved.

Calamos® and Calamos Investments are registered trademarks of Calamos Investments LLC.

OUTLKCOM 18619 0118O C

This material is distributed for informational purposes only. The information contained herein is based on internal research derived from various sources and does not purport to be statements of all material facts relating to the information mentioned and, while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

© Calamos Investments

Read more commentaries by Calamos Investments