Executive Summary

■ Beware of “derivatives of derivatives.” When evaluating whether a given volatility strategy is appropriate for their portfolio, investors should seek to understand the primary drivers of returns.

■ Put writing strategies can deliver equity-like returns over the long term with less sensitivity to market valuations and smaller drawdowns compared to the equity market.

■ Only twice have equity valuations been higher than they are today—in 1929 and in 1999—but volatility is no longer cheap. We think this should prompt investors to look at index put writing as a substitute for equities.

Introduction

With the sharp rise in both realized volatility and the VIX index of implied volatility at the beginning of February, the topic of volatility trading has taken center stage. Investors have been duly inundated with commentary on volatility and volatility related products. However, among the deluge of market chatter, and plenty of confusion, we think it is worth taking a step back to consider three broader questions that pertain to the role that equity volatility can play in institutional portfolios.1 First, how should investors think about the plethora of volatility linked products currently offered? Second, how can investors incorporate volatility based strategies into their portfolios without taking undue risks? And third, are these strategies attractive given where we are in the market cycle? We tackle each question in turn.

Not all volatility products are created equal

There are, broadly speaking, two categories of short volatility strategies that are accessible to institutional investors. The first category consists of plain vanilla strategies in which the underlying asset is a standard asset, such as a broad equity index. Common strategies in this category include selling index put options, writing covered call options and selling both puts and calls (e.g., straddles). Expected levels of future volatility determine the price of the put and call options when they are sold, but the outcome of these strategies is determined by the value of the underlying equity index when the options expire.

When the driver of returns is the performance of an equity index over the life of the options, then this primary risk could be hedged with old fashioned equities. Such a strategy is only indirectly exposed to the level of stock market volatility as a secondary risk.2 As we will discuss below, index put writing and similar strategies are most appropriately viewed as equity replacements given their meaningful exposure to broad equity indices.

The second class of short volatility strategies includes those in which the underlying “asset” is volatility itself. Common strategies in this category include selling variance swaps and shorting VIX futures. The returns to these strategies are determined by the difference between the level of volatility when the trade is made and the level of volatility when the derivatives expire. As the profit or loss for these strategies depends on a future level of volatility3 of an equity index and not the value of the equity index itself, these can be viewed as derivatives of derivatives or “derivatives squared.” The now infamous exchange-traded note (ETN), which traded under the ticker XIV, was based on a strategy that combined shorting VIX futures with a very specific daily rebalancing rule.4

Generally speaking, if the strategy is primarily a bet on future realized or future implied volatility, then the underlying asset is itself, in essence, a derivative. The primary risk for these strategies is changes in levels of volatility. Hedging this risk would require trading volatility directly and so the strategy is exposed to the volatility of volatility as a secondary risk. As recent events have clearly demonstrated, volatility can easily double or even triple in a single day’s trading session, exposing such products to explosive risks. It is no coincidence then that the recent rapid rise in the VIX was catastrophic for several of these complex products.

Plain vanilla volatility in an equity portfolio

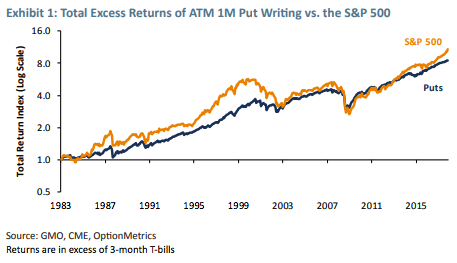

At GMO, we are strong believers that properly structured and risk managed options selling strategies have a role to play in institutional portfolios. In particular we think that products such as GMO’s Risk Premium Strategy, which sells fully collateralized put options on an array of global equity indices, belong in most investors’ equity portfolios as a complement to direct exposure to global equities for three reasons. First, for the entire history of the listed options market in the US, put writing has consistently delivered equity-like returns over multiple market cycles (see Exhibit 1). Index put sellers, like owners of equities, are fully exposed to correlated drawdowns in the equity market. It should therefore come as no surprise that put sellers have demanded (and received) a similar level of excess returns over full market cycles.

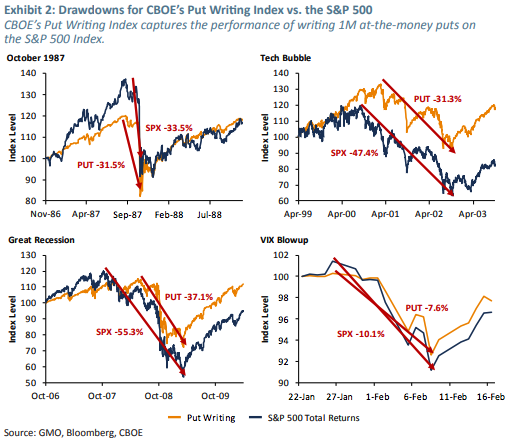

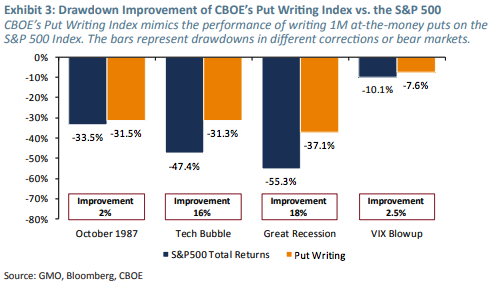

Second, as can be inferred from Exhibit 1, put writing strategies have a low beta to the equity market5 and they are able to collect elevated premiums during market sell offs due to enhanced demand for insurance in these periods. Put writing strategies should therefore be expected to have shallower drawdowns compared to the underlying equity index, seen in Exhibits 2 and 3, and this has been generally true. During the Black Monday event in 1987, the collapse of the TMT bubble, the Great Recession of 2008/2009 and the recent (but far less dramatic) VIX blowup, fully collateralized put writing has outperformed the broad market.

Finally, since put writing generates returns via the collection of option premiums rather than participation in upside earnings growth, the return profile is not especially correlated with equity market valuations. This is an attractive feature in fully priced markets,6 a point which is particularly appealing given the current overvalued nature of the US equity market.

Why does put selling make sense now?

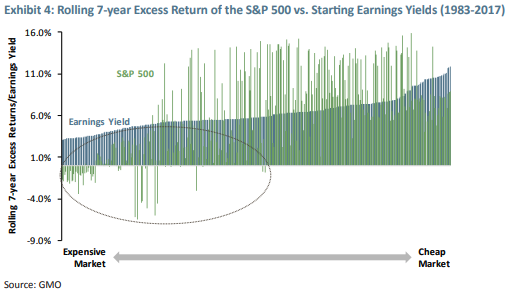

The long-term total returns of the equity market result from cumulative earnings growth combined with the compounding effect provided by re-invested dividends. Over any finite time horizon, the realized returns for any given investor are strongly determined by the multiples at which the equities were purchased. As shown in Exhibit 4, the returns to owning the S&P 500 over a 7-year horizon are strongly correlated with the starting earnings yield of the market. When earnings yields are low (and growth expectations are high) subsequent returns have been quite poor. In contrast, when earnings yields are modest to high (and growth expectations are subdued), the subsequent returns have ranged from good to very good.

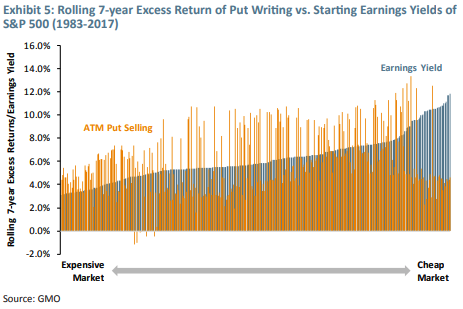

As noted above, put sellers have attained the same level of returns as long-only equity holders but with a very different return profile. The difference in return profile can be attributed to the source of the returns. In the case of long-only equities, the long-term returns are the result of price appreciation due to earnings growth and the initial price paid for that earnings growth. Put sellers have, by definition, no exposure to the upside of the equity market: they get their long-term return via the so-called implied-to-realized gap, which is a measure of the difference between the price at which an option is sold and an ex-post reckoning of what the fair price should have been.7 While the implied-to-realized gap has generally been positive for equity indices, it does vary over time. Importantly, its variation has not been especially correlated with equity market valuations. In other words, put selling strategies have historically delivered their returns in a manner which is remarkably insensitive to starting valuations of the equity market (see Exhibit 5). As such, this makes a global put selling strategy an especially attractive component of an equity portfolio today as equity markets, especially in the US, are trading at historically high valuations.8

Conclusion Given the current heightened valuations across global equity markets, now is a fitting time to take a careful look at put writing strategies as an equity replacement, especially after the VIX blowup. Following the recent spike in volatility, equities remain rich while volatility is no longer cheap. With the VIX now trading near its long-term historical average, the prospective returns to put writing can be expected to be in line with long-term averages. Given US equity market valuations have only twice been more extreme than they are today, the same cannot be said for traditional equities. We believe it is therefore a critical time for investors to consider swapping a portion of their traditional equity exposure for index put writing.

Special Topic: VIX Blowup Post Mortem

What happened?

While there are many press reports available which correctly focused on the role of inverse VIX Exchanged Traded Products (ETPs) in great detail,9 it suffices to say that due to the design of these products (which importantly guarantee holders daily as opposed to some other time horizon’s inverse exposure to the VIX index), inverse VIX issuers were forced to cover their risks on a matched daily basis by buying VIX futures in a self-fulfilling loop. More explicitly, the buying of VIX futures led to a higher VIX futures price, which led to lower NAVs for inverse VIX products, which led to more risks that needed to be covered, which ultimately led to buying more VIX futures, and so on. The cycle terminates at the decimation of the NAV. While this is the ostensible catalyst for movements in the VIX and S&P 500, it is important to recognize that it is nearly impossible to disentangle this from broader and contemporaneous market concerns, such as higher real and nominal rates, firming inflation and wages, quantitative tightening, shifting stock-bond correlations and fully priced markets.

Looking forward

Is the event behind us? While the inverse VIX ETPs have covered 95% of their shorts, we disagree with the market consensus that the VIX risk is now completely out of the system. For example, XIV had, and to a lesser extent, still has, significant exposure to the March expiry VIX futures, which they attempted to cover on Monday, February 5. This means that offsetting dealers now have this risk on their balance sheets, and we are doubtful that they managed to hedge all of it out during extremely dislocated markets, considering the size of the risk transfer. Hence the risk won’t completely evaporate until the March futures expiration. It is reasonable to expect periodic opportunistic volatility hedging from these dealers until then. This recent fading of the volatility spike seems an opportune time to unload market risks, for example.

1 For those who are interested in the February 5th VIX blowup post mortem, see the special topic box on page 6.

2 In options parlance, delta is a larger driver of returns than vega for this type of strategy.

3 In the case of variance swaps the underlying asset is the future realized volatility squared. In the case of VIX futures, the underlying asset is the future implied volatility. The returns to selling VIX futures also depend on the slope of the futures curve.

4 For derivatives experts: the daily rebalancing rule amounted to these ETNs having their own gamma. XIV was therefore really a third order derivative or a “derivative cubed.”

5 This is mechanical: At-the-money put writing strategies have a delta of approximately 0.5, so a low beta to the market is guaranteed.

6 For a detailed discussion please see the GMO white paper entitled “New Options for Equity Investors” by Neil Constable.

7 Technically, it is the difference between implied volatility at the time an option is sold and the subsequent realized volatility of the underlying asset.

8 As of January 31st,, GMO’s Asset Allocation team’s 7-year forecast for the US market is a rather dismal -5.6% and for the rest of the developed markets they are expecting an uninspiring -1.0%.

9 For examples, see here: https://www.bloomberg.com/view/articles/2018-02-09/inverse-volatility-products-almost-worked or here: https://www.reuters.com/article/us-usa-stocks-volatility/black-monday-for-vix-etps-leaves-retail-players-smarting-idUSKBN1FQ261

Van Trieu Le. Mr. Le is a research analyst for GMO’s Global Equity team. Previously at GMO, he was a member of GMO’s Asset Allocation team. Prior to joining GMO in 2015, he worked at JP Morgan most recently as a Sales and Trading Associate for Global Asset Allocation Investments and prior to that as a Fixed Income Sales and Trading Associate. Mr. Le earned his MS and undergraduate degree in Econometrics and Mathematical Economics from the London School of Economics and Political Science, his Master of Advanced Study in Mathematics from the University of Cambridge, and his Master of Finance from Princeton University.

Neil Constable. Dr. Constable is the head of GMO’s Global Equity team. Previously at GMO, he was the head of quantitative research and engaged in portfolio management for the Global Equity team’s quantitative products. Prior to joining GMO in 2006, he was a quantitative researcher for State Street Global Markets and a post-doctoral fellow at MIT. Dr. Constable earned his B.S. in Physics from the University of Calgary, his Master’s in Mathematics from Cambridge University, and his Ph.D. in Physics from McGill University.

Disclaimer: The views expressed are the views of Van Trieu Le and Neil Constable through the period ending February 2018, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2018 by GMO LLC. All rights reserved

© GMO

Read more commentaries by GMO