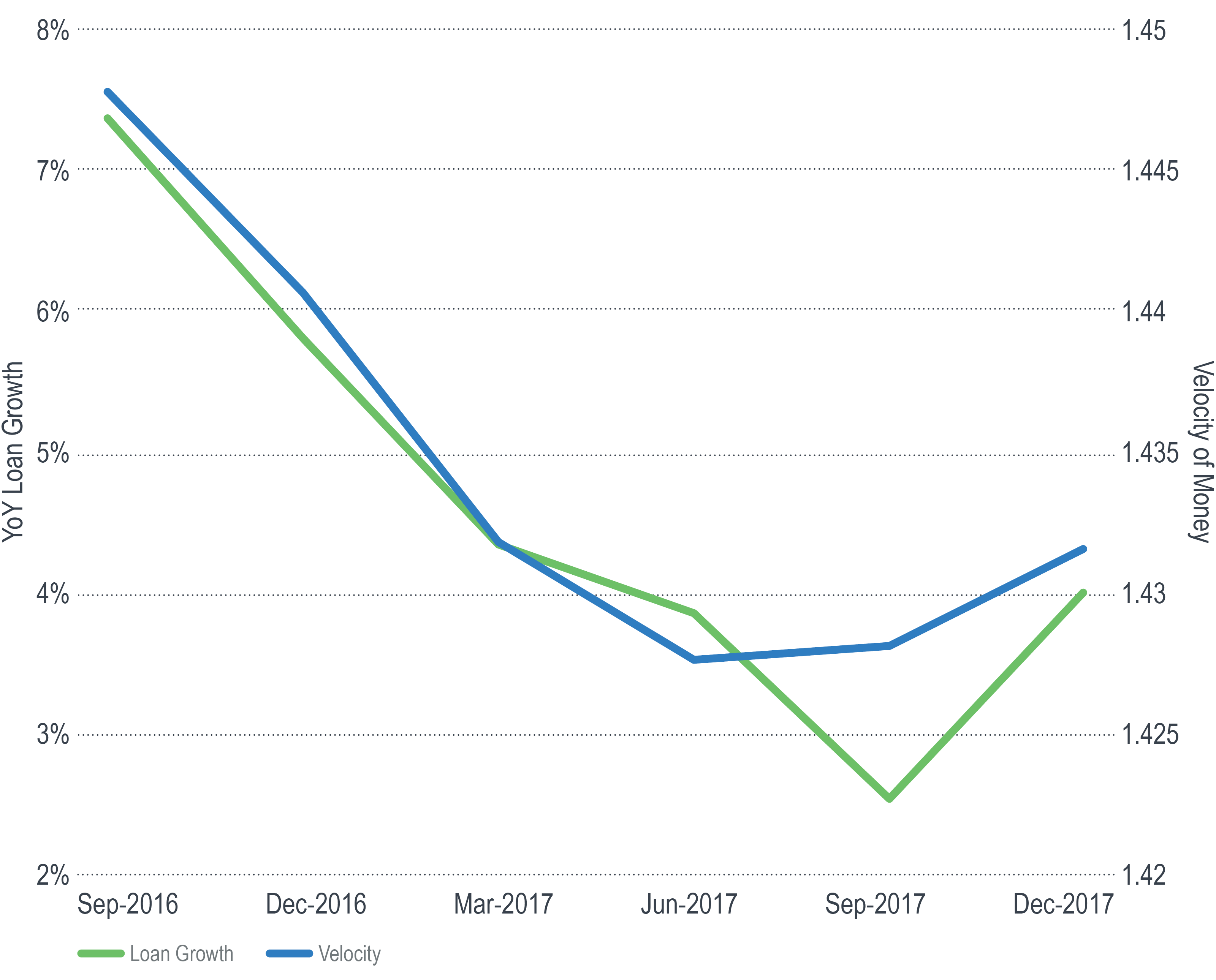

Chart of the week

Loan Growth & Velocity of Money

After declining for 11 consecutive quarters and for 26 out of the last 27, the velocity of money increased in both Q3 and Q4 2017.

As indicated in this simple formula, the velocity of money is a function of both money and prices:

V = PQ / M, where:

V = velocity

P = general price level

Q = quantity of goods and services

M = money supply

Velocity of money is the number of times one unit of money is spent to buy goods and services in a given unit of time. It is an indication of a willingness to spend money; that willingness can be affected by the quantity of credit formation. It is perhaps no fluke that the two consecutive increases in velocity coincided with the first increase in loan growth1 in more than a year.

Loan growth not only increases money supply (M), but also has a positive correlation with velocity of money (V). If Q and M rise at the same rate, a higher velocity (V) means a higher price (P).

In addition to both the price of gold and breakeven inflation rates pushing higher in recent months, this potential inflection of money velocity may be another sign that higher inflation is not far off.

1As measured by the growth in notional loan amounts held by the US banks listed in the S&P Banks Select Industry Index.

Unless otherwise noted, data is sourced from Bloomberg.

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

The results shown are historical, for informational purposes only, and do not guarantee future results.

Any discussion of risks contained herein with respect to any product or service should not be considered a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

Data included in this document has been sourced from providers that Milliman FRM believes to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by Milliman FRM as to the accuracy or completeness of the source data or any other information in this document.

For financial professional use only.