Executive Summary

In this paper, we revisit Ben Graham’s principles of value investing and extrapolate them further to the implications of investing in emerging markets. Graham reminds us that a disciplined approach to good investing requires us to be cognizant of changes in intrinsic value and be open to re-examining previously established conclusions. This holds true particularly in emerging markets where multiple risks abound and an economically diversified portfolio is critical to tackle uncertain outcomes.

Introduction

It was a typical Wednesday afternoon meeting with a client. As we reviewed the portfolio characteristics and valuation metrics of our Emerging Domestic Opportunities portfolio, the client, somewhat surprised, asked why the portfolio did not have stronger “value” characteristics. This was neither the first time we had been asked this question, nor was it the first time we had contemplated the notion of value.

Undoubtedly, the client was in the textbook, or conventional, sense correct. Yet, for us, the dichotomy was evident: We consider our emerging markets fundamental equity portfolio to be representative of value. In fact, much of our understanding of value is influenced by the work of Ben Graham. That said, our client’s question as to what constitutes “value” is important in and of itself, but is especially so in the context of emerging market equities.

We use a variety of approaches to assess value, ranging from data-driven macroeconomic countrylevel drivers to behavioral indicators at the country, sector, and security level. Contrary to popular belief, using a variety of approaches does not mean we are deflecting or diluting the essence of value. We would argue, in fact, that our approach increases the odds of putting together a true value portfolio.

Back to Basics: Revisiting Graham’s The Intelligent Investor2

In the introduction to Graham’s classic book on value investing, he spells out that his primary objective in writing the book was to help the lay investor develop and execute sound investment policy. In doing so, Graham introduced something rare in the realm of investing and economics: first principles.

Below are the bedrock principles that Graham believed should underpin any investment strategy.

■ An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return.

■ Our main objective will be to guide the reader against the areas of possible substantial error and to develop policies with which he/she will be comfortable.

As far as Graham was concerned, there are two primary ways investors violate these principles: They pay too high a price for a security relative to its intrinsic value, or they underestimate a potential decline in the intrinsic value of a security.

We believe value investing has come to be defined rigidly and narrowly as paying too high a price for an asset. The expensiveness or cheapness of a security is assessed using a handful of valuation-driven variables such as Price/Earnings, Price/Book, and dividend yield. However, the use of these tools alone ignores two critical points from Graham’s teachings:

1. It downplays the risk of a decline in intrinsic value. This error is made again and again despite Graham’s insistence of this variable’s importance.

2. While having an investment philosophy might sound simple, in practice implementing it is not. He emphasized repeatedly that an investor needs to be both pragmatic and flexible in order to guard against unknown risks.

By relying solely on headline valuation metrics, the value investing community commits what behavioral psychologists refer to as “attribute substitution.” They simply swap out the harder question – What are the intricacies of real-world investing? – for an easier one – Which straightforward valuation metrics can we use in order to avoid overpaying for an asset? Psychologists Kahneman and Tversky attribute many cognitive biases to this principle.3

We believe this error is particularly egregious and relevant to emerging markets because there is a larger complex of risks associated with these assets. That is to say, there are more ways to lose money and make substantial errors investing in emerging markets than there are in developed markets.

As value investors, we at GMO try to incorporate what we believe are the key principles that Graham espouses when it comes to meeting the objective of not losing money when investing. These principles are to:

■ Avoid buying overvalued assets;

■ Be cognizant of quality, i.e., the risk of a decline in intrinsic value; and

■ Build and maintain a pragmatic and flexible approach to thinking about the above issues.

The first is obviously important, however, because it has already been discussed ad nauseam, we will skip it here. Instead, we will focus on the last two points as they are equally (if not more) important in the context of investing in emerging markets.

The risk of a decline in intrinsic value

The value-investing crowd’s lack of appreciation for a decline in intrinsic value is surprising given how much Graham focused on this risk. From “Margin of Safety,” the last chapter of the book:

However, the risk of paying too high of a price for good-quality stocks – while a real one – is not the chief hazard confronting the average buyer of securities. Observation over many years has taught us that the chief losses to investors come from the purchase of low-quality securities at times of favorable business conditions.

This risk is significantly more prevalent in emerging markets. As fundamental equity investors in these markets, we have experienced firsthand a number of drawdowns, including the Asian financial crisis of 1997.

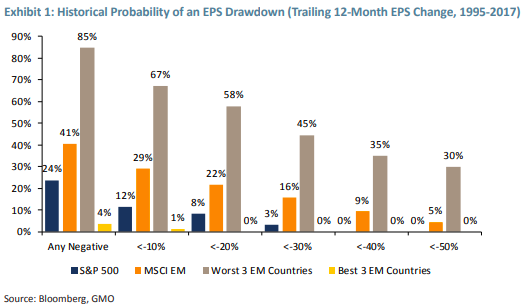

To further illustrate this point, the likelihood of a 20% or greater decline in EPS over any 12-month period for the S&P 500 is 8% (see Exhibit 1). Conversely, the probability of a similar decline for MSCI Emerging EPS is more than twice that at 22%. In addition, the likelihood of the three worst emerging market countries experiencing a drawdown of 20% or greater is staggeringly high at 58%.

These drawdowns happen with alarming regularity in emerging markets for a variety of reasons, including the lack of institutional frameworks, poor-quality management, and greater vulnerability to the credit cycle.

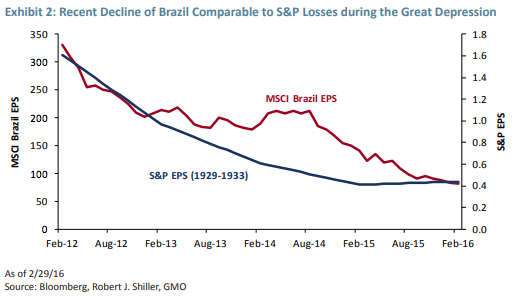

A recent example of such a drawdown occurred in Brazil. From 2011 to 2016, both the economy and the market experienced a significant decline in value (see Exhibit 2). Over this period, GDP per capita declined 30%, index earnings fell 68%, and the market fell 70% in US dollar terms. Comparing this to the fall of the S&P from 1929 to 1933 during the Great Depression, an event etched in our minds, GDP per capita fell 28% and the market fell 80%.

A pragmatic and flexible approach to investing

At the core of Graham’s approach was an acknowledgement that markets are not static and, in general, that we have a limited understanding of them. His pragmatic and flexible approach is neatly summed up in the book’s last chapter:

Thus, in sum, we say that to have a true investment there must be present a true margin of safety. And a true margin of safety is one that can be demonstrated by figures, by persuasive reasoning, and by reference to a body of actual experience.

The above is perhaps the central point of The Intelligent Investor. It is noteworthy that Graham does not espouse specific ratios or investment principles as the ultimate arbiter of value.

In addition, throughout his writings, Graham continually stresses the importance of data, reasoning, and experience. This approach is converse to popular belief and modern value investing literature. Ultimately, this is a nod to our general lack of understanding of markets.

Theory can only take us so far. When data contradicts theory, trust the data.

This view is best demonstrated in the first three chapters of the book, where Graham examined the impact of inflation on equity returns, pondering the attractiveness of equities versus bonds. He calculated that equities would likely yield ~8% (3.5% from dividend yield and roughly 5% from nominal earnings growth). The earnings growth figure he used was simply the historic average. This 8% figure was in line with nominal bond yields. Graham then questioned whether we should expect higher earnings growth given higher inflation.

Graham admits that in theory (and as he had stated in previous editions of the book), corporate earnings should be positively correlated to higher inflation. Consequently, equities should outperform bonds during these periods of high inflation.

Intellectual honesty: it’s okay to stand corrected

As opposed to relying on theory (or on what was said in prior editions), Graham then re-examined the data from 1915-1970 (1970 being the most recent year available to him). Following the exercise, Graham concluded, “Our figures indicate that so far from inflation having benefited our corporations and their shareholders, its effect has been quite the opposite.” He attributed this to the rise of corporate debt between 1950 and 1969; corporate debt rose fivefold while profit before taxes a little more than doubled.

Based on the data, he viewed the case for higher earnings growth given higher inflation as inconclusive. Consequently, he did not view equities as attractive when compared to bonds.

Utilizing data was simply not enough. Graham emphasized and demonstrated considerable flexibility and intellectual honesty. However, he also stressed the importance of having an adequate history of data:

But much of our space will be devoted to the historical patterns of financial markets, in some cases running back over many decades. To invest intelligently in securities one should be forearmed with an adequate knowledge of how the various types of bonds and stocks have actually behaved under varying conditions - some of which, at least, one is likely to meet again in one’s own experience. [Emphasis added.]

Lessons for the emerging market investor: triangulating value with limited data availability and the lack of historical precedents

When extrapolating Ben Graham’s experience in the context of emerging markets, it is imperative to acknowledge the limited availability of data and the general lack of knowledge in the absence of historical precedents.

For example, it is hard to fathom, but China, which accounts for 40% of the MSCI Emerging Markets Index, did not issue its first stock until 1984. In fact, the Shanghai Stock Exchange was non-existent until 1990. The Chinese equity market is still in its infancy. At best, we have just 27 years of historical data. (Compare this with the above example from the book, where Graham makes one conclusion after 80 years of data and then reassesses the initial conclusion after obtaining an additional 20 years of data.) Another example is the recent demonetization in India, which was effectively one of the biggest monetary experiments in emerging markets. Eight-five percent of the currency in circulation was taken out overnight without any prior notice!

Conclusion

Graham reminds us that as investors we have two primary objectives:

■ Protect principal while providing an adequate return; and

■ Avoid substantial errors.

In emerging market equity investing, the ways in which we might incur losses to principal are numerous and we must accept the realities of significant forecasting risks. Given this, investors should go well beyond seeking securities that are “cheap” purely in terms of traditional valuation metrics. The very nature of emerging markets should prompt us to regularly assess the macro-economic health of each country as well as the most likely government policies ahead and their potential impact on intrinsic value. These second-order effects of value, which are particularly pronounced in emerging markets, are not always captured in analysts’ valuation metrics. Emerging market investors would do well to focus on building economically diversified portfolios with a number of uncorrelated positions that can withstand short-term performance shocks. For if there is one thing we have learned in our years of dedicated experience in investing in emerging markets, it is that we can be caught off guard. We believe that our approach of triangulating value through myriad lenses, constantly revisiting the data, and dynamically allocating between country/sector and security combinations gives us the best probability of success.

Amit Bhartia. Mr. Bhartia is a portfolio manager for GMO’s Emerging Markets Equity team and oversees fundamental research. Prior to joining GMO in 1995, he worked as an investment advisor in India. Mr. Bhartia earned a Bachelor of Engineering at the University of Bombay and an MBA at the Institute for Technology and Management in Bombay. He is a CFA charterholder.

Matt Seto. Mr. Seto is engaged in fundamental research for GMO’s Emerging Markets Equity team. Prior to joining GMO in 2008, he was a vice-president in the global markets group at HSBC. Mr. Seto earned his BA in economics from the University of Michigan and his MBA from Columbia University.

Disclaimer: The views expressed are the views of Amit Bhartia and Matt Seto through the period ending February 2018, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2018 by GMO LLC. All rights reserved.

1 We would like to thank our colleague, Mehak Dua, for her many contributions to this paper.

2 The Intelligent Investor was first published in 1949 and was last revised in 1986. This paper uses material from the most recent edition.

3 See, for example, Amos Tversky and Daniel Kahneman, “Judgment Under Uncertainty: Heuristics and Biases,” Science, 185, 1124-1131, 1974.

© GMO

Read more commentaries by GMO