ESG: Improving Your Risk-Adjusted Returns in Emerging Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Introduction

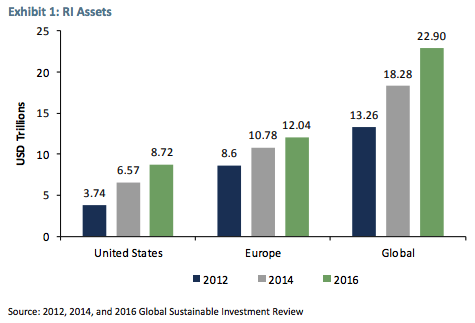

The demand for environmental, social, and governance (ESG) or responsible investing (RI) is growing at a rapid pace with nearly USD 23 trillion of assets being professionally managed under RI as of 2016, an increase of 72% since 2012.1 Despite increased investor interest and relatively higher risk exposure to ESG issues, the lack of breadth and depth in corporate sustainability disclosures has led to exaggeratedly low ESG scores and hitherto restricted rigorous application of ESG integration strategies to emerging market (EM) portfolios. With regulatory momentum moving toward more transparent, relevant, and accurate corporate disclosures, and the increased use of technology to capture and analyze data, this sustainability information gap is quickly reducing in many EM countries.

In Part 1 of this paper, we make the case that this cannot come too soon for EM investing as these countries are generally both more vulnerable to ESG issues and less prepared to deal with them. From an active manager’s perspective, the ESG scores in emerging markets encompass a wide spectrum, thereby offering another avenue to add value. In Part 2 we establish that both macro and micro ESG issues can substantially impact the earnings potential of corporations. We also highlight the benefits of developing a proprietary ESG assessment framework over a reliance on off-the-shelf ESG scores from vendors. We also demonstrate, using a case study, how one can integrate ESG risks and opportunities with traditional financial analysis to enhance the overall investment process. We conclude by underlining our conviction that although ESG signals are worth integrating in all strategies, there are some strategies in which these signals have a greater impact.

Part 1: Why ESG?

Environmental, social, and governance or responsible investing discussions are often accompanied by a degree of confusion because participants cannot agree on what it involves: whether it improves returns, lowers the risk profile, or is just aimed at having a positive impact on all stakeholders. In its early days, RI started off as socially responsible investing (SRI) and had a primary focus of screening out companies or, in some cases, entire industries (e.g., tobacco) based on ethical or religious beliefs. It has now evolved into a practice of integrating material ESG data with traditional financial analysis to better manage risk and strengthen the investment decision-making process. Globally, seven ESG strategies, as defined by the Global Sustainable Investment Alliance (GSIA), are typically applied. These include screening based on negative, norms-based, or positive criteria; thematic and impact investing; active ownership; and ESG integration. Depending on the asset owner’s motivation, ESG investing could mean investing in businesses that generate positive social or environmental impacts (impact investing); screening out controversial businesses such as tobacco, weapons, alcohol, etc., from the investment universe (values-based investing); or employing ESG signals at the security and portfolio level with a goal of improving risk-adjusted returns (ESG integration).

As shown in Exhibit 1, RI is growing at a rapid pace, with nearly USD 23 trillion of assets being professionally managed as of 2016, an increase of 72% since 2012. This growth has been driven largely by institutional investors, as evidenced by more than 1,900 signatories to the United Nations supported Principles for Responsible Investing (PRI).2 These investors have committed to incorporating ESG issues into investment analysis and the decision-making process. Investor interest in ESG is driven by two key global trends. First, mismanagement of sustainability issues such as climate change, product safety, data security, and resource scarcity are having increasingly substantial financial impacts on a company’s fair value, thereby making assessment of ESG risks and opportunities a relevant enhancement to traditional financial analysis. Second, millennials, the generation born in the 1980s and 1990s, are strong believers in investing sustainably and are demanding that investment managers systematically evaluate ESG risks as well as negative environmental and societal impacts of their portfolio investments, be it for their inherited wealth or pension contributions.

EM countries are usually characterized by rapid population growth and urbanization, income inequality, and a lower quality of governance and regulatory enforcement. These characteristics make their economies more vulnerable to the ill effects of ESG issues such as extreme weather events (e.g., floods, droughts, cyclones), resource scarcity (e.g., water, food), social unrest, and corruption. Despite increased investor interest and a relatively higher investment risk exposure to ESG issues, the lack of breadth and depth in corporate sustainability disclosures has led to exaggeratedly low ESG scores and consequently restricted the rigorous application of ESG integration strategies to EM portfolios.

With a regulatory-driven momentum toward more transparent, relevant, and accurate corporate disclosures, and the increased use of technology to capture and analyze data, this sustainability information gap is quickly reducing in many emerging markets. Historically, EM companies have lagged their developed market (DM) counterparts in integrating sustainability in their day-today operations and therefore have, on average, ranked poorly on ESG performance. However, the performance range is quite broad. At one end of the spectrum, there are companies in the EM universe that demonstrate strong awareness and management of their ESG risks and opportunities and thus rank at par or better than many of their DM counterparts. On the other hand, there are many laggards with high levels of unmanaged ESG risks and, therefore, may expose a portfolio to black swan type events. A similar scenario exists when one looks at country-level ESG risks. This wide range of ESG performance in the EM basket makes it essential to establish robust criteria for assessing performance and integration of ESG data in an investor’s EM country and stock selection processes.

How relevant is ESG in EM?

As we will establish by using a number of examples in this section, EM economies are generally both more exposed and less prepared to manage the impact of ESG risks than DM. Therefore, it is of utmost importance that investment analysts factor in both country-level as well as issuer-level ESG risks when making EM investment decisions.

Environmental risks

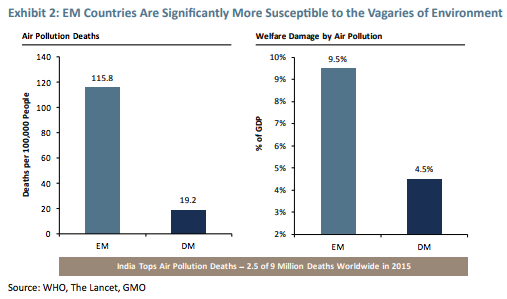

The greater vulnerability to environmental impacts follows from the fact that agriculture constitutes 8% of GDP in EM versus only 1% in DM. The physical impacts of climate change, such as changing weather patterns, will be felt in all aspects of life, but we know the effects are particularly severe within activities that are highly dependent on environmental stability, such as agriculture. Unlike most developed markets, emerging economies do not have the luxury of buffers such as mass irrigation and crop insurance, leaving them vulnerable to floods or droughts. Another key environmental issue is air pollution, which comes from both consumer and industrial sources. Consumer sources include untreated waste and use of kerosene rather than piped natural gas in residential areas; industrial effects arise from a deficiency of public transportation, weak enforcement of laws capping factory emissions, and a larger prevalence of industries (e.g., ship dismantling, leather tanning, textile dyeing) with harmful by-products. Exhibit 2 illustrates the greater impact of weak environmental standards on emerging markets whether it is measured from a human or economic perspective.

Social risks

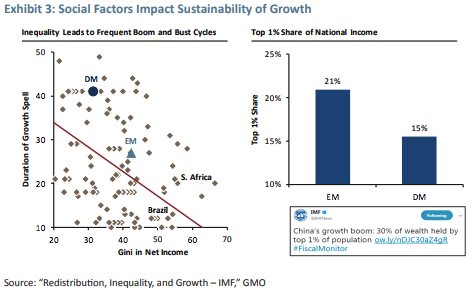

Social factors, sometimes dismissed as touchy-feely, can have real impacts on growth. Broadly speaking, a society that places less stress on social equity is also a society that is marked by big differences in human capital. Human capital is the best predictor of income. A socially unequal society is, not surprisingly, also a society that displays wide income inequality. Income inequality is inversely correlated to the longevity of growth cycles in an economy. A longer and more stable growth spell gives companies and individuals more confidence to plan and invest for the long term. This leads to a build-up of physical and human capital. Exhibit 3 shows that emerging countries are generally less equal as measured by the Gini coefficient (a higher Gini score reflects greater inequality in income), hence the duration of growth spells is shorter. In other words, EM economies are more prone to boom and bust cycles.

Governance risks

Closely related to social factors is governance. Compared to DM countries, politics in EM countries is more unpredictable as populations swing more easily from one particular ideology to another. A related aspect is that institutions are weak and unable to check the excesses of subpar leadership. These unfettered ideological swings are tied to a wide range of friendliness to capital and labor. This high level of uncertainty incentivizes domestic and foreign investors to make short-term bets rather than pledge capital for the long term. Inflows are therefore characterized more by portfolio flows (hot money) rather than direct investment (stable money).

The peril of ignoring ESG risks

The Arab Spring was arguably the first major ESG crisis of the 21st century. Populations in the Arab world were fed up with the corruption and nepotism of their authoritarian governments. This was compounded by the large proportion of young people who felt alienated from the system. The presence of social media helped these youth express and share their views without having to rely on the traditional (government controlled) media to be the intermediary. It is estimated that the number of Facebook users in the Arab world at this time surpassed 25 million. Finally, environmental effects such as droughts in Russia and Ukraine and torrential storms in Canada and Australia in previous years had driven up commodity prices. The self-immolation of a Tunisian roadside vendor was the spark that set off the Arab Spring, but it was continual poor performance on ESG factors that helped to build and fill the powder keg.

Part 2: Assessing and Integrating Country-Level ESG Risks for a Heterogeneous Asset Class

While we have used EM countries as a group to differentiate them from DM countries, there is a huge variation within emerging markets both with regards to each country’s current management of ESG risks, as well as their respective financial and economic strength to reduce each country’s vulnerability to ESG risks in the future. This variation lends itself naturally to a top-down ESG analysis of EM countries.

Assessing ESG risks

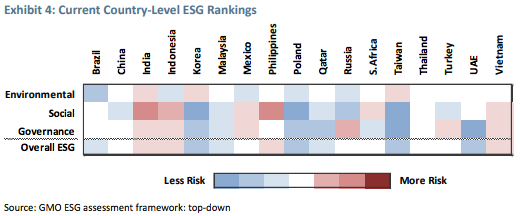

Sourcing a variety of ESG preparedness and performance signals across topics such as resource consumption, air quality, education, equality, political capacity, quality of institutions, and corruption, GMO has developed its own country ESG assessment framework. The heat map (Exhibit 4) demonstrates the relative ESG performance of major EM countries using our ESG assessment framework. Red signifies poor performance, and blue denotes strong management.

Importance of integrating country-level ESG risks into investment analysis

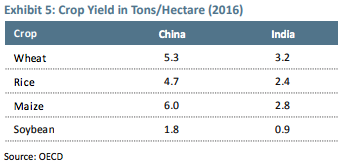

In order to better understand how the country-level ESG risks translate into negative impacts on a company’s fair value, let’s look at the varying level of preparedness of India and China to manage a country-level ESG risk – climate change. Indian farmers are highly dependent on monsoons and have low crop insurance coverage, which means subpar rains lead to massive rural distress. The government typically responds by waiving loans to small farmers (e.g., loans worth approximately USD 24 billion have been waived since 2014). This buys short-term popularity with the masses, but carries long-term negatives for the economy as the fiscal slippage leads to lower government spending on infrastructure development (say, for improved irrigation). This practice leaves India vulnerable to future impacts of climate change, and adds the further burden of weakened balance sheets in the banking system, which impacts growth. China, despite having just as large a population as India, has ensured that its economy is more resilient when facing risks related to climate change. It has channeled a lot of its debt toward infrastructure development. For example, China has irrigated the majority of its farming areas by diverting rivers and building canals. This has not only lowered the dependence on monsoon, but it has also led to increased productivity, with Chinese crop yields being approximately twice those of India (see Exhibit 5).

Social factors vary widely across EM. The Gini coefficient – a commonly used measure of inequality – is 34 for Taiwan and 48 for Mexico. And the difference in the impact on the stability of growth spells is just as striking. From 2000 to 2016, Mexico on average outgrew Taiwan 4.0% to 3.5%. But, the volatility of these growth rates tells a very different story. The volatility of GDP growth rates in Taiwan since 2000 has been 5.6% as opposed to 10.0% for Mexico. Needless to say, this higher uncertainty has had a deleterious effect on the average resident. The income of the average resident in Mexico grew at 2.1%/ yr. vs. 2.9%/yr. in Taiwan even though the overall country’s GDP growth rate was faster. Social failings thus translate into worse economic outcomes.

The case for sound governance is easy to make. The EM asset class has far too many examples where poor leadership at the country level led to a fall in economic activity and stock prices. A current example is South Africa. Corruption allegations against former President Zuma had led to a collapse in economic activity. Both business and consumer confidence languished at the lowest levels in over a decade, unemployment remained stubbornly high, and investors awaited relief from policy paralysis. The trust deficit stemming from poor governance is not as tangible as the current account and fiscal deficits, but is no less important. Some factors that we use to assess a country’s governance quality include: number of days required to start a new business – an indication of the degree of “red tapeism”; historical median term for each government – an indication of political risk; and judicial independence – an indication of the quality of institutions. The election of Cyril Ramaphosa as President has brought a palpable sigh of relief across the country. It is expected that he will reduce the governance discount, which has led businesses to underinvest for the last several years. A clear measure of the economic impact of governance is the radical turnaround of sentiment in the South African market. It underperformed the overall asset class every quarter of the year to end up significantly behind at the end of the first 3 quarters of 2017 (12.6% vs. 28.1%). But, in the fourth quarter, investors sensed that a change in governance might be forthcoming. They were proven correct in December; for the fourth quarter, the South African market handsomely outpaced the EM asset class as a whole with a return of 21.4% vs. 7.5%.

Assessing issuer level ESG risks: third-party ESG scores or proprietary scores?

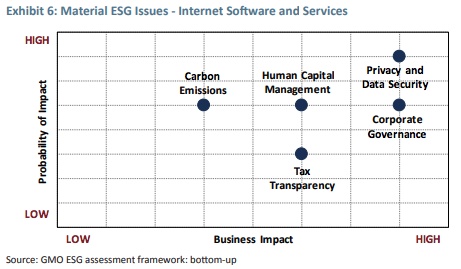

So, how does one go about assessing ESG risks and opportunities at the issuer level? The first, and probably most essential, step is to determine the set of material ESG risks (e.g., carbon emissions, physical impacts of climate change, occupational health and safety, product safety, data privacy and security, corporate governance, and corruption). Issue selection, as well as its relative importance, is a factor of the type of business lines in which a company operates, its geographical footprint, the severity of financial impact that the ESG issue itself may cause if not sufficiently managed, as well as the likelihood of and the time horizon over which, the financial impact is expected to occur. Time horizon is a relevant input, especially during integration, because there may be some issues that may impact a company’s short-term cash flows. Others have a longer time horizon, which will impact their terminal values in a discounted cash flow model. Once a set of ESG risks are identified for a company, a combination of qualitative and quantitative data points need to be assessed to determine whether a company manages its risk exposure sufficiently well or is vulnerable as a large portion of the risk remains unmanaged. After this exercise is carried out for all the different ESG risks to which a company is exposed, an analyst can then determine the company’s overall performance and the level of unmanaged risk that will be useful in making ESG adjustments to the financial model. Exhibit 6 represents an example of the list of material issues we have identified as a part of our internal materiality assessment framework for the Internet Software and Services sub-industry.

The relationship between corporate governance and financial performance has received considerable attention in emerging markets, and rightly so, as EM countries have had their fair share of controversies linked to a lack of independent board oversight, questionable ownership structures, and related party transactions. Relatively lower levels of transparency add to the complexity and, therefore, GMO has developed its own Corporate Governance (CG) assessment framework for emerging markets. This framework assesses over 50 indicators designed to determine whether there are any red flags related to board autonomy, ownership structure, related party transactions, capital allocation, executive compensation, auditor independence, taxes paid, and managing investor relations. This CG assessment forms a key part of our investment process in emerging markets.

While there is an increasing number of third-party rating agencies that provide both the raw data along with ESG ratings and commentary for a broad universe, we strongly believe that relying solely on these off-the-shelf ESG products is inadequate. This is because these products are designed to serve a wide variety of clients, each of whom may have different interests (say, impact investing vs. integration) and in the end they try to be “all things to all people.” Moreover, their assessment is often based on a long list of indicators, some of which may not necessarily have any substantial impact on a company’s financials and thus may distort the ESG signal, making the process of integration inefficient. Widespread use of off-the-shelf ESG products also makes it difficult for the rating agencies to quickly evolve their assessment frameworks because some clients may have been integrating a set of indicators in a specific manner historically. Modifying the assessment criteria or dropping the indicator altogether not only requires extensive client engagement, but also triggers a pushback because standard integration models need to be altered at the clients’ end. Therefore, in our view, it is best to focus the ESG analysis in each case on a small number of highly material ESG risks and opportunities that have the potential to make the biggest impact on the relevant company’s fair value. It is also important to reassess materiality on a periodic basis (say, annually) as it enables us to incorporate evolving ESG issues and increase their relevance over a period of time while dropping those that may no longer be material. Let’s see how ESG Integration plays out in practice using the case below.

ESG Integration Case Study: A Large Chinese Cement Manufacturing Company

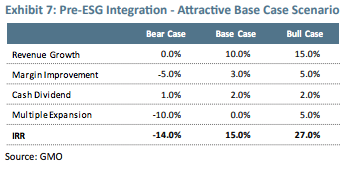

Case background: ESG performance assessment of a large cement manufacturer in China demonstrates unmanaged risks related to toxic emissions, energy use, carbon emissions, health and safety, as well as limited adoption of alternative/renewable sources of energy. During Q4 2017, by setting a carbon price on the country’s largest greenhouse-gas emitters, China has launched a new, crucial endeavor in its efforts to tackle pollution and climate change. While the first phase of the carbon market covers only power generation, subsequently, emissions from other carbon-intensive industries such as cement manufacturing will also be capped. Despite some ad-hoc initiatives, the company lacks firmwide programs to limit energy use or carbon emissions, thereby remaining exposed to increased costs to offset the excess emissions. The average price on carbon across seven pilot markets in China in 2017 was between $3 and $10 per ton of CO2. In addition, the company’s performance in managing toxic emissions as well as health and safety falls short of industry best practice, leaving it exposed to related risks. Exhibit 7 demonstrates how we integrate material environmental and social risks into our financial model for that company.

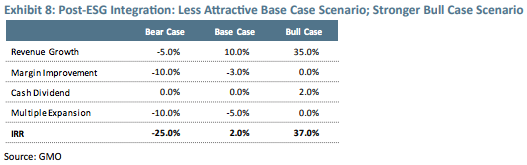

We assumed that compliance with national and provincial carbon regulations would require the company to increase spending on equipment, resulting in a 1% erosion in operating margin. Moreover, to limit toxic emissions, the company would have to switch to relatively cleaner sources of energy such as gas-based powered plants. This is expected to further dampen operating margin by 2% due to higher fuel costs. As a result of higher spending, we assumed that the previously stable cash dividend policy would turn conservative in the short term and hence the reduced dividend from 2% to 0%. Lastly, there is a downside to multiples as a result of the concerns related to management of health and safety risks as the company’s performance is below its peers’ and capital markets tend to discount the share price in the event of safety incidents. Based on all the above changes, the base case IRR for the cement company case became less attractive (see Exhibit 8).

It would be prudent to note that in the bull case we have assumed that the company management would take necessary steps to better manage some of the key ESG risks in the short term. Therefore, owing to its size and the fact that the Chinese government is pushing a supply side reform in the industry, the company might benefit from increased market share (assumed at 6%) as the uneconomical cement makers with marginal scale may not be able to cope with the stricter environmental regulations. This translates into a 35% top line growth; significantly higher than the 15% assumed in the bull case before ESG considerations. Lastly, the company has above-average corporate governance practices in the home market and hence is likely to improve ESG performance at a relatively faster pace. In this manner, key ESG risks and growth opportunities were integrated with traditional financial analysis to help arrive at a more robust investment decision.

Which strategies should integrate ESG signals?

We have shown above how ESG can substantially impact the purchasing power of residents and the earnings potential of corporations. This suggests that these signals could be used in all strategies. However, we believe there are some in which they are particularly effective. A prime example would be a concentrated, fundamental strategy that emphasizes quality growth. Here the larger weight on individual names and markets means a slip-up can be more expensive to the portfolio. Furthermore, the emphasis on quality and growth suggests that the valuations come with a premium. If it turns out that the perception of quality and/or steady growth is misplaced, the diminution of the associated premium can significantly impact the position. Finally, a fundamental approach makes it easier for an analyst, working alone or in tandem with an ESG expert, to uncover the ESG aspects of the company/country that are not already reflected in the price.

Even within fundamental strategies, one could argue that a strategy focused on the emerging consumer can especially benefit from incorporating ESG. Many investors are taken in by the fact that rising incomes have led to a jump in demand for all sorts of goods and services. We agree that emerging markets are currently in the sweet spot where some of the highest growth rates of consumption are typically observed. The drivers underlying the strategy are two powerful forces – economics and demographics. As poor countries get richer, they save as much as they can. Savings rates usually rise until countries reach a range of $3,000 to $10,000 per capita, at which point savers become consumers as society starts to provide a social safety net. The economic case is reinforced by a demographic one: a record number of people are coming into their earning years at the same time that the number of dependents is declining, yielding a powerful demographic dividend. These twin forces are generating a massive jump in demand for all kinds of goods and services.

However, as recent events in Brazil and South Africa have only too clearly proven, progress in emerging markets rarely follows a straight line. While the quality of institutions has improved over time, the caliber of policymaking in emerging markets is still very dependent on the government of the day. This introduces significant macroeconomic volatility that can buffet the fragile, emerging consumer and translate into uncertain prospects for companies relying on domestic demand. Therefore, we believe ESG integration is critical in helping to build a portfolio that can withstand these swings in macroeconomic and stock market volatility.

Conclusion/Key Takeaways

■ In recent years, responsible investing has gone mainstream, driven by two major global trends: the increasingly material financial impacts of mismanaging ESG risks and the rising decision-making power of millennials with their strong desire for sustainable investing. Both these trends are expected to gather pace in the future.

■ A thorough analysis should convince non-believers of the value in integrating ESG into investment decisions as it impacts security valuations through a host of avenues such as the volatility of earnings, resilience of assets, and the cost of capital.

■ Third-party ESG rating agencies serve a wide variety of clients and try to be “all things to all people.” Therefore, in order to differentiate and outperform, investment managers need to develop their own understanding of ESG issues by focusing on the aspects of ESG risks and opportunities that are material to their process.

■ EM countries are more vulnerable to the ill effects of ESG issues as they have far greater exposure to extreme weather events (e.g., floods, droughts); resource scarcity (e.g., water, food); social unrest; corruption; and poor governance.

■ There is a wide range of ESG performance levels in the EM basket, offering active managers the opportunity to add value along both the country allocation and the stock selection dimension. You can do well by doing good.

Binu George. Mr. George is a portfolio strategist for GMO’s Emerging Markets Equity team. Prior to joining GMO in 2009, he was a portfolio manager with AXA Rosenberg. Previously, Mr. George worked in several roles encompassing research and investment strategy at Barclays Global Investors. Mr. George earned his B.Tech. in Civil Engineering from Indian Institute of Technology, Madras and his MBA in Finance from University of Rochester. He is a CFA charterholder.

Hardik Shah. Mr. Shah is the ESG Practice Manager at GMO. Prior to joining GMO in 2017, he was manager of Environmental, Social and Governance Research at Sustainalytics. Previously, he was an associate in ESG Ratings at MSCI Inc. Mr. Shah earned his Bachelor of Engineering in Electronics from University of Mumbai. He is a CFA charterholder.

Disclaimer: The views expressed are the views of Binu George and Hardik Shah through the period ending March 2018, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2018 by GMO LLC. All rights reserved.

1 Global Sustainable Investment Review 2014, 2016

2 https://www.unpri.org/directory/ (Accessed March 6, 2018.)

© GMO

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits