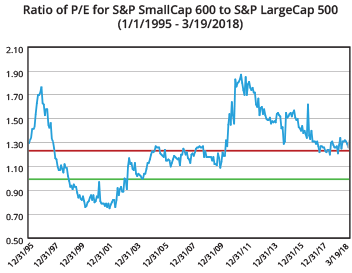

While ICON does not use the Price-Earnings (P/E) Ratio for individual stock selection or overall market pricing, we do believe it can be useful for direct comparisons. The graph shows the ratio of the P/E of the S&P SmallCap 600 Index (the Small 600) to the P/E of the S&P LargeCap 500 Index (the Large 500) from the inception of the Small 600, January 1995. The green line in the graph is 1.00, where the two ratios would be equal. Over this period, the ratio of the P/E of the Small 600 to the P/E of the Large 500 is usually above 1.00, meaning that typically the P/E for small-cap stocks is greater than the P/E for large-cap stocks. This makes sense as small-cap stocks generally have faster growing earnings and, mathematically, the rate of growth of earnings per share is one component of P/E. The red line on the graph is the average ratio of the P/E of the Small 600 to the Large 500 over the twenty-three year period. The average of 1.25 over the period suggests that on average, the P/E ratio of the Small 600 is about 25% higher than the Large 500.

Small-cap stocks did well in the early 1990s, which drove them to a relatively expensive level by 1996. At its highest point during this period, the P/E on the Small 600 was over 1.7 times that of the P/E on the Large 500. Then in the late 1990s, large-cap stocks surged in popularity. In 1999 and 2000 the P/E of the Large 500 was about 25% higher than the P/E of the Small 600. Following that expensive perch for large caps, the ratio of P/Es moved back toward equal, at first, and then closer to the neutral or historic average range. It is interesting that from February 2003 to October 2007, the Small-Cap 600 gained about 144%, beating the Large-Cap 500, which gained about 100%. Perhaps neutral or average readings is all it takes for small caps to exert their long term advantage.

As the market rallied off its recession lows of March 2009, it appears the Small 600 surged ahead of its earnings growth, taking its P/E to 1.8 times that of the Large 500. Since that peak of small-cap stocks’ lofty pricing, large-cap stocks have outperformed from 2011 through 2015. Now, however, the ratio is back near its historic average.

This relative pricing does not suggest a huge advantage for small-cap stocks as the conditions of 1999 and 2000 did. It simply suggests that small-cap stocks are not at the pricing disadvantage they were in 1996 and 2010. We first published this paper when the relative ratio crossed below its historic average on a monthly basis at the end of February 2016, just as the market hit a short term low and rebounded. The Small-Cap 600 Index beat the large cap 500 Index over the remainder of 2016. Then in 2017, performance reversed and large caps beat small caps. For two years with the ratio of the P/Es on small caps to large caps in their historic neutral ranges, we have experienced alternating leadership. Perhaps that is rational when the reading is historically neutral. Just as in 2016, small caps are leading large caps off the February low of 2018.

It is too early to tell if one month of neutral or average readings is the start of something, but off the low of February 11, 2016, through March 11, 2016 the S&P SmallCap 600 Index has gained 13.9%, outpacing the 10.8% gain on the S&P LargeCap 500 Index.

To Learn More about ICON Advisers visit our News and Views page.

To Learn More about ICON Advisers visit our News and Views page.

Or for more information contact ICON at 1.800.828.4481.

Want to Learn more about the entire lineup of ICON funds?

Email the ICON Sales Desk.

Craig Callahan, DBA, is founder and president of ICON Advisers, Inc.

Data quoted is past performance, which does not guarantee future results.

Opinions and forecasts are subject to change at any time, based on market and other conditions, and should not be construed as a recommendation of any specific security, industry, or sector.

The unmanaged Standard & Poor’s (S&P) 500 Index is a market value-weighted index of large-cap common stocks considered representative of the broad market. The unmanaged Standard & Poor’s (S&P) SmallCap 600 Index is an unmanaged index of 600 domestic stocks chosen for their market capitalization, liquidity, financial viability, and sector representation.

Price/Earnings Ratio is the price of a stock divided by its earnings per share.

Investing in securities involves risks, including the risk that you can lose the value of your investment. There is no assurance that the investment process will consistently lead to successful results. Individuals cannot invest directly in an index.

Please visit ICON online at www.iconadvisers.com or call 1-800-828-4881 for the most recent copy of ICON’s Form ADV, Part 2.

© 2018 ICON AdvisersSM All Rights Reserved