“Go West, young man” was advice popularized in the late 1800s by the American author and newspaper editor Horace Greeley in regards to America’s Westward Expansion.1 Greeley “saw the fertile farmland of the west as an ideal place for people willing to work hard for the opportunity to succeed.”2 Potential success, measured in terms of productive land to farm, luxurious furs to trap, and of course shiny gold to pan, enticed many Western settlers to take significant risks.

Investing requires bearing risk to reap rewards, but there is no definitive causal relationship here. Just because you might be willing to pack up your wagon and head off into the sunset doesn’t ensure you’ll be rewarded with wealth. Today investors should be particularly diligent in assessing risk before setting off on any journey.

On the one hand, the road out of town looks inviting: global economies are growing synchronously, many leading indicators including global Purchasing Managers Indices remain robust, earnings have been strong with expectations anchored around continued growth, and inflation generally remains contained. Looking toward the horizon, however, we can see dark storm clouds building: labor conditions in the U.S. have been tightening while more fiscal spending is on tap (all being a potential precursor to higher inflation levels), and the Fed has pivoted from quantitative easing to tightening and is hiking rates. The scariest storm, chock-full of lightning strikes and cacophonous thunder, for the adventurous traveler though, is the elevated valuation levels of assets across the board.

This is not the time to pack a knapsack with limited provisions, straddle a horse, and gallop off. It is a time to be well prepared for the harsh conditions of a long westward journey. To be clear, we are not counseling investors to avoid all risks right now. We are simply pointing out that it is more important than ever to do so in an intelligent manner.

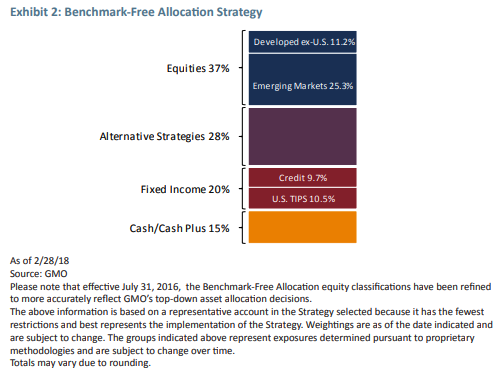

What does intelligent investing look like to us? It means investing where you have a fighting chance to make decent returns and harbor a margin of safety. As valuations have continued to climb higher and prospective returns lower, our Benchmark-Free Allocation Strategy (“BFAS”) has become more provocatively positioned: we are lighter in equities with an even heavier concentration in emerging markets; we have more weight in alternative strategies; and we are still carrying meaningful cash/ cash plus exposure.

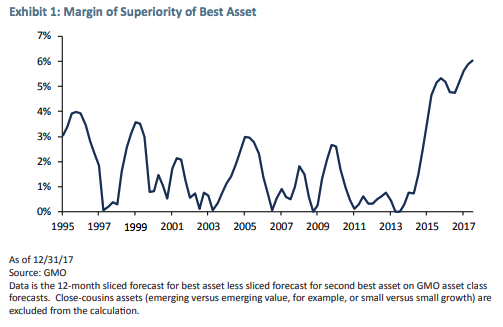

In equities, we think emerging market value stocks are the only asset priced near fair value, offering up mid-single-digit forecasted real returns. While that sort of absolute forecast is good, though certainly not great, the wide spread of GMO’s emerging markets value forecast relative to the next best asset class is impressively wide today (see Exhibit 1). Combining this attractive spread opportunity with an otherwise paltry opportunity set and low exposure to equities in general is leading us to significantly concentrate our 37% equity weight. After Quality stocks continued to rally through January, our forecasts for the group fell, leading us to sell down our remaining long Quality equity position (though we retain exposure to a beta-neutral expression of Quality, per below). BFAS presently holds only non-U.S. equities, with 25% in emerging value and 11% in developed ex-U.S.

Another approach to investing intelligently means finding other ways to get paid for risk in a manner that can diversify a portfolio away from today’s threats of elevated valuations and rising discount rates. Alternatives can play such a role and have grown to 28% of our portfolio. The growth in our alternatives sleeve came from the recent addition of a long Quality / short S&P position, which provides exposure to the alpha opportunity offered by our Quality positions and the spread between our relative forecasts while limiting the underlying sensitivity to stocks, which are generally expensive.

While equities can be thought of as one somewhat monolithic bucket exposed to depressions and growth shocks, alternatives are heterogeneous in nature and require careful analysis and portfolio construction. On the one hand, most alternatives are less valuation sensitive than stocks (or bonds for that matter today), have lower durations, less equity beta, and can help diversify traditional portfolios. Alternatives, however, do not offer a silver bullet and come with their own issues as they tend to be more complicated to implement, more path dependent, and more reliant on manager skill. Acknowledging and managing these issues is imperative, and requires a skilled team and rigorous process. Managing risk is an intelligent thing to do in any environment, but particularly so in today’s world of expensive assets with limited opportunities and thin margins of safety.

Intelligent investors can learn another lesson from our pioneering ancestors. Successful trailblazers recognized the importance of patience in reaching their long-term destination. Rather than climb a snowy pass in treacherous conditions, they waited for the weather to clear. Our 15% cash/cash plus position represents such patience (see Exhibit 2). We know it might slow our journey, but it is essential in helping us get there. Cash will provide a store of value in a large drawdown, and important optionality once skies clear and asset prices are more attractively priced.

While today’s investment landscape may not be as wide-open and promising as the westward view in the mid to late1800s, there are pockets of opportunity for which investors should be willing to bear risk. However, given that they are few and far between, perhaps the greatest risk worth taking is choosing the road less travelled and bearing the inevitable career risk that comes with holding a portfolio that looks substantially different from the average investor’s.

Rick Friedman. Mr. Friedman is a member of GMO’s Asset Allocation team. Prior to joining GMO in 2013, he was a senior vice president at AllianceBernstein. Previously, he was a partner at Arrowpath Venture Capital and a principal at Technology Crossover Ventures. Mr. Friedman earned his B.S. in Economics from the University of Pennsylvania and his MBA from Harvard Business School.

Disclaimer: The views expressed are the views of Rick Friedman through the period ending March 2018, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2018 by GMO LLC. All rights reserved.

1 The phrase was first stated by John Babsone Lane Soule in an 1851 editorial in the Terre Haute Express, “Go west young man, and grow up with the country.” Wikipedia contributors. “Go West, young man.” Wikipedia, The Free Encyclopedia, 1 Mar. 2018. Web. 13 Mar. 2018.

2 Ibid

© GMO

Read more commentaries by GMO