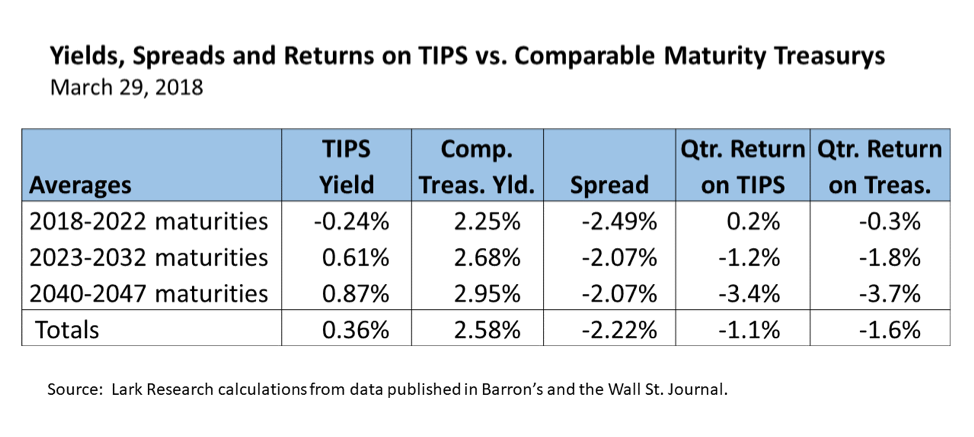

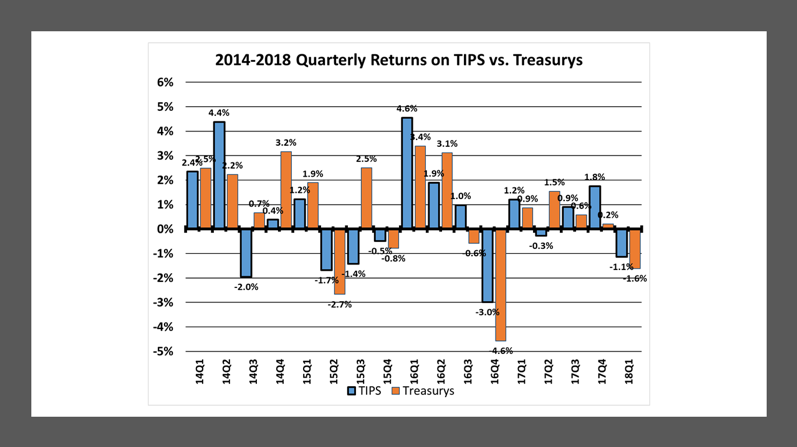

- TIPS on average declined 1.1% on the 2018 first quarter, less than the 1.6% decline in comparable maturity straight Treasurys.

- The average breakeven spread widened to 222 basis points from 184 basis points at the end of the 2017 fourth quarter.

- Most of the widening was due to a sharp drop in short-maturity TIPS yields, as investors sought a safe haven in a rising interest rate environment.

- With interest rates backing off a bit, longer-term TIP offer better relative value, but they will still be vulnerable to declines, if interest rates continue to rise.

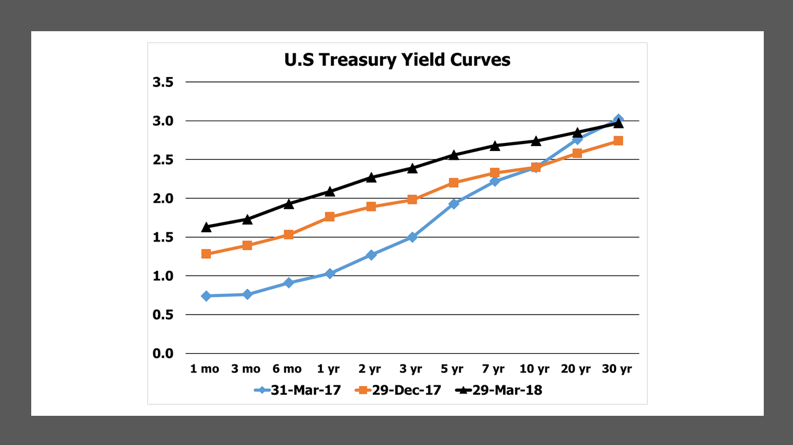

In a quarter characterized by rising interest rates, TIPS outperformed comparable maturity straight Treasurys, but still produced a negative return. On average, TIPS fell 1.1%, less than the 1.6% decline in comparable maturity straight Treasurys. During the quarter, the average yield on TIPS rose by two basis points (bp) to 0.36%, while the average yield on straight Treasurys increased by 40 bp to 2.58%. As a result, the average spread between straight Treasury and TIPS yields increased by 38 bp from 184 bp to 222 bp.

Given the sharp increase in the yield spread, I was somewhat surprised to see the relatively small performance differential between TIPS and straight Treasurys. Intuitively, TIPS should have performed much better. That anomaly caused me to double check my yield and return performance calculations.

For the record, my calculations exclude the newly issued TIPS, primarily because their returns over a partial quarter were affected significantly by where they were priced at issuance. Including them, I believe, would have distorted the average performance for the TIPS universe.

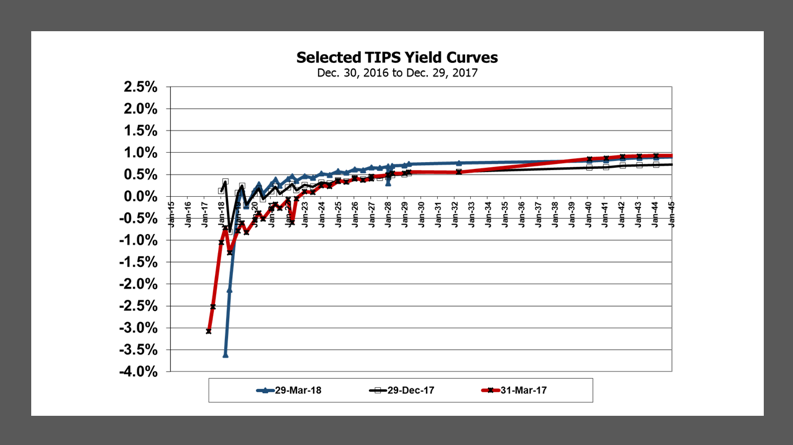

The Treasury-TIPS yield (or breakeven) spread widened primarily because the average yield on short maturity TIPS, declined by 31 bp to -0.24%. Average yields in all other maturity categories for both TIPS and straight Treasurys increased during the quarter (by about 15-25 bp for TIPS and 25-35 bp for straight Treasurys).

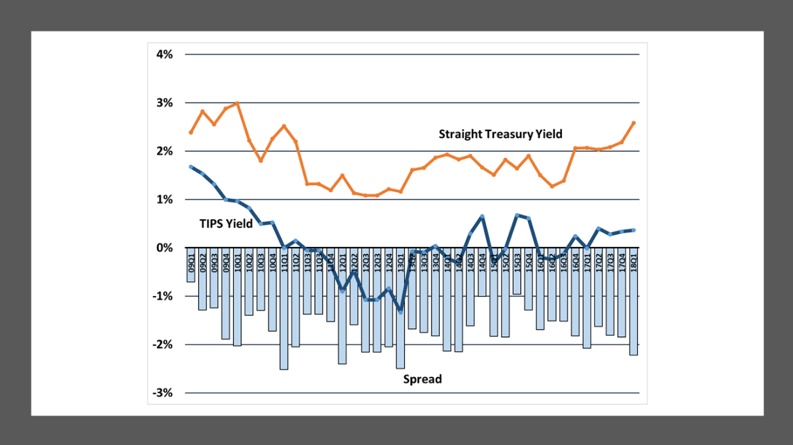

The decline in short-maturity TIPS yields widened their spread vs. Treasurys by a whopping 86 bp to 249 bp. That is 116 basis points above the average spread and close to the maximum spread of 267 bp over the past decade.

With interest rates generally on the rise and increasing concerns about a pick-up in inflation, investors apparently flocked to short-maturity TIPS as a safe haven. Since peaking in late February, however, intermediate and long-term interest rates have moderated. Short-maturity TIPS yields also increased (i.e. became less negative) by about 5-10 basis points from late February to the end of March, which is roughly in line with the decline in Treasury yields.

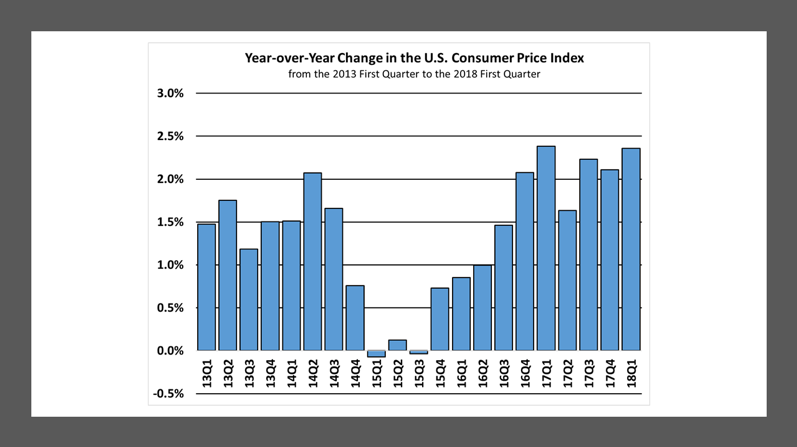

Furthermore, even though the Consumer Price Index has risen at a progressively faster pace in each month this year, the monthly year-over-year increase has been lower than in 2017. (Short-maturity TIPS yields were more negative at the end of the 2017 first quarter, but the breakeven spread was about 100 bp lower at 144 bp).

Of course, inflation could pick up more from in the weeks and months ahead, but I believe that the data do not currently make a strong case for that. Consequently, I think that the chances are good that the breakeven spread between short-maturity TIPS and Treasurys will moderate over the next quarter or two, which should bring it back in line with the spreads on intermediate- and long-term TIPS vs. Treasurys.

At the current time (as of March 29), the best relative value in the TIPS sector is in the longer maturities, where breakeven spreads are close to their 10-year historical average. By comparison, short-maturity TIPS spreads are well above their historical average (as already noted) and intermediate-term TIPS spreads at 207 bp are about 25 bp above their historical average.

Said another way, current buyers of short-term TIPS should be confident that short-term inflation expectations will rise in the months ahead.

Of course, if interest rates do continue to rise, TIPS probably will still deliver negative returns, but assuming no decline in inflation expectations, the losses on TIPS will probably not be as large as those on straight Treasurys.

© Lark Research

Read more commentaries by Lark Research