April 2018 Economic Outlook

Membership required

Membership is now required to use this feature. To learn more:

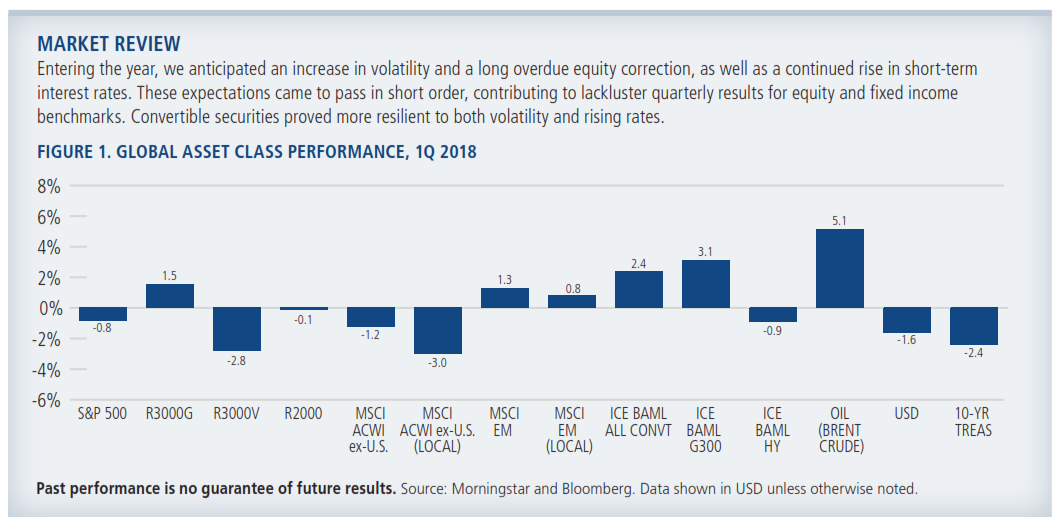

View Membership BenefitsDuring the first quarter, volatility returned to the markets in dramatic fashion. Despite generally positive economic data and healthy corporate fundamentals, markets gyrated as investors confronted the likelihood of more Federal Reserve hikes and rising inflation. The shifting terrain may be jarring for some, but the conditions we are seeing today are more normal than recent years, when investors grew accustomed to record low interest rates, a near-absence of inflation and the subdued volatility. As a more typical environment emerges, our positioning reflects the following beliefs:

- Coordinated global economic expansion will continue through 2018, although improvements in some economic fundamentals may have peaked. The pace of growth among economies will likely be more varied than in 2017.

- The near-term risk of a U.S. recession is very low. Inflation and short-term interest rates will rise but are unlikely to soar out of control in 2018.

- The bull market has more room to run, supported by positive economic conditions and corporate fundamentals. Volatility is unlikely to return to unusually low levels, however.

- In advancing but choppy markets, opportunities increase for active and risk-aware approaches.

Evolving trade policies, uncertainties around North Korea, Russia and Syria, and U.S. mid-term elections will fuel short-term market disruptions over these next months. Fears of a trade war have risen in the markets, but we believe Washington’s recent moves can set the stage for negotiations that lead to freer and fairer trade over the long term.

United States

We see very low risk of an imminent U.S. recession. GDP growth has continued at a good clip in the U.S., and tax reform and deregulation can provide further catalysts from here. With tighter labor markets and increased incentives to make capital expenditures, we expect U.S. businesses to re-invest in their businesses at higher rates than recent years. While we are monitoring a falling savings rate as a potential signpost of weakness, the U.S. consumer looks to be in good shape overall, benefiting from job growth, wage gains and rising housing values.

Corporate fundamentals—including earnings, sales and revenue growth—are very strong, and equity valuations look more reasonable due to the tailwinds that tax reform provides corporations. We expect good company earnings announcements to steady the U.S. equity market and push it higher. That said, year-over-year comparisons are likely to become harder as time progresses, given the healthy growth expected over the nearer term.

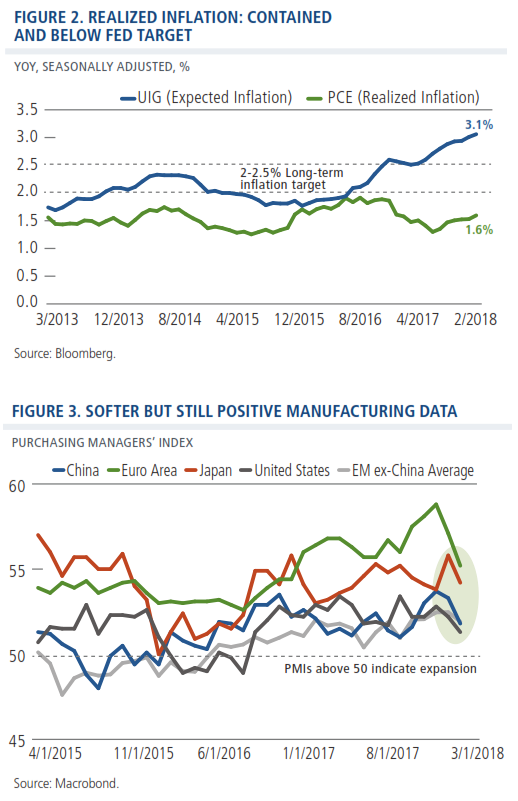

There is every reason to expect inflation will continue rebounding as slack in the U.S. and global economies decreases. At this point, the trend merits close monitoring, but not consternation. Inflation is coming off historically low levels and remains contained, with realized inflation readings significantly trailing expected inflation (Figure 2). As economic growth continues, the Fed is likely to maintain a gradual course. We anticipate at least two more short-term interest rate hikes in 2018, with the yield curve flattening as global bond markets hold U.S. long-term rates in check.

In an environment of continued economic growth and more normal interest rates, the bond surrogate trade is over. As the search for income becomes easier, it should be less of a dominant focus in the equity market. Cyclical growth sectors should enjoy greater market recognition, with utilities and real estate coming under increased pressure. We believe many of the technology growth names that sold off in the wake of negative headlines will stabilize. Through the remainder of the bull market, we could well see a narrowing of leadership across all sectors, which would benefit active managers.

Global and International Strategies

Major global economies are positioned for growth, although softening data suggests that the improvements in economic fundamentals may well have peaked. PMI data points to a slower rate of manufacturing activity (Figure 3), and positive economic surprises have fallen. Liquidity conditions have tightened at the margin (primarily in the U.S. and China), and geopolitical risks remained heightened. In addition to those risks we already noted, we are vigilant to the potential for an unexpected ECB tightening, and elections in Italy, Brazil and Mexico.

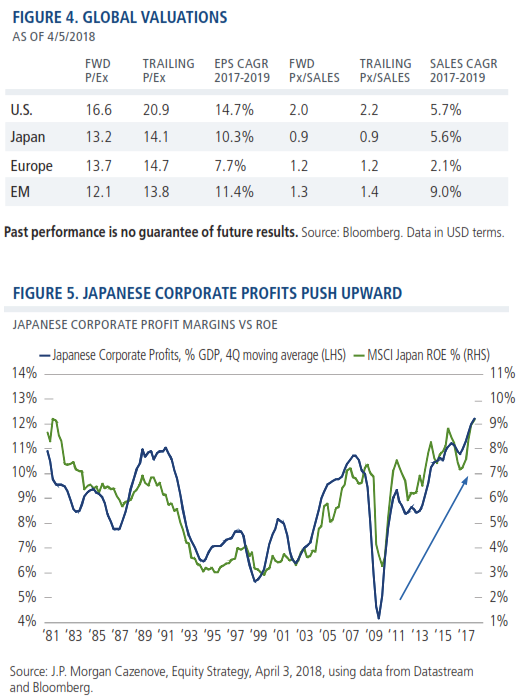

Global equities can still do well in this slower-growth environment, supported by attractive valuations and growth metrics (Figure 4). We have sought to build in greater resilience to downside equity moves, broadly favoring a mix of secular growth and cyclical growth names. We remain constructive on the emerging markets, with Chinese companies among those especially well represented in our portfolios. We expect Chinese economic data to be more mixed than in 2017 as targeted tightening works its way through the economy, but we have found names that offer attractive valuations and strong earnings prospects. These include technology companies that provide exposure to several of our favorite secular growth themes, as well as home-court advantage over U.S. counterparts in understanding how to navigate the domestic market. Further, China continues with initiatives that will enhance the long-term stability of its markets and economy, including reducing its dependence on the U.S. dollar through the expansion of renminbi-denominated securities.

Within the developed markets, Japan offers attractive valuations and favorable liquidity conditions. Although economic fundamentals remain challenged, many companies have put capital to good use and have seen profits soar (Figure 5). We have sourced a number of growth opportunities in Japan, including worldwide leaders in robotics and automation. By favoring multinational companies benefiting from improving global growth, we have also reduced exposure to the domestic economy. In contrast, in Europe we have favored small and mid cap companies over large-cap multinationals with more vulnerability to rising rates and a stronger euro.

Convertible Securities

During a difficult quarter, the U.S. and global convertible markets posted positive returns, diverging from the losses in the equity and bond markets. We expect convertible securities to perform well in this environment. With attributes of stocks and fixed income securities, convertibles tend to benefit from upward moving but volatile equity markets. (Since the March 2009 low, there have been 20 corrections of 5% or more in the U.S. stock market, and convertibles have outperformed equities through 19 of those periods.) Moreover, convertibles’ equity characteristics may make them less vulnerable than investment-grade bonds to rising interest rates.

However, in a period of rising rates and elevated equity market volatility, active management is especially important for maximizing the potential benefits of the convertible structure. Convertibles vary in their degree of equity and fixed-income sensitivity. Securities with the highest levels of equity sensitivity may fail to provide adequate downside protection, while those with the lowest levels may be sidelined during upswings. In our positioning, we seek to capture the majority of equity upside, with better potential downside protection than both the overall equity and convertible markets. Reflecting these considerations, we continue to favor balanced structures, emphasizing the technology and consumer discretionary issues. We are more cautious regarding defensive sectors, where convertible structures tend to be more bond-like and therefore, less likely to participate in the rising equity market we expect.

The global new issuance market got off to a brisk start during the first quarter as $27.8 billion came to market. The U.S. set the pace ($13.7 billion), with cloud computing companies especially well represented. We expect a strong stream of issuance for the remainder of 2018, as companies seek new growth capital and refinancing for maturing securities. As we noted earlier this year, U.S. issuance could ramp up in the wake of tax reform. Interest deductibility caps provide additional incentive for companies to issue convertibles rather than straight bonds. Further, if repatriated funds catalyze M&A activity, acquiring companies may choose to shore up their balance sheets by issuing convertibles.

Fixed Income

After years of unprecedented conditions, Fed rate hikes have begun to work their way through the economy, inflation is trending upward and financial conditions have begun to tighten from extraordinarily loose levels. While many market participants expect Chair Powell will take a more hawkish tone than his predecessor, we believe a gradual path remains most likely: two additional Fed hikes this year and a “Chairman’s choice” in December, dependent on the economic environment.

In high yield, we anticipate gradual, further softening in credit spreads, but view some out-of-favor areas as a source of idiosyncratic opportunities, while fundamentals are strong. The high yield market may face challenging technicals, such as decreased demand from foreign investors. We expect the default environment to continue to trend below the long-term historical average of 3%. Although several large, well-telegraphed distressed situations are expected to default in 2018, these have been anticipated for some time and are not expected to dramatically change an otherwise positive fundamental environment.

Following the Financial Crisis, historically low interest rates and extraordinarily accommodative liquidity drove investors to seek out bonds for appreciation and stocks for income. In a more normalized interest rate environment, we would expect a return to the traditional relationship, with fixed income allocations still providing valuable benefits: diversification from equity market volatility and a source for income. However, given the crosscurrents associated with this shift back to normal, an experienced and active approach remains essential to ensure appropriate compensation for potential risks.

Conclusion

We may not have yet seen the bottom of this current correction, but we believe the duration of the downturn will be relatively short lived. Our teams are using short-term volatility to our advantage—rebalancing our positions, locking in gains, and striking the risk /reward profile we believe is appropriate for this climate. We encourage investors to maintain a long-term approach and resist the urge to make short-term moves. More often than not, trying to time the ups and downs results in being whipsawed—capturing the downside and missing the upside. Instead, managing volatility will be key to succeeding in this environment.

Having invested through more than 40 years, we believe we are well equipped to navigate the course ahead. We welcome the return of more normal levels of volatility and the opportunities it will bring for our active approach.

Indexes are unmanaged, not available for direct investment and do not include fees and expenses. The U.S. Dollar Index measures the value of the U.S. dollar relative to a basket of foreign currencies, including Euro Area, Canada, Japan, United Kingdom, Switzerland, Australia, and Sweden. The Russell 3000 Growth Index and Russell 3000 Value Index measure U.S. growth and value equities, respectively. The Russell 2000 Index measures U.S. small cap stock performance. The S&P 500 Index is considered generally representative of the U.S. equity market. The MSCI All Country ex U.S. Index represents the performance of global equities, excluding the U.S. The MSCI Emerging Markets Index is a measure of the performance of emerging market equities. The ICE BofAML U.S. High Yield Index is an unmanaged index of U.S. high yield debt securities. The ICE BofAML All U.S. Convertible Index (VXA0) is a measure of the U.S. convertible market. The ICE BofAML G300 Index measures the performance of 300 global convertibles. Oil is represented by current pipeline export quality Brent blend. Core PCE is a gauge for inflation, measuring personal consumption expenditures excluding food and energy prices.

Purchasing Managers Indexes measure manufacturing sector strength. The Underlying Inflation Gauge seeks to capture sustained movements in a broad set of prices, incorporating additional macroeconomic and financial variables. ICE Data: Source ICE Data Indices, LLC, used with permission. ICE permits use of the ICE BofAML indices and related data on an `as is’ basis, makes no warranties regarding same, does not guarantee the suitability, quality, accuracy, timeliness, and/or completeness of the ICE BofAML Indices or data included in, related to, or derived therefrom, assumes no liability in connection with the use of the foregoing and does not sponsor, endorse or recommend Calamos Advisors LLC or any of its products or services.

Earnings per share (EPS) is a company’s profit divided by its number of outstanding shares. Price-to-earnings ratio (P/E) is a valuation ratio of a company’s current share price compared to its per-share earnings; forward P/Es are based on forecasted earnings. CAGR, or compounded annual growth rate measures year-over-year growth. Price-to-sales ratio measures a company’s stock price versus its revenues. Hawkish refers to economic policy that supports higher rates to keep inflation in check.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be suitable for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

This material is distributed for informational purposes only. The information contained herein is based on internal research derived from various sources and does not purport to be statements of all material facts relating to the information mentioned and, while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

©2018 Calamos Investments LLC. All Rights Reserved.

Calamos and Calamos Investments are registered trademarks of Calamos Investments LLC.

OUTLKCOM 18631 0418O C

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All