Bitcoin is back in the news in a big way. The world’s largest cryptocurrency neared $10,000 this week, meeting strong 200-day moving average resistance of around $9,800. Also this week, the 17 millionth bitcoin was mined. Remember, the crypto was originally designed to have a limited supply of “only” 21 million, an attractive feature that should continue to burnish its value as we get ever closer to that ceiling.

It’s no coincidence that the rally we’re seeing right now began soon after Tax Day. Many bitcoin and altcoin investors likely liquidated some of their holdings ahead of the filing deadline to cover capital gains taxes from last year and are now getting back into the trade. Month-to-date as of April 27, bitcoin was up more than 33 percent.

Also moving prices is news that Goldman Sachs and Barclays are both rumored to be working on introducing cryptocurrency trading desks. Similarly, Nasdaq CEO Adena Friedman told CNBC this week that Nasdaq “would consider becoming a crypto exchange over time,” and that “digital currencies will continue to persist.”

As I see it, these are huge steps for the crypto market to take on its path to full maturation and acceptance as an asset class. We’re still in the very early stages, and recent calls that “bitcoin is dead,” not to mention general negativity toward bitcoin in the media, are strikingly premature.

I’m bullish, but I don’t expect bitcoin to test $20,000 again in the short term, especially before July. That’s when G20 finance ministers are scheduled to present their recommendations on how cryptocurrencies should be regulated.

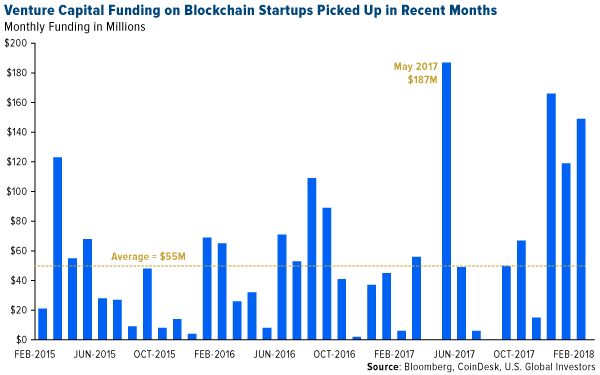

More and More Smart Money Flowing into Cryptocurrency and Blockchain Tech

As I’ve said before, I don’t necessarily see regulation as a major headwind to cryptocurrencies, so long as it’s fair and reasonable. Such rules might even spur some investors, who until now have been watching from the sidelines, to participate.

That includes hedge funds, financial firms and other large institutional investors. A recent Thomson Reuters survey found that one in five firms are planning to trade altcoins this year. Of those, about 70 percent said they would do so in the next three to six months. Clearly, an increasing number of big investors see cryptocurrencies as an opportunity too good to pass up.

More and more money from venture capital firms is also being plowed into startups focused on cryptocurrency and blockchain technology. In the three months through February, the amount of capital flowing into blockchain businesses far exceeded the monthly average of $55 million for the three-year period. Momentum is building.

And it’s not just “dumb money” making these bets. Bloomberg reports that successful venture capital firm Venrock Associates is ready to start speculating in the space. Venrock, a compound of “Venture” and “Rockefeller,” was founded in 1969 by members of the wealthy Rockefeller family, and it has a stellar track record for investing early in wildly profitable companies, including Apple and Intel.

Bitcoin to Meet Growing Demand for Alternative Payment Systems

One of the most bullish crypto participants right now is venture capitalist Tim Draper, an early investor in Hotmail (since acquired by Microsoft and renamed Outlook), Skype (also purchased by Microsoft) and Tesla (not currently owned by Microsoft, as far as I know). Last weekend at an Intelligence Squared debate in New York, Draper made the bold claim that bitcoin is bigger than those three ventures combined. “Bigger than the Industrial Revolution,” he said.

Further, he doubled down on his bullish call of $250,000 per coin in the next four years, and predicted that fiat currency will disappear much faster than expected.

“In five years, you are going to try to go buy coffee with fiat currency and they’re going to laugh at you because you’re not using crypto,” he said.

No doubt some of you reading this are laughing at Draper’s hyperbolic claims. But as I’ve written before (here and here), there’s already a global war on cash, incited by some central banks, economists and policymakers.

To try to prevent terrorism financing and drug trafficking, the eurozone has already scrapped the 500 euro note. India did the same with its 500 and 1,000 rupee notes to combat corruption. (See the dramatic dip in the chart below.) And Sweden, one of the first countries to experiment with paper currency, could soon become the first to eliminate it altogether and rely exclusively on electronic payment systems. (Again, notice Sweden’s steady slope toward 0 percent of GDP.)

Here in the U.S., the $100 bill’s days might be numbered, which would affect not only America but also many countries where Benjamins are still in high demand. In fact, more than three quarters of all $100 bills in circulation today live outside the U.S., according to the Federal Reserve Bank of Chicago.

|

Banning large denomination banknotes might be well intended, but ultimately it debases people’s economic freedom. This becomes especially true when low to negative interest rates are also introduced, as they are in Japan. (Today, in fact, the Bank of Japan announced it would keep its short-term rate at minus 0.1 percent.)

The demand for other liquid assets and “alternative technologies for making payments,” as the Chicago Fed puts it, is therefore surging, and I expect digital currencies such as bitcoin and Ethereum to fill that need. Today, U.S. currency in circulation stands at $1.59 trillion. According to one estimate by the Chicago Fed, that figure could sink to as low as $501 billion within 10 years as altcoins become more widely used to make transactions.

In a report for the second quarter, the St. Louis Fed likewise predicts a rapid transition from cash to cryptos:

In the near future, a close cash substitute will be developed that will rapidly drive out cash as a means of payment. A contender is Bitcoin or some other cryptocurrency. While cryptocurrencies still have many drawbacks… these issues could rapidly disappear with the emergence of large-scale off-chain payment networks (e.g., Bitcoin’s lightning networks) and other scaling solutions.

Maybe Tim Draper is onto something!

Have a great weekend!

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.62 percent. The S&P 500 Stock Index fell 0.01 percent, while the Nasdaq Composite fell 0.37 percent. The Russell 2000 small capitalization index lost 0.50 percent this week.

- The Hang Seng Composite lost 0.14 percent this week; while Taiwan was down 2.1 percent and the KOSPI rose 0.65 percent.

- The 10-year Treasury bond yield fell 0.3 basis points to 2.958 percent.

Domestic Equity Market

Strengths

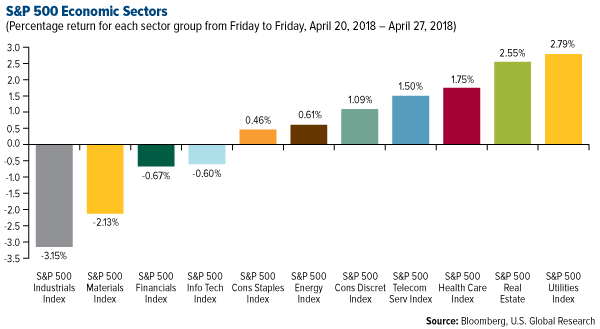

- Utilities was the best performing sector of the week, increasing by 2.8 percent versus an overall increase of 0.05 percent for the S&P 500.

- Chipotle was the best performing stock for the week, increasing 28.74 percent.

- A heated debate lasted for months over whether companies would hand the biggest tax break in three decades back to shareholders or reinvest it in its businesses. Finally, there’s finally some hard data. Among the 130 companies in the S&P 500 that have reported results in this earnings season, capital spending increased by 39 percent, the fastest rate in seven years, according to data compiled by UBS AG show.

Weaknesses

- Industrials was the worst performing sector for the week, decreasing by 3.15 percent versus an overall increase of 0.05 percent for the S&P 500.

- Freeport-McMoran was the worst performing stock for the week, falling 20.84 percent.

- Shares of LKQ – a global distributor of automotive replacement parts, components, and systems – fell 17 percent after the company posted a worse-than-expected first quarter due to rising costs.

Opportunities

- A surge in U.S. 10-Year Treasury yields to above 3 percent suggests a bullish outlook for commodities, according to Bloomberg Intelligence. The Bloomberg Commodity Spot Index is lower now than in 2014 when yields last topped 3 percent. With a strengthening global economy, recent gains in crude oil, a pickup in inflation and a weakened dollar, strategist Mike McGlone believes commodities are poised to rise further. This would greatly benefit commodities stocks.

- T-Mobile and Sprint may complete a deal as early as next week. T-Mobile owner Deutsche Telekom and Softbank, the Japanese holding company that controls Sprint, are working on a deal that would allow Deutsche Telekom to bring a combined company onto its books without majority control, Reuters says.

- Amazon blew past Wall Street estimates, earning $3.27 a share on revenue of $51 billion, easily beating the $1.26 and $49.96 billion that Wall Street was expecting. Additionally, the company said it expects groceries and household products to account for half its business in India in the next five years. The company hinted that it would bring AmazonFresh to the country.

Threats

- As the 10-Year Treasury yield flirts with 3 percent and S&P 500 earnings are about as good as they'll get, a third factor is curbing investors' appetite for stocks according to Bloomberg Intelligence strategists Gina Martin Adams and Peter Chung. The expected windfall from the U.S. tax overall hasn't helped share-buyback announcements, which are at new cycle lows. The index's shareholder yield (dividend plus buyback yield) is feeling the effects, remaining near 2010 lows. While short-term earnings positives are clear, longer-term benefits to the broader economy and shareholders remain elusive. Until this changes, stocks could remain stuck in a rut.

- For the first time since the 2016 election, more Americans expect stocks to fall over the next 12 months than rise, according to the Conference Board's Consumer Confidence survey in April.

- Caterpillar warned its first quarter earnings represent a “high watermark” for the year. While the maker of large industrial equipment beat on both the top and bottom lines, its shares tumbled more than 6 percent after executives on the conference call warned the first quarter was as good as it’s going to get this year.

The Economy and Bond Market

Strengths

- The first reading on first-quarter gross domestic product (GDP) growth came in at 2.3 percent versus expectations of 2.0 percent.

- U.S. new-home sales increased in March to a four-month high, mainly reflecting a surge in the West, and upward revisions to prior months showed stronger first-quarter demand than previously estimated, according to government data.

- Home prices in 20 U.S. cities grew in February at the fastest pace since mid-2014, underscoring the persistent scarcity of inventory amid strong demand, according to S&P CoreLogic Case-Shiller data. The 20-city property values index increased 6.8 percent from a year earlier, faster than an estimated 6.4 percent.

Weaknesses

- The yield on the benchmark 10-year Treasury note hit 3 percent intraday for the first time in more than four years on Tuesday. The rally in yields has put bonds in negative territory this year.

- The March durable goods results were less encouraging than the upside surprise to headline orders would otherwise suggest, write Bloomberg Economics’ Carl Riccadonna and Niraj Shah. Boosted by a surge in aircraft orders, the sum of the remaining components fell short of expectations. Shipments were also lackluster in the month.

- Central banks may be losing their appetite for Treasuries just as supply is set to ramp up. The amount of U.S. government bills, notes and bonds held in custody at the Federal Reserve Bank of New York fell to $3.06 trillion as of April 25, down from a record high of $3.11 trillion reached in March, data show. The decline suggests that "some foreign official institutions may be reducing Treasury holdings in response to global trade tensions," Amherst Pierpont Securities global strategist Robert Sinche wrote in a note.

Opportunities

- The credit-worthiness of state and local governments in the U.S. has continued to improve amid an economic expansion that was boosted in the short term by tax cuts and increased spending, S&P Global Ratings said. The rating company said it sees economic growth accelerating in 2018, providing near-term fiscal relief for many state and local governments.

- U.S. consumers are getting more bullish on the housing market despite rising mortgage rates, tight supply and prices that are creeping higher. The share of Americans who plan to buy a home in the next six months rose to a record 7.8 percent, according to the Conference Board’s latest survey on consumer confidence.

- European Central Bank (ECB) policymakers see scope to wait until their July meeting to announce how they’ll end their bond-buying program, according to euro-area officials familiar with the matter. Governing Council members want sufficient time to judge if the economy is overcoming its first-quarter slowdown, officials said.

Threats

- The economic significance of currency fluctuations has been greatly underappreciated in the current economic cycle, in part due to the intense scrutiny on unconventional monetary-policy measures, such as quantitative easing. The resurgence of a strong dollar should not be ignored, as it could lead to a repricing of financial markets, reduce the pace of GDP growth and inflame the Trump administration’s focus on trade imbalances.

- The biggest threats to global economic growth are government debt and protectionist leanings, European Union (EU) economy commissioner Pierre Moscovici said, underlining the challenges confronting finance chiefs at the International Monetary Fund (IMF) meetings.

- While most states exercised fiscal restraint, Illinois, the lowest rated U.S. state, bucked the trend last year by increasing its debt 16 percent, Moody’s said. That wasn’t because it was investing in infrastructure, though. Illinois sold $6 billion in bonds to pay off a backlog of bills left from a long-running standoff over the budget. Additionally, Illinois accrued about $1.14 billion in late-payment interest fees over the past two and half years for bills not paid on time, more than the sum of such penalties during the previous 18 years combined, according to a report from Comptroller Susana Mendoza.

Gold Market

This week spot gold closed at $1,323.35, down $12.25 per ounce, or 0.92 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week slightly lower by 0.42 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index rose 2.63 percent. The U.S. Trade-Weighted Dollar pushed higher this week and rose 1.32 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Apr-24 | New Home Sales | 630k | 694k | 667k |

| Apr-24 | Conf. Board Consumer Confidence | 126.0 | 128.7 | 127.0 |

| Apr-26 | Hong Kong Exports YoY | 3.1% | 8.0% | 1.7% |

| Apr-26 | ECB Main Refinancing Rate | 0.0% | 0.0% | 0.0% |

| Apr-26 | Initial Jobless Claims | 230k | 209k | 233k |

| Apr-26 | Durable Goods Orders | 1.6% | 2.6% | 3.5% |

| Apr-27 | GDP Annualized QoQ | 2.0% | 2.3% | 2.9% |

| Apr-30 | Germany CPI YoY | 1.5% | -- | 1.6% |

| May-1 | ISM Manufacturing | 58.5 | -- | 59.3 |

| May-1 | Caixin China PMI Mfg | 50.9 | -- | 51.0 |

| May-2 | ADP Employment Change | 193k | -- | 241k |

| May-2 | FOMC Rate Decision (Upper Bound) | 1.75% | -- | 1.75% |

| May-3 | Eurozone CPI core YoY | 0.9% | -- | 1.0% |

| May-3 | Initial Jobless Claims | 224k | -- | 209k |

| May-3 | Durable Goods Orders | -- | -- | 2.6% |

| May-4 | Change in Nonfarm Payrolls | 195k | -- | 103k |

Strengths

- The best performing metal this week was gold, down 0.92 percent. This week was fairly negative for gold as the dollar held strong and the 10-year Treasury yield reached its highest since 2014 to 3 percent. A new use of blockchain technology will allow jewelers to track diamonds and gold from where they were mined to where they will be sold in retail. Four gold and diamond companies—Helzberg, Richline, LeachGarner and Asahi—will use the TrustChainInitiative, running on IBM’s technology, to prove to consumers that their purchases don’t include blood diamonds or other conflict metals, writes Bloomberg.

- We often get data points on U.K., Swiss or China/Hong Kong gold shipments, but one report on U.S. exports of gold caught our eye this week. U.S. exports of gold jumped 40 percent in February to 50.4 metric ton, roughly 25 percent of U.S. annual production that’s exported out in one month, with the largest percentage going to Hong Kong. China also imported 59.6 metric tons from Hong Kong in the same month. Gold is certainly moving from West to East.

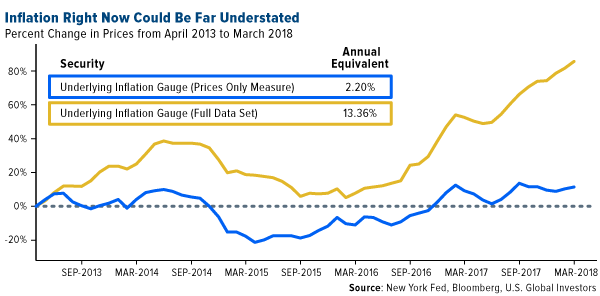

- With inflation talk starting to get more serious, we wanted to remind investors about the Underlying Inflation Gauge (UIG), which the New York Federal Reserve released last year. It has two parts to it: 1) a price-only index that has only been compounding at 2.20 percent for the last five years, and 2) a series that incorporates other non-price data, such as change in inventories. The research paper documenting all the variables is available on the New York Fed’s website. What is not talked about by the media is the UIG Full Data Set measure of inflation, which has been compounded at 13.36 percent over the last five years and really has been lifting strongly since 2016, the first year that gold had a positive return since 2012.

Weaknesses

- The worst performing metal this week was palladium, down 5.58 percent. Gold traders were bearish this week for the first time in four weeks, according to the weekly Bloomberg survey. Gold also broke its 13-day streak of inflows into ETFs; however, total gold held by ETFs rose 4.3 percent this year to 75 million ounces. Two-year Treasury yields are now at their highest in almost a decade, touching 2.5 percent this week. Mark Heppenstall of Penn Mutual Asset Management says that “in a rising-yield environment, it’s going to be hard to see out-sized gains for gold.”

- Palladium fell more than 5 percent on Monday to a session low of $971.72 an ounce, amid the U.S. hinting it might relieve sanctions on Russia, reports Reuters.

- Freeport-McMoRan, a Phoenix-based mining company, was blindsided this week by “shocking and disappointing” environmental claims from the Indonesian government, reports Bloomberg. The company announced that it would not be possible to continue mining at its flagship copper and gold mine in Indonesia unless it adopts new environmental standards imposed by the nation.

Opportunities

- Suki Cooper, analyst at Standard Chartered Plc, told Bloomberg in an interview this week that “investors are starting to look at gold again as a perceived inflation hedge.” Cooper estimates that the gold price may average $1,375 by year-end. Jeffrey Gundlach is also bullish on the gold price, saying this week that gold has broken its downtrend and is on the verge of breaking out to the upside. CPM Group is bullish on silver and said this week in its Silver Yearbook 2018 that “the enormous range of economic, financial and political issues facing the world and individual investors seems more likely to lead to a rekindling of silver demand from investors.”

- Although China’s gold output declined 6 percent year-over-year in 2017 and dropped 5.4 percent in the first quarter of 2018, it still kept its spot at number one in the world for production. China is also the world’s largest consumer of gold at around 1,089 tons last year, up by 4.1 percent. It’s important for investors to remember that China was a small player in the gold industry just 20 years ago and has gone through significant transformation due to a careful and deliberate strategy to expand the ownership of gold.

- Bloomberg Intelligence’s Mike McGlone writes this week that metals are in a bull market transition with stocks. McGlone also says metals are positioned to outperform the stock market and that increasing volatility is dragging on equities. He says current conditions mirror the decade-long metals bull run over two decades ago.

Threats

- HSBC has changed its forecast to include a strong U.S. dollar due to a shift in the relative dominance of cyclical drivers over structural and political drivers. Bloomberg also writes that the dollar is strengthening and could potentially have negative side effects such as repricing financial markets. This could reduce the pace of GDP growth and inflame the Trump administration’s focus on trade imbalances. A stronger dollar has historically been negative for the price of gold.

- Americans are growing pessimistic of the market, and for the first time since President Trump took office, a majority of consumers expect stocks to be lower in a year from now, according to the latest sentiment reading from the Conference Board. This is in stark contrast to a few months earlier in January when optimism was at a record high in the Conference Board survey. Apple’s costliest smartphone, the iPhone X, has struggled to attract new customers, and its manufacturing partners are feeling the downturn. Bloomberg writes that “Apple Inc.’s largest device assemblers reported a sharp slowdown after peaking at the end of last year, suggesting that demand for the high-end device may have faded just a quarter after its release.” For some of our readers who lived through the dotcom bubble, you might remember that forecasts of falling handset sales back in the year 2000 preceded the market downturn.

- U.S. debt continues to grow as Treasury officials are set to announce second-quarter funding plans on May 2 with bond dealers expecting another across-the-board boost to auction sizes, reports Bloomberg. According to JPMorgan’s estimate, government debt sales will more than double this year to a net $1.44 trillion. Andrew Lapthorne of Societe Generale SA says that interest rates have already been doing damage to the economy and that “leverage in the U.S. is grotesque for this stage of the cycle.” Lapthrone continued to say in an interview this week that “it’s not like you have to dig deep to find a problem.”

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended April 27 was Daneel, which gained 769 percent. This week during an interview, Adena Friedman CEO of Nasdaq, said that “Nasdaq would consider becoming a crypto exchange over time.” Although it is unlikely to launch a service anytime in the near future, this is very positive news for the cryptocurrency market in gaining widespread adoption, writes Coindesk. “I believe that digital currencies will continue to persist, it’s just a matter of how long it will take for that space to mature,” Friedman added.

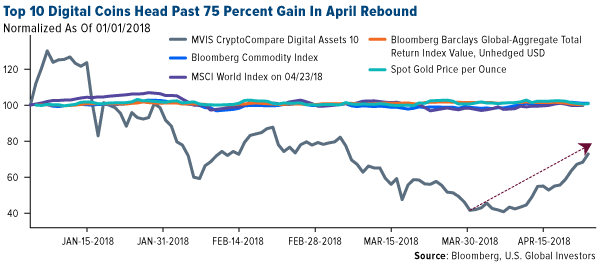

- Some of the world’s biggest cryptocurrencies rose again this week, reports Bloomberg. This extends their April rally deep into its fourth week, taking this month’s increase past 75 percent. According to Marc Ostwald, global strategist at ADM Investor Services in London, “The noise from regulators has been far less destructive in recent weeks than since the end of last year, and we haven’t had a big theft from an exchange recently.”

- Walmart Inc. is getting suppliers to put food on the blockchain, according to Frank Yiannas, vice president of food safety and health. As Bloomberg reports, the move would help reduce waste, better manage contamination cases and improve transparency. Another new use for blockchain technology is tracking jewels. From mines all the way to retail stores, four gold and diamond companies – Helzberg, Richline, LeachGarner and Asahi – are developing a network to do just that. These companies will use the TrustChainInitiative, running on IBM’s technology, to prove to consumers that their purchases don’t include blood diamonds or other conflict metals, writes Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended April 27 was Global Cryptocurrency, which lost 41 percent.

- Bloomberg reports that some ERC20 tokens, which are based on the Ethereum network, could be susceptible to a bug in the system. These tokens encompass about 90 percent of the $53 billion token market, according to CoinMarketCap. On Wednesday, two exchanges suspended the ERC20 token, with one going back up the same day.

- Central bankers still don’t seem to agree on cryptocurrencies and how to regulate them, but they do agree that tokens such as bitcoin and Ethereum won’t replace traditional currencies. The IMF wrote in a report this month that, “while they may serve as a store of value, their use as a medium of exchange has been limited and their elevated volatility has prevented them from becoming a reliable unit of account.” Different approaches around the world to regulating cryptocurrencies would mean that the effectiveness of regulation is limited, writes Bloomberg.

Opportunities

- A litecoin trade is turning heads in the cryptocurrency community, writes Business Insider. In a single trade at the end of last week, $99 million-worth of litecoin was sent between two crypto wallets in a single trade. The trade cost only $0.40 and took around 2.5 minutes to complete. Users are pointing out that a similar transaction in traditional finance “would take days to clear, multiple parties to sign off and carry heft fees,” the article continues.

- The Federal Reserve Bank of St Louis has conducted a new study breaking down cryptocurrencies and asking some of the biggest questions in the space today, reports CCN.com. The study includes an analysis of the control structure of various currencies and also looks into whether or not central banks will adopt cryptocurrencies as a form of payment. As the article points out, the study shows the bank as stating “we welcome anonymous cryptocurrencies, but also disagree with the view that the government should provide one.”

- Venrock Associates, a venture capital firm that grew out from the Rockefeller fortune, is setting its sights on investing in cryptocurrencies, specifically blockchain startups. Bloomberg reports that it is looking to invest some in tokens, but mostly in startups before issuing its own cryptocurrencies. David Pakman, a partner at Venrock Associates said that he thinks “this is one of the most transformative tech ecosystems and has the possibility of creating hundreds of companies worth billions of dollars each.”

Threats

- According to the Mosaic Network, cryptocurrencies’ “number-one problem” is the massive void in reliable research. Of course, there are books, blogs and critical media coverage on the space, but there still remains very little in the way of timely and rigorous 1) fundamental analysis of project teams and track records, 2) quantitative analysis of adoption and community traction, and 3) technical road-map risk assessment, to name a few, the article continues.

- Many large brokerage firms, such as Merrill Lynch and Wells Fargo, are banning their financial advisors from recommending cryptocurrencies. However, Jack Tatar, who is the co-author of “Cryptoassets” and was a Merrill Lynch financial advisor for almost 10 years, says “these firms will back-track their policies” eventually. Furthermore, Forbes writes that even though brokers can’t trade cryptos for their clients, they’ll go against their employers’ policies and advise their clients to make a personal investment.

- According to Coindesk, Capital Group, a financial services company with $1.7 trillion in assets under management has prohibited its associates from investing in initial coin offerings (ICOs) or initial public offerings (IPOs). The code of ethics says that there may be some exceptions to investing in IPOs, with no exceptions for ICOs. The ban could be positive with implications that the firm might invest in ICOs on behalf of their clients sometime in the future.

Energy and Natural Resources Market

Strengths

- Lumber was the best performing major commodity this week, rising 4.1 percent. The commodity rallied to a new record as a shortage of rail capacity in Canada’s west coast led to a pile-up of inventories sitting at sawmills and pulp mills, limiting deliveries to U.S. clients.

- The best performing sector this week was oil and gas equipment and services. The group rose 1.4 percent after a number of stocks in the sector were upgraded by analysts at Raymond James and Piper Jeffrey arguing increased visibility into a tightening market for well servicing and offshore rig maintenance.

- The best performing stock for the week was Rosneft Oil. Russia’s largest oil producer rose 11.5 percent after reporting earnings. The stock benefited as European leaders called on President Trump to ease off on imposing further sanctions on Russia.

Weaknesses

- Silver was the worst performing commodity this week. The commodity dropped 4.1 percent, posting its worst weekly decline since the summer of 2017. The commodity dropped as the U.S. dollar gained lost ground as a result of the 10-year government bond yield hitting 3 percent for the first time since 2014.

- The worst performing sector this week was diversified metals and miners. The group dropped 6.6 percent, tracking large weekly declines in base and industrial metals.

- The worst performing stock for the week was Freeport-McMoRan. The Phoenix-based miner dropped 20.1 percent after it warned new environmental rules and regulations imposed by Indonesian authorities may lead to a production drop at its flagship Grasberg mine.

Opportunities

- U.S. manufacturing business conditions rebounded in April, with the flash, or preliminary, purchasing manager’s index (PMI) rising to 56.5. Notable growth in output and new orders stimulated the headline PMI, with new orders rising at the most rapid pace in more than three-and-a-half years.

- China is considering proposals to cut import duties on passenger cars by about half, a move that reiterates the Asian nation’s commitment to advance trade liberalization with the rest of the world. The State Council is weighing proposals to reduce the levy on imported cars to 10 percent or 15 percent from the current rate of 25 percent.

- The integrated oil majors reported earnings this week showing increased profits, driven by higher oil prices, increased production and lower costs. The results “reflected improving profitability in the upstream exploration and production business, offset by less favorable refining market conditions and lower contributions from commodity trading,” according to the Financial Times.

Threats

- Oil futures signal a flood of U.S. exports is coming this summer. Once the world’s largest importer of crude, the U.S. now is closing in on Russia to become the world’s largest producer. America exported 2.33 million barrels a day of oil last week, the highest on record going back 25 years. As a result of strong Permian production, analysts expect West Texas Intermediate (WTI) crude to continue trading at a discount to other global benchmarks.

- The United Kingdom economy almost stalled in the first quarter of 2018, growing by just 0.1 percent, the Office for National Statistics (ONS) reported on Friday. It was also the weakest quarterly growth rate since 2012. The U.K. was hit by severe bad weather in February and March, but the ONS said that snow disruption could not explain all the fall in growth.

- Oil prices corrected lower on Wednesday in response to an unexpected build in U.S. crude oil stockpiles during last week. Data from the Department of Energy showed U.S. crude oil supplies unexpectedly increased 2.17 million barrels in the week versus an expected drop of 1.6 million barrels, thus posting one of the largest negative reconciliations in recent months.

China Region

Strengths

- South Korea’s GDP rose 2.8 percent year-over-year, just about in line with estimates. The economy expanded 1.1 percent in the first quarter, much better than the prior quarter’s 0.2 percent contraction.

- Year-over-year exports from Hong Kong were up 8 percent in the March measurement period, up from 1.7 percent for the February period.

- Singapore’s Industrial Production clocked in at a better-than-expected 5.9 percent for March, down from the prior month but still ahead of expectations. Month-over-month growth also beat, coming in higher by 0.3 percent.

Weaknesses

- The preliminary year-over-year Taiwan GDP reading for the first quarter came in below expectations at 3.04 percent, shy of the anticipated reading of 3.20 percent and below the prior quarter’s 3.28 percent.

- Industrial Profits in China came in lower than last month’s reading, at a 3.1 percent growth rate as opposed to last month’s 10.8 percent year-over-year showing.

- It was an ugly week for Indonesia’s Jakarta Composite—which tumbled by 6.53 percent over the last five trading days. Vietnam’s Ho Chi Minh Stock Index didn’t make out much better, continuing its recent woes and falling by 6.19 percent.

Opportunities

- Soon North and South Korea will no longer be officially at war! The Koreas held an historic summit on Friday in which the reclusive North Korean dictator walked across the border into the DMZ and attended a highly-publicized summit with South Korean President Moon. After many chummy photos and a few relatively minor announcements, the leaders announced a commitment to “denuclearization.” There is some debate as to precisely what that means. As expected, most press seems quite positive—the meeting is clearly notable and obviously any progress toward peace is most welcome—but there remain lingering questions about Kim’s intentions and the ultimate fate of North Korea’s nuclear program. The stage is now set, though, for the next major (and as of yet partially) scheduled event in the North Korean leader’s increasingly busy social schedule: a meeting with U.S. President Donald J. Trump, slated for late May or sometime in June. Leonid Bershidsky wrote shrewdly in a Bloomberg View column today of Mr. Kim and Mr. Trump that, “If they manage to achieve peace in Korea, they’ll be genuine heroes, whatever else they are.” He also noted that “Coral, one of the top British bookmakers, has Donald Trump and Kim Jong Un as favorites—at 2 to 1 odds—to win the Nobel Peace Prize this year.” Do take note.

- Chinese tourists abroad spend more than twice as much as Americans, according to a recent Bloomberg article that cited data from the UN World Tourism Organization. The theme of the expanding Chinese middle class—and growing purchasing power—continues.

- Malaysia’s Prime Minister Najib Razak announced this week a plan to alter the taxation scheme of the energy-exporting nation, aiming to cut corporate and personal income taxes and “shift toward consumption-based levies,” according to a Bloomberg report. The timetable for the changes will depend upon oil prices and GST income, the article observes.

Threats

- The upcoming U.S.-China trade discussions will loom particularly large in investors’ minds for the next several days as senior Trump administration officials—including Secretary of the Treasury Steven Mnuchin, Director of National Economic Council Larry Kudlow and U.S. Trade Representative Robert Lighthizer—travel to China to discuss trade, tariffs and intellectual property concerns.

- Related to the above is the announcement this week of an investigation into Chinese company Huawei Technologies over the possibility of Iran sanctions violations. The latest announcement comes on the heels of last week’s banning of ZTE—a major Chinese network equipment producer—from the purchase of U.S.-made components for similar sanctions violations. These moves could complicate upcoming trade discussions in China. Then again, perhaps it simply strengthens the U.S.’s hand as it comes to the table to talk. Time will tell.

- Continued volatility remains a threat if it generates an increase in selling.

Emerging Europe

Strengths

- Russia was the best performing country this week, gaining 3.1 percent. In absence of new sanctions, Russian equites are bouncing back from a sharp sell off after U.S. administration imposed new sanctions on the country. Brent crude oil continues its uptrend, supporting the Russian economy.

- The Turkish lira was the best performing currency this week, gaining 84 basis points against the U.S. dollar. The Central Bank of Turkey hiked its late liquidity-landing rate by 75 basis points to 13.25 percent, above market expectations of 50 basis points.

- Energy was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst performing country this week, losing 3 percent. Last week, the government announced that presidential and parliamentary elections will be held in June. After the elections, political uncertainty may decline and Turkey will shift to an executive presidency, a move approved in a constitutional referendum last year.

- The Polish zloty was the worst performing currency this week, losing 2.1 percent against the U.S. dollar. Retail sales came in strong; however, industrial orders plunged 24.3 percent in March from a year earlier, suggesting a slowdown in growth. Bloomberg’s survey predicts that the key rate in Poland will stay at a record low for at least another 18 months. Economists previously expected a first increase in the second quarter of next year.

- Industrials was the worst performing sector among eastern European markets this week.

Opportunities

- A slowdown in the pace of business activity in the eurozone came to a stop in April. After two straight monthly declines, the Markit Composite PMI stalled at 55.2 in April from March, above economists’ forecast of 54.8. Manufacturing PMI came in weaker, offset by a stronger reading in the Services PMI. The European Central Bank (ECB) left its policy rates unchanged and intends to continue its $30 billion monthly bond buying program until September, “or beyond if necessary.”

- Vladimir Putin is planning a roughly 10 trillion ruble ($162 billion) increase in spending on health care, education and infrastructure in the next six years in order to revive the economy and raise living standards. This plan has been in the works for several months, and should be finalized shortly after Putin’s inauguration on May 7.

- According to Capital Economics, while GDP in Central Europe has peaked, it remained strong at 4.5 to 5 percent year-over-year in the first quarter of 2018. Romania’s growth is slowing down, but the country is expected to publish its first-quarter GDP around 6 percent. Poland, the Czech Republic and Hungary continue to grow at close to 5 percent. Russia’s GDP most likely peaked around 1.8 percent in the first quarter from 0.9 percent in the fourth quarter of last year. Turkey’s latest economic data points show growth of 7.5 percent in the first quarter, in line with the fourth quarter.

Threats

- Global investors are likely hearing chatter about a flattening U.S. yield curve, which is a problem not only for the Federal Reserve but for the ECB too. Last week, the gap between the two-year and 10-year U.S. Treasury yield reached its narrowest since 2007, below 0.5 percentage point. The flattening U.S. yield curve may turn into an inverted yield curve, (where short-term rates rise above long term rates), and has as strong record of being a leading indicator of a recession. An economic slowdown in the U.S. will make the ECB’s job to tighten its policy more difficult.

- Six months after elections in the Czech Republic, Andrej Babis is struggling to form a new government as a potential partner intensified demands for joining his coalition. The Social Democrats have set a series of new conditions for the talks, including removing the anti-Muslim SPD party’s officials from the leadership post in the parliament. However, the lack of new government since the elections took place last October, have had little effect on the local stock market. Italy is also trying to form a new government after elections were held at the beginning of March.

- Since U.S. administration imposed the latest set of sanctions on Russia, the ruble declined sharply against the U.S. dollar, and it is poised for the worst month since December 2015. This week, the 50-day moving average for the dollar-ruble pair crossed above its rising 200-day rate, signaling a so-called “death cross.” Uncertainty about future sanctions against Russia, geopolitical tensions in Syria, and the ongoing Robert Mueller case into Russia’s meddling with the U.S. elections, may put more pressure on the currency. Analysts from Morgan Stanley and UBS Wealth Management warned that a selloff in emerging markets could leave the ruble especially vulnerable.

© US Global Investors