Insights from ICON Advisers: May 2018

Domestic Equities

Over nine trading days, the S&P 1500 Index dropped a quick 10% from its high January 26, 2018. The initial fear driving investors to sell was potential inflation based on labor data. That concern has faded from the headlines but has been replaced by another issue; international trade and the potential for tit-for-tat tariffs (often referred to as a trade war). As a business man, President Trump may have found issuing pre-negotiation threats to be a productive tool, but investors are having difficulty dealing with that tactic when it comes to international trade. (It appears they believe him!) As a result the broad market has moved in an up-and-down sideways trading range since early February. Entering May with a market value/price (V/P) ratio of 1.09, we expect the market to break out and move higher over the next year.

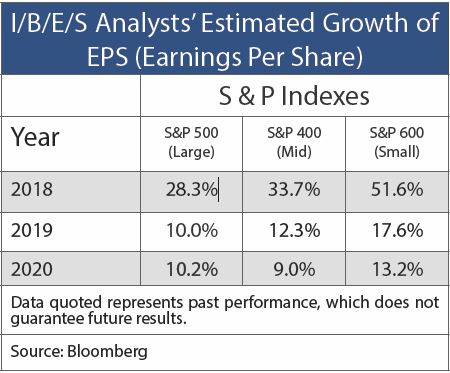

Earnings are the starting point for ICON to estimate the intrinsic value of a company. The first table shows forecasts for analysts who respond to the I/B/E/S survey. It is the year-over-year estimated rate of growth for earnings for companies in the S&P 500 (large-cap), S&P 400 (mid-cap), and S&P 600 (small-cap) Indexes. The new tax law is contributing to the surge predicted for 2018, but the outlook is favorable out into 2019 & 2020 as well. All else equal, if this growth materializes, our estimate of value will grow.

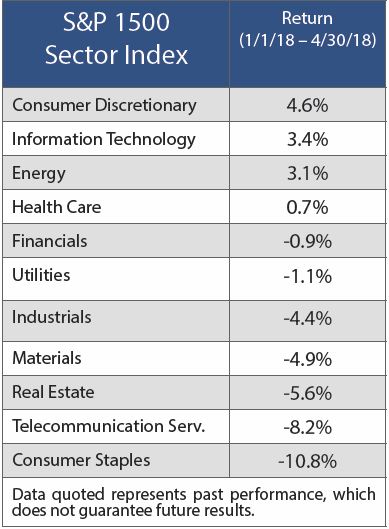

In the January Market Commentary we wrote, “Other conditions we contend accompany theme changes (volatility, for example) are absent, so we are inclined to believe the sector and industry theme of 2017 – a theme highlighted by large gains in the Financials, Information Technology, Health Care and Consumer Discretionary sectors – can continue into 2018.” The next table shows the S&P 1500 Sector Index returns for YTD 2018 (through April 30). The four we highlighted entering 2018 are all in the top five. “Volatility,” which was mentioned in January as being absent, is now up to levels often seen at sector and industry theme changes. It is too early to tell, but we may rotate in the coming weeks to try to capture the potential new theme that may emerge.

International Equities

Most international indexes resemble the domestic market the last few months, dropping sharply in early February and moving sideways since then. For years, we have labeled such synchronized behavior as driven by emotions rather than fundamentals. We believe that is the case this time. With an international V/P of 1.08, we expect international stocks to break out to the upside over the next year. We have done some rotating in our international exposure over the last six months. For emerging markets, in Asia, India has been reduced for valuation reasons while China is in the middle of the value rankings and, therefore, is a solid “hold.” Exposure has been increased to some emerging market countries in Eastern Europe.

Bonds

In the final months of 2017, the yield on the 10-Year Treasury was in the 2.30% to 2.40% range. It has increased in 2018, closing April at 2.954%, after spending just one day above 3.00%. We believe inflation expectations influence the yield on the 10-Year. Year-over-year increases in the CPI have increased from 0.1% in 2015 to 2.3% for 2018, so it appears the yield is just responding to modestly higher inflation. A survey of economists reported in Bloomberg calls for inflation to level off at 2.5% for 2018, 2.2% in 2019, and 2.3% in 2020. These forecasts seem reasonable to us, so we do not expect the yield on the 10-Year to rise sharply.

Summary

Many of the conditions often seen at buying opportunities are present. Investor sentiment is negative, volatility in stocks is above average, and our market V/P is 1.09. We expect the market to move higher over the next year. Value will guide us to determine if we make any sector rotations in the coming weeks.

The data quoted represents past performance, which is no guarantee of future results.

Opinions and forecasts regarding sectors, industries, companies, countries and/or themes, and portfolio composition and holdings, are all subject to change at any time, based on market and other conditions, and should not be construed as a recommendation of any specific security, industry, or sector.

Investing in securities involves inherent risks, including the risk that you can lose the value of your investment. An investment concentrated in sectors and industries may involve greater risk and volatility than a more diversified investment. Investments in international securities may entail unique risks, including political, market, regulatory and currency risks. In general, there is less governmental supervision of foreign stock exchanges and securities brokers and issuers. The risks of investing in international securities are greater for investments in emerging markets. Emerging market countries may experience greater social, economic, regulatory, and potential volatility and uncertainty than more developed countries. Investing in fixed income securities such as bonds involves interest rate risk. When interest rates rise, the value of fixed income securities generally decreases. High-yield bonds involve a greater risk of default and price volatility than U.S. Government and other higher-quality bonds.

ICON’s value-based investing model is an analytical, quantitative approach to investing that employs various factors, including projected earnings growth estimates and bond yields, in an effort to determine whether securities are over- or underpriced relative to ICON’s estimates of their intrinsic value. ICON’s value approach involves forward-looking statements and assumptions based on judgments and projections that are neither predictive nor guarantees of future results. Value readings are contingent on several variables including, without limitation, earnings, growth estimates, interest rates and overall market conditions. Although valuation readings serve as guidelines for our investment decisions, we retain the discretion to buy and sell securities that fall beyond these guidelines as needed. Value investing involves risks and uncertainties and does not guarantee better performance or lower costs than other investment methodologies.

ICON’s value-to-price ratio is a ratio of the intrinsic value, as calculated using ICON’s proprietary valuation methodology, of a broad range of domestic and international securities within ICON’s system as compared to the current market price of those securities. According to our methodology, a V/P reading of 1.00 indicates stocks are priced at intrinsic value. We believe stocks with a V/P reading below 1.00 are overvalued while stocks with a V/P reading above 1.00 are undervalued. For example, we interpret a V/P reading of 1.15 to mean that for every $1.00 of market value, there is $1.15 of intrinsic value which has not yet been realized in the market price.

The unmanaged Standard & Poor’s Composite 1500 (S&P 1500) Index is a broad-based capitalization-weighted index comprising 1,500 stocks of Large-cap, Mid-cap, and Small-cap U.S. companies.

The unmanaged Standard & Poor’s (S&P) 500 Index is a market value-weighted index of large-cap common stocks considered representative of the broad market.

The unmanaged Standard & Poor’s (S&P) MidCap 400 Index is a widely recognized unmanaged mid-cap index of 400 domestic stocks chosen for their market capitalization, liquidity, and industry group representations.

The unmanaged Standard & Poor’s (S&P) SmallCap 600 Index is an unmanaged index of 600 domestic stocks chosen for their market capitalization, liquidity, financial viability, and sector representation.

The unmanaged Standard & Poor’s (S&P) 1500 Sector Indexes track the performance of sectors that comprise the S&P 1500 Index. Total return for the unmanaged index include the reinvestment of dividends and capital gain distributions but do not reflect deductions for commissions, management fees, and expenses. The Portfolios’ composition may differ significantly from the indexes. Individuals cannot invest directly in an index.

I/B/E/S: Institutional Brokers’ Estimate System.

EPS: Earnings from ongoing operations; earnings per share equals total earnings divided by the number of shares outstanding.

The Consumer Price Index (CPI) is a measure of the average change in prices over time of goods and services purchased by households. The CPIs are based on prices of food, clothing, shelter, fuels, transportation fares, charges for doctors’ and dentists’ services, drugs, and other goods and services that people buy for day-to-day living.

The 10-year yield is the benchmark 10-year yield to maturity reflected by the current issue 10 year U.S. Treasury note.

Source: Bloomberg, FactSet

Please visit ICON online at InvestwithICON.com or call 1-800-828-4881 for the most recent copy of ICON’s Form ADV, Part 2.