Last week’s Barron’s cover story asked whether U.S. value stocks are primed to break out of their “funk” after 10 years of underperformance vs. growth stocks.

Included in the case for value is a standard definition of value investing: “At its most basic, it’s buying stocks that are cheap and holding them until the rest of the market realizes these great companies are selling at a bargain price, and pile in, driving prices up.”

Such an argument separates growth and value equities by stock price while overlooking a fundamental difference between the two. We base this on our perspective on international growth and value stocks.

Many of the “growth” companies that dominate growth indexes/portfolios and look more “expensive” are actually the winners of secular changes that have occurred while value indices/portfolios are littered with casualties of the change.

For us, growth vs. value—as they are often defined rigidly and simplistically in benchmarks—is not a binary choice. We prefer to think of growth and value in concert, as we invest in businesses with compelling growth fundamentals that support the ability to compound intrinsic value over time. This is fundamental to our approach to finding the best growth businesses and understanding the path to intrinsic value creation.

Technology Spending Skews P/E

Our team believes that conventional valuation metrics like P/E may not be appropriate in measuring value in an increasing number of instances.

The application of tremendous innovations in technology to a variety of industries is disruptive. There are companies that have and continue to invest heavily to build scale, in internet retail, media, financial services, advertising and cloud computing, among other areas.

This spending often isn’t accounted for properly as an investment (something we try to address with our economic profit-based approach) so it reduces current reported earnings and increases the P/E in some cases to levels well beyond the comfort zone of traditional value investors. But those investments are helping build scale and other competitive advantages that increase the longer-term cash generation capacity of the business—which results in growing intrinsic values.

Several leading platform technology companies are investing heavily to support growth initiatives, but we also see the pricing power they are exhibiting over recent quarters with minimal or no impact on user growth. These companies are taking price and, after you factor this into longer term cash flow projections, don’t look as expensive as a simple P/E may indicate.

Meanwhile, many of the low P/E stocks that screen well within a classic value universe are being “creatively destroyed,” and the current cash flows that make them look cheap are highly vulnerable over the longer term. (Creative destruction, as originally coined by Joseph Schumpeter, refers to the incessant product and process innovation mechanism by which new production units replace outdated ones.)

The Secular Vulnerability of Value Stocks

Differences in business models and industry opportunities have important implications on the investible universe within growth and value benchmarks. Such disruptive shifts may be most evident in the realm of the consumer in the economy, and in the consumer discretionary sector for investors.

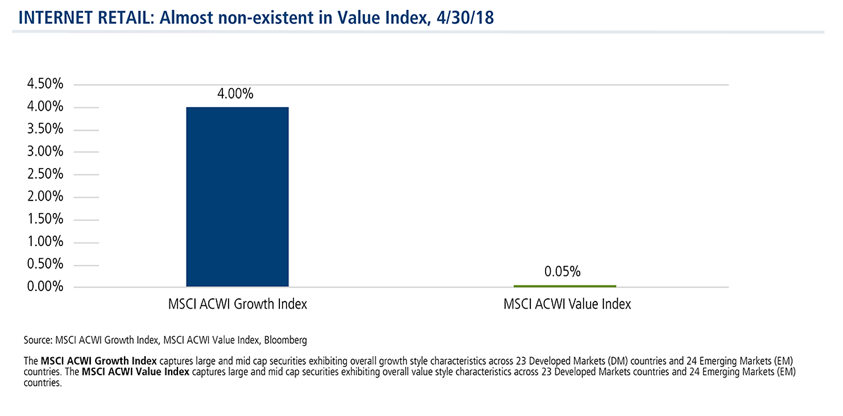

Internet retail, for example, is over 4% of the MSCI ACWI Growth Index vs. essentially non-existent in the Value Index, where consumer companies are mainly represented in traditional brick and mortar retail and automotive industries, for example.

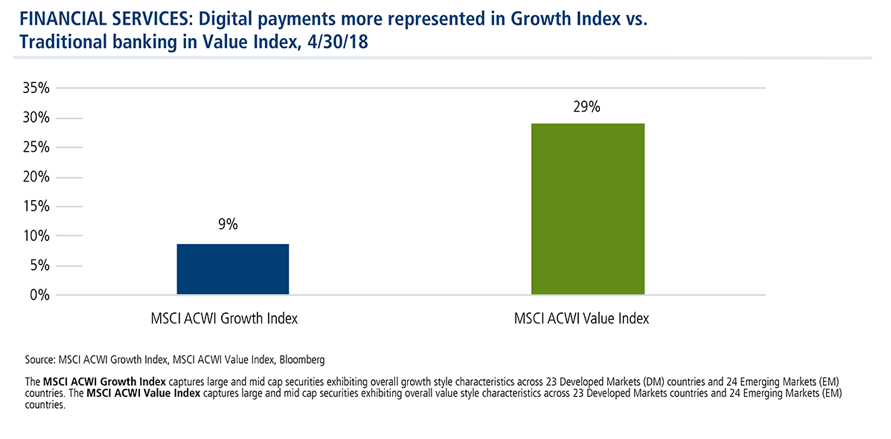

Financial services companies are also operating in a context of rapid change, with digital payments as a key frontier area. The Financials sector is 29% of the MSCI ACWI Value Index vs. 9% in Growth—with the Growth universe having significant exposure to digital payments in addition to disruptive technology companies with a leading foothold in mobile payments. The Value index, on the other hand, is heavily represented in traditional banking services.

Ultimately, we are interested in investing in sound businesses offering good growth prospects at reasonable valuations. While we recognize the role of simple, rules-based indexes to determine a set of growth and value companies, we highlight the dynamic that security prices and single-period valuation metrics may not always be an effective shorthand for the underlying business value over time.

This is a recurring example of the critical intersection of art and science in investing, of quantitative analysis and qualitative judgment.

--

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constiute our judgment and are subject to change without notice. The views and strategies described may not be suitable for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations. As a result of political or economic instability in foreign countries, there can be special risks associated with investing in foreign securities, including fluctuations in currency exchange rates, increased price volatility and difficulty obtaining information. In addition, emerging markets may present additional risk due to potential for greater economic and political instability in less developed countries.

©2018 Calamos Investments LLC. All Rights Reserved. Calamos®, Calamos Investments® and Investment strategies for your serious money® are registered trademarks of Calamos Investments LLC.

Calamos Investments LLC, referred to herein as Calamos Investments®, is a financial services company offering such services through its subsidiaries: Calamos Advisors LLC, Calamos Wealth Management LLC, Calamos Investments LLP and Calamos Financial Services LLC.

www.calamos.com

© Calamos Investments

Read more commentaries by Calamos Investments