The emergence of green bonds presents an attractive sustainable vehicle for fixed income investors, though not without drawbacks. The potential value of green bonds is obvious from the name; the securities prioritize the importance of environmental concerns as a means of either reducing risk or forming a competitive advantage when using the proceeds from the sale of the note. Green bonds also send the market a positive signal about their issuers’ intentions and priorities.

Although green bonds have begun to blossom as an asset class, with impressive growth since they first appeared in 2008, the size of the asset class is still that of a tiny sprout relative to the total bond market.1 Green bonds make up just 0.13% of fixed-income assets under management worldwide. This figure will likely grow, as institutional and retail investor demand for fixed-income investments that consider environmental, social, and governance (ESG) factors remains in the early stages. And that’s where confusion may lie ahead: green bonds have idiosyncrasies in their structures, ratings, geographic makeup, and ultimately, performance. Investors only broadly familiar with ESG investing need to account for these idiosyncrasies before allocating to this budding asset class.

How green are green bonds?

Since 2008 when green bonds were born from a limited public-private experiment, they have experienced a strong rate of growth. According to the Climate Bonds Initiative, in 2017 a record $155.5 billion of green bonds were issued, up from $87.2 billion the year before, representing 78% year-on-year growth.2 Unsurprisingly, as the rate and diversity of green bond issuance has grown, the characteristics of green bonds have come under greater scrutiny within the ESG community. Essentially the question comes down to, "How green is green?"

So far, this question has been difficult to answer with authority.

One reason is that green bond issuers aspire to meet voluntary standards and principles, but ultimately green bonds are not regulated or subject to a formal compliance process on their "green" status. Currently, the Green Bond Principles and the Climate Bonds Standards are the main international frameworks employed to label green bonds, but compliance is neither screened nor ensured by any one authoritative third party.

One example of how the ambiguity of green labeling has sown confusion is embodied by one of the green bond market’s most notable participants, China.

In the last two years, China ranked as the largest green bond issuer, dominating global issuance with $25 billion in 2017 and $33 billion in 2016.3 China's issuance equated to nearly 40% of the $81 billion of green bonds issued globally in 2016.4 China is expected to become an even more dominant issuer of green bonds as the People's Bank of China,China's central bank, says the country will need an estimated $320 billion a year to meet its government’s pollution reduction targets.5

China’s emergence as a dominant green bond issuer brings with it a tangible challenge. That’s because when it comes to green bonds, China has a playbook all its own. This includes issuing "green" bonds to support coal-fired power plants, a hard asset that is screened out under international guidelines adhered to by other green bond issuers.6 While China established its own regulations to "harmonize" its current guidelines with that of international practices, such a wide divergence on a key issue may be hard to reconcile any time soon.

Do green bonds perform?

Given that such a large issuer of green bonds fails to conform to international standards, it becomes imperative for investors to look before they leap. Ambiguous issuing guidelines are only one reason for doing so. Reviewing the performance thus far of green bonds reveals additional reasons to be cautious.

Green bond performance rests on the issuer satisfying two essential criteria: maintaining fiscal health and retaining "green proceeds" status. While these two criteria may seem straightforward, green bonds come from such a wide variety of global issuers that their solvency can come under question. An equally important dynamic is the risk of a green bond losing its status as a green issue, also known as "falling from green grace."

The lack of transparency in the green bond market makes credit quality and green status more difficult to assess, posing additional challenges in pricing the bonds with confidence. Green bonds, by their very nature, are more likely to fund innovative – but also sometimes experimental – projects; pricing risk accurately is more difficult due to a lack of apposite historical benchmarking data.

GREEN BONDS, BY THEIR VERY NATURE, ARE MORE LIKELY TO FUND INNOVATIVE – BUT ALSO SOMETIMES EXPERIMENTAL – PROJECTS; PRICING RISK ACCURATELY IS MORE DIFFICULT DUE TO A LACK OF APPOSITE HISTORICAL BENCHMARKING DATA.

Even more ambiguous is the green rating system for green bonds. As already noted, the green bond market relies on voluntary and nonbinding regulations to determine green-label eligibility. Issuers are reluctant to self-regulate their bonds, as they have little incentive to paint themselves into a legal corner if financial conditions change and they cannot meet their green obligations.

While the green status of a bond may at first seem superficial, the severity of the loss of green issue status can be meaningful, especially considering that research has shown green bonds can command higher prices relative to non-green bonds as a result of greater investor demand. A 2017 academic study 7 concluded that, on average, green bonds are more liquid relative to conventional bonds and trade at a premium in the secondary market. A similar academic study 8 found the effect of green bonds' higher liquidity on yield spreads to be pronounced, with green bonds commanding 10 times the premium of speculative German bonds and 100 times the premium of investment-grade US corporate bonds.

A LARGE PERCENTAGE OF GREEN BOND ISSUERS IN MANY INDUSTRIES FAIL TO RECEIVE ANY FORMAL RATING FROM AN AGENCY.

The risk a bond may lose its green-label status makes clear the potential pain for investors, and the ambiguities around the qualifications of green bonds all the more frustrating. Ambiguity might be forgivable if credit ratings could be accurately assessed. Unfortunately, a large percentage of green bond issuers in many industries fail to receive any formal rating from an agency. In the energy industry, US-domiciled firm Solar City offers an especially egregious example: Despite having issued 85% of all outstanding energy industry bonds and having nearly $3.7 billion in outstanding debt as of year-end 2016, 9 Solar City is not rated by any of the major credit rating agencies, such as Fitch, Moody’s, or S&P.

Foreign bond issuers play a large and growing role in the green bond market and bring their own risks. In March 2017, Moody’s downgraded China a notch from Aa3 to A1, reflecting concerns about slower growth, increased debt, and a weaker capacity to service its debt obligations. Adding to these concerns is the lack of an adequate bankruptcy process, which puts international creditors at risk.

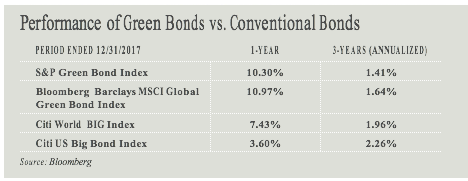

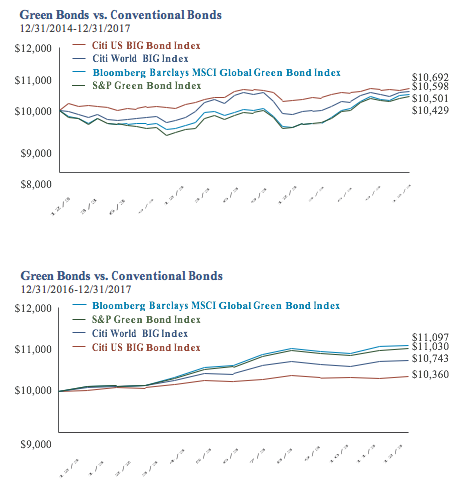

When it comes to the important question of performance, even greater attention is needed to find the budding flowers among the weeds. For example, when comparing green bond indices, such as those provided by S&P and Barclays MSCI, to their respective conventional counterparts, we find not only relative underperformance over a three-year period but also considerable variability with regard to fixed income benchmarks. The S&P Green Bond Index is "designed to track the global green bond market." For a bond to be included in the index, the bond issuer must explicitly disclose the use of proceeds; otherwise, its compliance with the Green Bond Principles must be independently verified.

How do we explain the disparity in returns among these indices, especially when numerous studies indicate compatibility between sustainable investing and competitive returns?

First, part of the answer has to do with index composition. Prior to 2015, most green bond issuers were primarily government-sponsored or supranational entities offering a lower yield consistent with their stellar credit ratings. In addition, many of these issues were non-US dollar denominated securities during a period of dollar strength.

Second, academic research points to green bond investors paying higher prices than conventional bond investors. Barclays research from 2015, for example, found that green bond returns have historically tracked conventional bond returns, though green bond prices trade with statistically tighter spreads, or lower price variance. The study’s authors note that if the spread divergence between green and conventional bonds continues, future green bond investors and sponsors will be forced to decide what price differential they will pay to be green.10

Additional academic research found that green bond investors accept a lower yield—by as much as 0.28%—to pursue socially responsible investments. The study examined the prices of 92 green bonds against 258 conventional bonds over the period from November 2013 to October 2016 and found a statistically and economically significant price premium associated with investment-grade green bonds versus investment-grade conventional bonds. 11

Lastly, an important distinction between green bonds and high ESG ratings is paramount. Issuing a green bond does not mean that the company scores well on ESG characteristics. Some green bond issuers have strong ESG characteristics and some don’t. Again, a green bond label simply identifies that a bond’s proceeds will be applied toward environment- related projects.

According to a study by Barclays Research titled "Sustainable Investing and Bond Returns" that analyzed data from independent ESG ranking and scoring organizations MSCI and Sustainalytics, companies with high governance scores can provide returns enhanced by as much as 5.5% relative to companies with low governance scores.12

The upshot is that bonds issued by companies with high ESG ratings exhibit measurable positive return characteristics, while similar return enhancements cannot yet be attributed to green bonds. Investors cannot simply "set and forget" an allocation to green bonds. While this segment of the fixed-income market is promising and growing, it does not yet have the maturity to be a properly investable asset class, particularly for nonprofessional investors. The return histories of both green bonds and the more robust ESG fixed-income universe suggest that most investors would be better off with the latter approach, at least until green bonds can establish sturdier roots.

COMPANIES WITH HIGH GOVERNANCE SCORES CAN PROVIDE RETURNS ENHANCED BY AS MUCH AS 5.5% RELATIVE TO COMPANIES WITH LOW GOVERNANCE SCORES.

While we stress the green bond market is still in its infancy and has its challenges, green bonds are making a significant contribution by aligning issuers with investors interested in addressing environmental risks.

Green bonds’ intrinsic value arises from their explicit consideration of environmental impact. Not only can green bonds help investors understand how companies are prioritizing their capital allocation and operational activities, they assign great importance to issuers’ consideration of externalities, such as the risk of environmental detriment. This is an enormous departure from past practices and is worthy of acknowledgment.

Footnotes

1 Cochu et al. Study on the potential of green bond finance for resource-efficient investments, European Commission, November 2016. http://ec.europa.eu/environment/enveco/pdf/potential-green-bond.pdf

2 Chestney, Nina. Global green bond issuance hit record $155.5 billion in 2017 – data, Reuters, January 10, 2018. https://www.reuters.com/article/greenbonds-issuance/global-green-bond-issuance-hit-record-155-5-billion-in-

2017-data-idUSL8N1P5335

3 Yen, Nee Lee. Trying to fight pollution, China is now the world’s largest issuer of ‘green’ bonds, CNBC, December 26,

2017. https://www.cnbc.com/2017/12/26/climate-change-china-is-the-worlds-biggest-green-bond-issuer.html

4 https://www.ft.com/content/84ac893a-028e-11e7-aa5b-6bb07f5c8e12?mhq5j=e2

5 Ibid.

6 Davidson, Ogunlade et al. New unabated coal is not compatible with keeping global warming below 2 ° C, Joint statement by leading climate and energy scientists, November 18, 2013. https://europeanclimate.org/documents/ nocoal2c.pdf

7 Wulandari, F. C., Schäfer, D., Stephan, A, & Sun, C.Liquidity risk and yield spreads of green bonds, Ratio Working Paper

No. 205, The Ratio Institute, December 21, 2017.d

8 Sun, C., & Wulandari, F. C. Liquidity Risk and Yield Spreads of Green Bonds: Evidence from International Green Bonds

Market, 2017. http://urn.kb.se/resolve?urn=urn:nbn:se:hj:diva-35819

9 Data obtained from Bloomberg

10 Preclaw, R and Bakshi, A. The Cost of Being Green, Barclays U.S. Credit Focus, September 18, 2015. https://www. environmental-finance.com/assets/files/US_Credit_Focus_The_Cost_of_Being_Green.pdf

11 Environmental value in corporate bond prices: Evidence from the green bond market, Aalto University School of

Business Department of Finance, https://www.google.com/search?source=hp&ei=qaMdWpOMI8SP0wKlj76YDQ&q

=Aalto+University+and+green+bond&oq=Aalto+University+and+green+bond&gs_l=psy-ab.3..33i160k1.615.4071

.0.4266.16.15.0.0.0.0.171.1257.11j3.14.0....0...1c.1.64.psy-ab..2.14.1256...0j0i22i30k1j33i22i29i30k1.0.ITi747VI6OU

12 Desclée, A, Hyman, J, Dynkin, L, and Polbennikov, S. Sustainable investing and bond returns, Barclays Research Department, Barclays Bank. https://www.investmentbank.barclays.com/content/dam/barclaysmicrosites/ibpublic/ documents/our-insights/esg/barclays-sustainable-investing-and-bondreturns-3.6mb.pdf

Important Disclaimers and Disclosures

This material is for general information only and is not a research report or commentary on any investment products offered by Saturna Capital. This material should not be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. To the extent that it includes references to securities, those references do not constitute a recommendation to buy, sell or hold such security, and the information may not be current. Accounts managed by Saturna Capital may or may not hold the securities discussed in this material.

We do not provide tax, accounting, or legal advice to our clients, and all investors are advised to consult with their tax, accounting, or legal advisers regarding any potential investment. Investors should not assume that investments in the securities and/or sectors described were or will be profitable. This document is prepared based on information Saturna Capital deems reliable; however, Saturna Capital does not warrant the accuracy or completeness of the information. Investors should consult with a financial adviser prior to making an investment decision. The views and information discussed in this commentary are at a specific point in time, are subject to change, and may not reflect the views of the firm as a whole.

The S&P Green Bond Index is designed to track the global green bond market and includes only bonds whose proceeds are used to finance environmentally friendly projects.

The Bloomberg Barclays MSCI Global Green Bond Index measures the global market for fixed income securities issued to fund projects with direct environmental benefits and includes only bonds that adhere to established Green Bond Principles.

The Citi WorldBIG Index is a multi-asset, multi-currency benchmark, which provides a broad-based measure of the global fixed income markets.

The Citi US Broad Investment-Grade Bond Index is a broad-based index of medium and long-term investment grade bond prices.

Investors cannot invest directly in the indices.

All material presented in this publication, unless specifically indicated otherwise, is under copyright to Saturna. No part of this publication may be altered in any way, copied, or distributed without the prior express written permission of Saturna.

Copyright 2018 Saturna Capital Corporation and/or its affiliates. All rights reserved.

1300 N. State Street Bellingham, WA 98225-4730 www.saturna.com

Read more commentaries by Saturna Capital