Defined maturity bond funds ETFs may provide a compelling option for a rising interest rate environment

Interest rates continue their upward trend. In March, the US Federal Reserve (Fed) hiked the federal funds rate by 25 basis points to a target range of 1.5% to 1.75%, citing strength in the US labor market, a low unemployment rate and moderate economic growth.1 This was the sixth such rate increase since December 2015, and isn’t likely to be the last. With inflation nearing the Fed’s annual 2% target, members of the Federal Open Market Committee (FOMC) — the Fed’s policy-making arm — anticipate at least two more 0.25% increases in the federal funds rate by year-end.2

What’s in store for the yield curve?

While higher short-term interest rates are likely in the near term, there is less agreement about the direction of long-term rates. Quite recently, the 10-year Treasury yield flirted with 3%. Going forward, I believe the prospects for higher long-term interest rates are still significantly greater than many forecasters would have you believe. Here’s my reasoning:

1. The tapering of quantitative easing in Europe. I expect the tapering of quantitative easing in Europe to reduce the demand for US Treasuries flowing from across the Atlantic. Reduced European demand for Treasuries could provide further room for Treasury bond prices to fall, which could support higher Treasury yields.

2. Rising currency hedging costs. While nominal Treasury yields are currently high enough to attract foreign investors, the high cost they’d pay to hedge against a falling US dollar could easily dissolve the yield advantage of US Treasuries, which could keep foreign investors on the sidelines.

3. Rising federal budget deficits. The federal budget deficit is expected to top $800 billion in 2018 and could balloon to $1 trillion by 2020, according to the nonpartisan Congressional Budget Office.3 Higher deficits mean more public borrowing, and a higher supply of US Treasuries can lead to lower Treasury prices — which can drive up interest rates.

4. Inflation. Although inflation gauges have yet to signal danger, rising commodity prices, recent fiscal stimulus and a strong US economy have raised market participants’ expectations of future inflation. If inflation does move beyond the Fed’s current annual 2% target, the Fed may continue raising short term interest rates, and US Treasury debt buyers may require higher longer-term interest rates to compensate for the accelerating decline in the US dollar’s purchasing power.

What’s a fixed income investor to do about rising interest rates?

There are a number of ways fixed income investors can position their portfolios for rising interest rates — including floating rate senior bank loans, which feature coupons that adjust upward as rates rise, and defined maturity exchange-traded funds (ETFs), which hold bonds until their final maturity dates. Keep in mind that as interest rates rise, bonds tend to lose value. That means most fixed income funds provide limited options for a rising rate environment. That’s where defined maturity ETFs come in.

The potential benefits of defined maturity ETFs

Traditional fixed income ETFs tend to provide a steady income stream, but don’t return principal to fund holders when the underlying bonds mature. Instead, traditional ETFs usually sell bonds well before their final maturity dates and reinvest those proceeds into other bonds. By contrast, defined maturity ETFs invest in a variety of bonds that all mature within a defined window of time. At the end of that window, proceeds are returned to investors. This may allow investors to time the distribution of any fund proceeds with future cash flow needs, such as college tuition, retirement or mortgage balloon payments.

If you expect rates to rise, you can target shorter-dated funds and simply reinvest the proceeds into longer-dated funds as rates increase. If you’re not sure about the direction of rates, you can invest in a laddered portfolio of funds that will provide you the opportunity to reinvest proceeds at regular intervals in the future.

The potential benefits of bond ladders

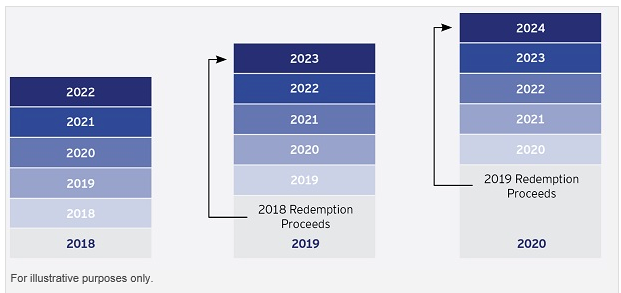

A ladder is a portfolio of bonds that mature at staggered intervals across a range of maturities. Assuming rates rise, proceeds from each maturing rung of defined maturity ETFs can be reinvested in longer-dated funds at higher rates. If market interest rates fall or remain flat, fund holders can stay invested and take the proceeds when the funds mature. By bond laddering with defined maturity ETFs, investors can generate regular income through a diversified range of maturities while maintaining the liquidity offered by the ETF structure. (Of course, diversification does not ensure a profit or protect against loss.)

Example of a laddered portfolio

Choosing a defined maturity ETF

Not all defined maturity ETFs are structured the same, of course. Some funds hold bonds that can be called in the event of falling interest rates. This shouldn’t be a problem for many investors, as there is a generally a premium associated with callable bonds, and callable bonds often feature higher yields than non-callable bonds.

Defined maturity ETFs also allow you to take advantage of the cost- and tax-efficient ETF structure4, while eliminating time-intensive bond credit research. Defined maturity ETF holdings are generally selected by a rules-based methodology and, depending on which defined maturity ETF you choose, you can access either investment grade or high yield credits.

Investors interested in defined maturity ETFs may wish to consider Invesco’s BulletShares suite of ETFs, which offers the choice of investment grade or high yield bond exposure.

1 Source: Board of Governors of the Federal Reserve System, March 21, 2018

2 Source: Board of Governors of the Federal Reserve System, FOMC projections materials, March 21, 2018

3 Source: Congressional Budget Office, The Budget and Economic Outlook: 2018 to 2028

4 Source: Since ordinary brokerage commissions apply for each buy and sell transaction, frequent trading activity may increase the cost of ETFs. Invesco does not offer tax advice. Please consult your tax adviser for information regarding your own personal tax situation.

Jason Bloom

Global Market Strategist

PowerShares by Invesco

Jason Bloom is the Global Market Strategist representing the PowerShares family of exchange-traded funds (ETFs). In this role, Mr. Bloom is responsible for providing the overall macro market outlook across all asset classes globally, in addition to leading the team’s specialized efforts in commodity, currency, and alternatives research and strategy. He joined Invesco PowerShares in 2015.

Prior to joining PowerShares, Mr. Bloom served as an ETF strategist with Guggenheim Investments for six years and then River Oak ETF Solutions where he helped launch several funds focused on both energy and volatility related strategies. Previously, he spent eight years as a professional commodities trader specializing in arbitrage strategies in both the energy and US Treasury markets.

Mr. Bloom earned a BA degree in economics from Gustavus Adolphus College and a JD from the University of Iowa College of Law.

Important information

A basis point is one hundredth of a percentage point.

The Congressional Budget Office is a federal agency within the legislative branch of the United States government that provides budget and economic information to Congress.

The federal funds rate is the rate at which banks lend balances to each other overnight.

Quantitative easing (QE) is a monetary policy used by central banks to stimulate the economy when standard monetary policy has become ineffective.

BulletShares funds do not seek any predetermined amount at maturity, and the amount an investor receives may be worth more or less than the original investment. In contrast, an individual bond matures; an investor typically receives the bond’s par or (face value).

There are risks involved with investing in ETFs, including possible loss of money. Shares are not actively managed and are subject to risks similar to those of stocks, including those regarding short selling and margin maintenance requirements. Ordinary brokerage commissions apply. The funds’ return may not match the return of the underlying index. The funds are subject to certain other risks. Please see the current prospectus for more information regarding the risk associated with an investment in the funds.

Investments focused in a particular sector are subject to greater risk, and are more greatly impacted by market volatility, than more diversified investments.

The funds are non-diversified and may experience greater volatility than a more diversified investment.

Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa.

During the final year of the funds’ operations, as the bonds mature and the portfolio transitions to cash and cash equivalents, the funds’ yield will generally tend to move toward the yield of cash and cash equivalents and thus may be lower than the yields of the bonds previously held by the funds and/or bonds in the market.

An issuer may be unable or unwilling to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

The values of junk bonds fluctuate more than those of high quality bonds and can decline significantly over short time periods.

Shares are not individually redeemable and owners of the Shares may acquire those Shares from the Fund and tender those Shares for redemption to the Fund in Creation Unit aggregations only, typically consisting of 10,000, 50,000, 75,000, 80,000, 100,000, 150,000 or 200,000 Shares.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2017 Invesco Ltd. All rights reserved.

Are you prepared for rising interest rates? by Invesco