Sector Performance and Economic Cycles: When Do Sectors Have the Potential to Shine?

Where we stand in the economic cycle can have a measurable effect on sector performance

There are many determinants of stock performance. Corporate earnings, fiscal policy and interest rates can all influence the equity markets. But equity returns are also dependent on where we stand in the economic cycle.

Some sectors, such as industrials and financials, tend to display strong performance early in the economic cycle when economic growth is accelerating. Other sectors, like utilities and consumer staples, tend to be strongest very late in the economic cycle when economic growth is weakest.

How do we know this?

The correlation between excess returns and economic cycles

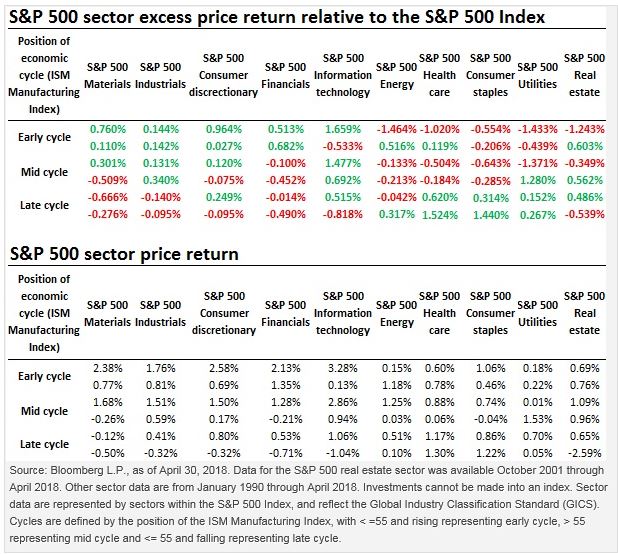

Consider the table below, which displays the excess price return of the 10 sectors that make up the S&P 500 Index over a roughly 17-year period, from October 2001 through April 2018. (Here, I am defining excess returns as the price of each sector minus the price of the S&P 500 Index.) I’ve segregated returns by economic cycle, defined by the position of the Institute of Supply Management Manufacturing Index (ISM Manufacturing Index), which is a broad barometer of manufacturing activity in the US.

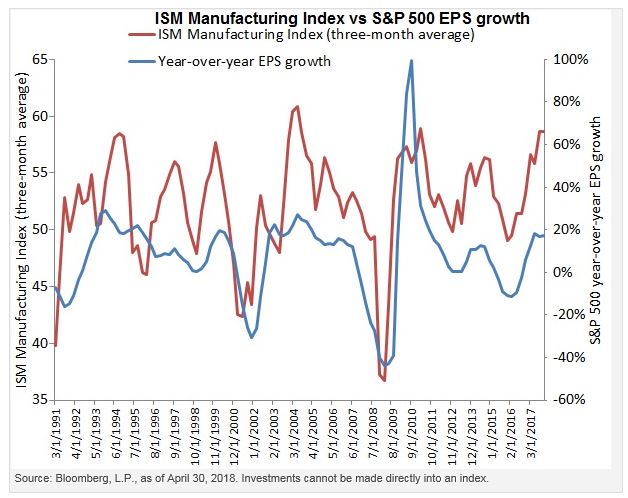

As you can see from the chart below, the ISM Manufacturing Index has historically tracked year-over-year changes in earnings per share (EPS) growth for the S&P 500 Index. In fact, the correlation between year-over-year EPS growth and the ISM Manufacturing Index over the 17-year period was a robust 0.60, indicating a strong correlation between economic cycles and corporate profit growth. This correlation can be useful in framing sector performance relative to economic cycles, represented by the swells and dips in the ISM Manufacturing Index.

Where are we in the current economic cycle?

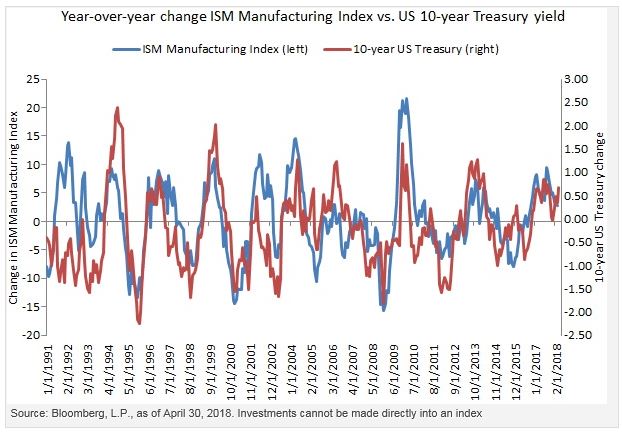

The ISM Manufacturing Index also displays a vibrant relationship to interest rates, further highlighting its ability to capture economic cycles. Historically, the one-year change in the 10-year US Treasury yield has coincided with the one-year change in the ISM Manufacturing Index, as evidenced by a 0.52 correlation. As of April, the ISM Manufacturing Index was 57.3 below its February 2018 peak of 60.8. In my view, this suggests that US economy is mid-cycle, but on its way to being late-cycle.

- Materials have tended to underperform when the ISM Manufacturing Index is falling from its cycle peak, and have tended to outperform when the index is increasing. The excess return of the materials sector now looks quite cyclical following the direction of the ISM Manufacturing Index.

- Utilities also display cyclicality, but their excess return moves opposite to the excess return of materials. Utilities have historically generated excess returns when the ISM Manufacturing Index was falling and have underperformed when the index was rising.

- Consumer staples stocks are cyclical as well, displaying past weakness during periods when the ISM Manufacturing Index was rising through the early phase of a decline in the index. However, this sector has historically outperformed later in the cycle when the ISM Manufacturing Index was below 55 and falling.

- Health care has historically performed somewhat like consumer staples — performing best very late in the cycle and poorly early in the cycle.

- Industrials have historically been weakest very late-cycle when the ISM Manufacturing Index was under 55 and falling, but have shown strength through the upward cycle of the index (under 50 and rising, 50 to 55 and rising, and over 55 and rising). Moreover, industrials have a history of generating excess return very early in the downside cycle (ISM Manufacturing Index over 55 and falling). Conversely, industrials have historically performed most poorly very late in the cycle when the index was under 55 and falling.

- Financials have historically shown the greatest strength early-cycle when the ISM Manufacturing Index was rising from under 50 through the 50-to-55 range. They were weakest very late-cycle when the index was falling. Fallout from the housing bubble and global financial crisis may have distorted some of the cyclical influences since 2008.

- The performance of information technology has historically been choppy throughout economic cycles. The potential for technology to provide innovation may have muted the influence of the economic cycle on performance. However, technology has historically shown to perform very poorly very late-cycle and most strongly very early-cycle.

- Energy stocks are likely more sensitive to the price of oil, oil products and natural gas than the economic cycle. Their past performance relative to the ISM Manufacturing Index seems mixed, which may simply be random, rather than indicative of a clear pattern.

- Real estate — particularly real estate investment trusts (REITs) — has historically displayed strength mid- to late-cycle (over 55 and falling, and 50 to 55 and falling), and relative weakness very late-cycle (under 50 and falling) and very early cycle (over 50 and rising). REITs can be tricky, as they are often influenced by both interest rates and rent patterns. Rents could be under pressure very late- and very early-cycle, and strong through periods of the middle cycle.

Investors looking for access to equity sectors may wish to explore the PowerShares Equal Weight ETFs or the PowerShares Dorsey Wright Equity ETFs.

Nick Kalivas

Senior Equity Product Strategist

Nick Kalivas is a Senior Equity Product Strategist representing the PowerShares family of exchange-traded funds (ETFs). In this role, Nick works on researching, developing product-specific strategies and creating thought leadership to position and promote the smart beta* equity line up.

Prior to joining Invesco PowerShares, Mr. Kalivas spent the majority of his career in the futures industry, delivering research, strategy and market intelligence to institutional and high net worth clients centered in the equity and interest rate markets. He was a featured contributor for the Chicago Mercantile Exchange, and provided research services to a New York-based global macro commodity trading advisor where he supplied insight on equities, fixed income, foreign exchange and commodities. Nick has been quoted in the Wall Street Journal, Financial Times, Reuters, New York Times and by the Associated Press, and has made numerous appearances on CNBC and Bloomberg.

Nick has a BBA in accounting and finance from the University of Wisconsin – Madison and an MBA from the University of Chicago Booth School of Business with concentrations in economics, finance, and statistics. He holds the Series 7 and Series 63 registrations.

Important information

Blog header image: PowerUp/Shutterstock.com

The Global Industry Classification Standard (GICS) was developed by and is the exclusive property and a service mark of MSCI Inc. and Standard & Poor’s.

The ISM Manufacturing Index, which is based on Institute of Supply Management surveys of more than 300 manufacturing firms, monitors employment, production inventories, new orders and supplier deliveries.

Correlation is the degree to which two investments have historically moved in relation to each other.

Earnings per share (EPS) refers to a company’s total earnings divided by the number of outstanding shares.

A real estate investment trust (REIT) is a closed-end investment company that owns income-producing real estate.

There are risks involved with investing in ETFs, including possible loss of money. Shares are not actively managed and are subject to risks similar to those of stocks, including those regarding short selling and margin maintenance requirements. Ordinary brokerage commissions apply. The funds’ return may not match the return of the underlying index. The funds are subject to certain other risks. Please see the current prospectus for more information regarding the risk associated with an investment in the funds.

Investments focused in a particular sector, such as industrials, such as materials, industrials, financial services, health care, information technology, energy, consumer staples and utilities are subject to greater risk, and are more greatly impacted by market volatility, than more diversified investments. Investments in real estate related instruments may be affected by economic, legal, or environmental factors that affect property values, rents or occupancies of real estate. Real estate companies, including REITs or similar structures, tend to be small and mid-cap companies and their shares may be more volatile and less liquid.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2017 Invesco Ltd. All rights reserved.

Sector performance and economic cycles: When do sectors have the potential to shine? by Invesco