One of the many ways this year differs from last is that in 2017 even your hedges rose–a surprise, since one expects that assets intended to hedge equity risk won’t perform well in “risk on” periods. However, in 2018, in contrast, not only are stocks producing lower returns with more volatility, hedges have become less reliable. U.S. government bonds are down anywhere between 2% and 4%, depending on the duration of the bond. Gold, another portfolio hedge, is flat year-to-date.

Last November, I suggested that investors trim, but not abandon gold. Since then global stocks are up around 3% in dollar terms; the U.S. has done even better, gaining roughly 5%. At the same time a broader index of U.S. bonds is off around 2.5% while gold is flat. In other words, gold has beaten bonds but been a drag on equity returns.

What is more troubling is a recent trend

Even during equity market sell-offs, gold has been a less reliable hedge. For example, during the May 29th sell-off on the back of turmoil in the Italian bond market stocks got pounded; gold was flat.

Why has gold recently proved a less effective hedge? As I noted last November, the change reflects two key, related developments: a stronger, tax-cut fueled U.S. economy and an accompanying bounce in the dollar. In particular, the stronger dollar has been a headwind for gold. While the dollar declined in December and January, its recent strength has removed one of the key props for the yellow metal.

Tailwinds for the dollar

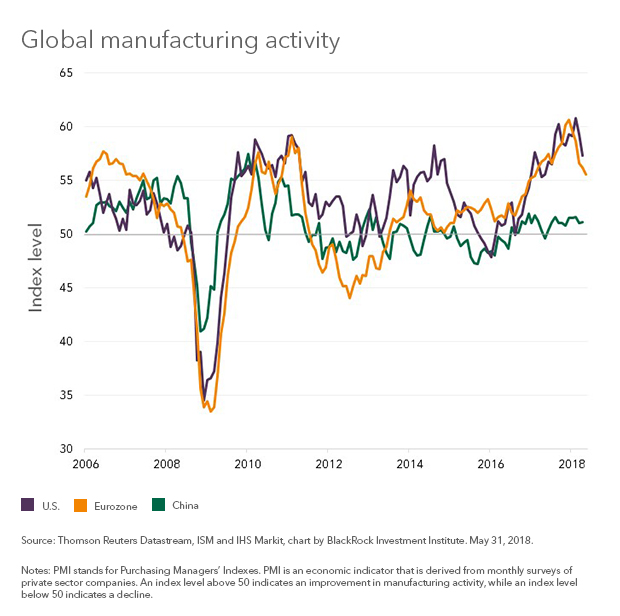

What to expect going forward? To my mind this is still mostly about the dollar. While the twin fiscal and current account deficits suggest a weaker dollar longer-term, fundamentals in the near-term may be more supportive. Although U.S. growth has moderated, Europe has decelerated at a much faster pace (see Chart 1). In fact, European economic surprise indexes, i.e. economic data versus expectations, are stuck at the lowest level since 2011.

Beyond slow growth, the other tailwind for the dollar is European political stability, or more precisely, the lack of any in Italy. On Tuesday, growing fears of a populist coalition in Italy pushed 10-year Italian bond yields over 3%, a four-year high. For the first time in years, investors are beginning to question the long-term sustainability of the euro. These fears are probably overblown, but there is no quick cure for the current instability in Italian politics. These concerns are likely to linger, at least through the next Italian election.