Imagine that your goal is to maximize the total return of your portfolio. You can either invest your portfolio 100% in stocks or split the portfolio equally between stocks and an uncorrelated strategy with an annual return that is 1% less than stocks.

Would you take the 50/50 mix or put it all in the stock market? Most investors would opt for the 100% stock portfolio, presuming it would outperform an option that includes a lower returning investment. In fact, the 50/50 portfolio is the correct choice.

This is an excellent example of the underappreciated fact that all returns are not created equal. A grossly undervalued characteristic of a return set is its correlation. This ARIS Insights explores the power of adding low correlation investments to a portfolio.

Two main points will be covered in this brief discussion:

- Inclusion of low correlation assets can improve returns more than many investors may realize.

- Today, the return hurdle for including low correlated assets is much lower than normal.

Low Correlation Can Lower Risk and Boost Returns

Most investors understand that adding low correlation returns to a portfolio will reduce portfolio risk. However, very few appreciate how much low correlation assets can improve the overall portfolio return. The return enhancement comes from the annual rebalancing from the outperforming investment to the underperforming one. Since the two uncorrelated assets produce comparable long-term returns through very different paths, the repeated buy-low and sell-high discipline accrues over time. We call this hidden benefit the “low correlation boost.” The lower the correlation the greater the boost potential because of the increased dispersion of returns between the two investments. This is a well-known and widely documented phenomenon1 that is commonly overlooked.

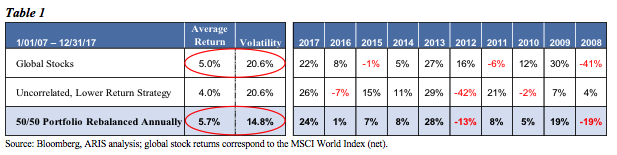

The math can be illustrated using a simple example as summarized in Table 1 below. The portfolio of 100% global stocks has averaged 5% per year during the past 10 years ending 12/31/17. The uncorrelated return strategy is created by randomly rearranging the 10 calendar year returns of global stocks and subtracting 1% each year, resulting in a return that averages 4% per year and is zero correlated to global stocks.2

The returns of the 50/50 portfolio are surprisingly high. It is instinctive to think that this mix should earn 4.5%, or the average of the two component return streams. However, there is an extra 1.2% annual return that accrues to the total portfolio from adding an uncorrelated asset, resulting in a 5.7% annual return – better performance than the 100% stock portfolio!3 The entire 1.2% boost in this example comes from annual rebalancing, as the portfolio is consistently rotated from the outperforming return to the underperforming one.4

Not only does adding the lower returning option yield superior performance, it also offers the additional benefit of lowering the risk due to the improved diversification that comes from owning two very different sets of returns. This shows up in both the lower volatility of the 50/50 portfolio (14.8% vs. 20.6%) and in the worst calendar year loss being much less severe (-19% vs. -41%).

The math is compelling: adding low correlation investments can both reduce risk and increase portfolio returns, even when the low correlation investment has a lower return than your existing portfolio.

Lower Return Hurdle Today

Most portfolios predominantly consist of traditional stock and bond allocations. During normal periods, these portfolios may have earned 6-8% on average per year (with stocks around 8-10% and bonds at 4-6%). However, these are not normal times. Cash has been yielding close to zero for almost a decade and many asset markets are near their most expensive levels in the past 100 years. As a result, many conventional markets are likely to produce low returns for the foreseeable future.

At the same time, risk may be greater than what we have experienced since 2009. Central banks are starting to tighten monetary policy, we are entering the late stages of the business cycle and governments have limited ability to respond to the next economic downturn. Meanwhile, high global debt levels and the rise of populism create the potential for extreme outcomes.

For these reasons, the return hurdle for adding low correlation strategies to a portfolio may be even lower than normal. That is, if we expect low returns out of traditional assets, then a high return should not be a prerequisite for adding return streams that are reliably different. Moreover, as we show in the example above, a relatively low uncorrelated return can actually increase portfolio returns through prudent rebalancing. Investors may be well served to focus at least as much on correlation as they do on the level of returns.

Putting Theory into Practice

Significant patience will always be required to successfully implement these ideas in practice. Investors will potentially face periods of underperformance from low correlation strategies when the rest of the portfolio may be performing well. For example, in 2012 in the table above, stocks are performing strongly while the uncorrelated investment is experiencing a massive loss. A natural response at that point in time is to question whether this investment (which is less familiar and likely more expensive) is worth having.

To help during these challenging environments, it is critical to use the appropriate reference point in assessing performance. Rather than anchor to the stock or bond markets, as is common practice, an investor must develop a set of expectations that are unique to each uncorrelated strategy, which can include exposures such as reinsurance, healthcare royalties or market neutral hedge funds. As all strategies will experience losing environments, it is crucial to understand whether the losses make sense relative to the expected return, risk, correlation, and environmental biases of the strategy. If so, the investor should instead be thinking about rebalancing from the outperformer to the uncorrelated strategy to take advantage of the low correlation boost described earlier.

In our experience, the most undervalued characteristic in investment management is correlation. Through careful identification/evaluation of low correlation strategies and disciplined incorporation of these returns into investment portfolios, investors can improve portfolio returns while reducing their susceptibility to extreme market outcomes.

Important Information

PAST PERFORMANCE IS NOT AN INDICATION OF FUTURE RESULTS

Advanced Research Investment Solutions, LLC (“ARIS”) is an SEC-registered investment adviser that provides investment advisory services and investment consulting services to a select set of clients and pooled investment vehicles. None of ARIS’s services are intended to represent a complete investment program.

This publication is for illustrative and informational purposes only and does not represent investment advice or a recommendation of or as an offer or solicitation with respect to the purchase or sale of any particular security, strategy or investment product. Past performance is not indicative of future results.

Different types of investments involve varying degrees of risk, including possible loss of the principal amount invested. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by ARIS), or any non-investment related content, will be profitable, equal any corresponding indicated historical performance level(s), be suitable for a client’s portfolio or individual situation, or prove successful. Nothing contained herein is intended to predict the performance of any investment. There can be no assurance that actual outcomes will match the assumptions or that actual returns will match any expected returns.

Nothing contained herein constitutes legal, tax or other advice nor is it to be relied upon in making an investment or other decision.

Certain information contained herein has been obtained or derived from unaffiliated third-party sources and, while ARIS believes this information to be reliable, neither ARIS nor any of its affiliates make any representation or warranty, express or implied, as to the accuracy, timeliness, sequence, adequacy or completeness of the information.

The information contained herein and the opinions expressed herein are those of ARIS as of the date of writing, are subject to change due to market conditions and without notice, and have not been approved or verified by the United States Securities and Exchange Commission (the “SEC”), the Financial Industry Regulatory Authority (“FINRA”), or by any state securities authority.

This publication is not intended for redistribution or public use without ARIS’s express written consent.

1 One example of a long-standing research article on the subject is Bernstein, William J. “The Rebalancing Bonus: Theory and Practice.” Efficient Frontier: An Online Journal of Practical Asset Allocation. September 1996. http://www.efficientfrontier.com/ef/996/rebal.htm.

2 We compared 500 different random combinations of the same calendar year returns and found that the “boost” is directly proportional to the correlation (the lower the correlation the greater the boost). The boost of 1.2% is similar for all combinations with roughly zero correlation.

3 Please note that this analysis assumes no tax consequences from rebalancing. For taxable investors, potential income taxes from selling appreciated securities would reduce the low correlation boost. Taxable investors may incorporate a less frequent rebalancing approach (which would still be highly beneficial) and/or use cash flows to rebalance the portfolio to minimize realized gains.

4 To provide some context, the 1.2% boost from adding an uncorrelated return that averages 4.0% is the equivalent of adding a perfectly correlated return that averages 6.4%. In other words, the return hurdle for the uncorrelated return to improve the performance of the total portfolio is much lower than that of a highly correlated strategy. Thus, investors should give material weight to correlation when assessing various investment options.

© ARIS

Read more commentaries by ARIS