Energy equities have underperformed the S&P 500 materially over the last five years. While spot oil prices have risen significantly over the last twelve months, longer dated oil prices have not, and energy equities have remained under pressure. The lower oil price environment has forced the companies to focus on improving profitability via cost control and capital restraint and we see this, in combination with rising longer dated oil prices, as positive catalysts for energy equities. We explore these arguments below.

It has been a good twelve months for spot oil prices. Why is the oil price at $70/bl?

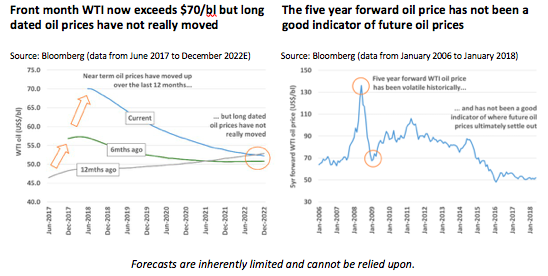

Since the start of May 2016, WTI has rallied from under $50/bl to $70/bl. The key drivers of a tighter oil market have been:

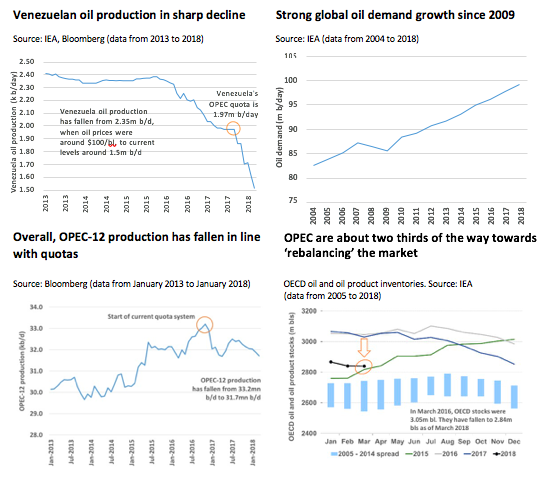

Strong global oil demand. Global oil demand is forecast to grow by 1.5m b/day in 2018, to a new high of 99.3m b/day, according to the IEA. A combination of good global GDP growth and inexpensive oil (relative to the first half of the decade) has resulted in demand forecasts in recent years consistently being revised higher. 2018 looks to be no exception to that. The growth this year is mainly expected to come from emerging countries. In the passenger vehicle market in China, for example, we have seen a surge in ownership of SUVs: five years ago they made up 15-20% of new sales, whereas today it is close to 45%. Air travel across the Asia-Pacific region is also surging, thanks to economic expansion, with air traffic up nearly 12% versus a year before. In the five years since 2013, global oil demand is expected to have grown by 7.6m b/day, the strongest period of demand growth since 2003-07.

OPEC supply discipline and political tensions. OPEC compliance with the 1.2m b/day quota cuts that were announced at the end of 2016 has been strong. In our estimation, they are about two thirds of the way on their journey to rebalancing the market. High compliance has been led by Saudi, and supported by a smaller cut from Russia, as both countries work to fix domestic fiscal issues. The tightening effect of OPEC’s planned supply cuts has been compounded by under-investment from OPEC’s poorer members, particularly Venezuela. Venezuelan production is currently estimated to be around 1.4m b/day, down by 0.6m b/day since the start of the year, as deteriorating infrastructure, weak reservoir management and poor relations with foreign partners have combined to lower supply. Most recently, the re-introduction of sanctions against Iran in relation to their nuclear program brings the prospect of a drop in Iranian oil exports later this year.

Controlled US shale oil supply growth. US shale oil is on the rise again, with year-on-year growth of around 1.2m b/day. However, improved capital discipline has filtered through to the US E&P community, with a significant number of larger producing companies favoring dividends or expanded share repurchase programs over unconstrained capital spending and growth. We are also seeing signs of greater oilfield service cost inflation than was generally expected, and the emergence of infrastructure challenges in the prolific Permian basin in Texas. Overall, while the strength in spot oil prices is causing some acceleration of activity, forecasts for US supply growth at any given oil price are no higher today than they were twelve months ago.

Non-OPEC (ex US) supply concerns. The largest slump in capex for over 20 years has caused a deterioration in the long term outlook for non-OPEC production outside the US. Existing fields have declined faster during the oil price fall and there is a shortfall of new projects coming online in this area, which represents over half of current world oil supply. Due to the long lead times involved in this sector of the industry, non-OPEC (ex US) supply is still being held up by projects that were sanctioned when the oil price was over $100/bl. There are increasing signs, however, that new international production into the end of the decade will tail off as the lack of investment bites.

An elevated spot oil price has not necessarily been bullish for equities

While spot oil prices have risen sharply on strong demand and OPEC-led supply constraint, longer dated oil prices have hardly moved (five year forward WTI is still around $52/bl). The downward sloping shape of the oil futures curve (i.e. in backwardation) reflects OPEC’s supply cuts being only short term in nature and the market’s apparent belief that global oil supply will be able to match demand at a price of around $50/bl in the longer term. This may be the current market view, but it is worth noting that longer dated oil prices are often volatile and have a low correlation to where prices eventually end up. In recent months, we believe that forward selling (hedging) of crude oil by US exploration & production companies has also exacerbated the scale of the backwardation. We expect the longer dated end of the forward curve to rise from here.

What is a reasonable level of long term oil price and what would it mean for the companies?

We believe that long run oil prices will return to a $60-70/bl range. This is a price which is sufficient for world oil demand and US shale oil to grow while also providing acceptable economics for OPEC countries and sufficient profitability for investment in new oil projects around the world. This would be a ‘reasonable’ oil price level for all constituents of the global oil market.

Today, assuming operating and capital costs are held constant, we calculate that our portfolio of energy equities currently offers fair value assuming a long term WTI oil price in the mid to low $50s (i.e. broadly in line with where long dated oil prices currently are). Looking out two years, while we see downside risk of about 10% if energy equities were to factor in $50/bl long-term, we see around 30% upside at a $60 WTI oil price and more like 60% upside at a $70/bl WTI oil price.

So, higher long dated oil prices is good for company valuations. Is that it?

Rising oil prices clearly help, but energy companies have also made significant efforts towards improving profitability via internal measures such as cost reductions and the sale of peripheral assets. It is still quite early in the year but given the improved cost and capital discipline delivered so far, the companies in the Guinness Atkinson portfolio are likely to produce better free cashflows at $55/bl WTI oil in 2018 than they did at $100/bl oil in 2011-2014.

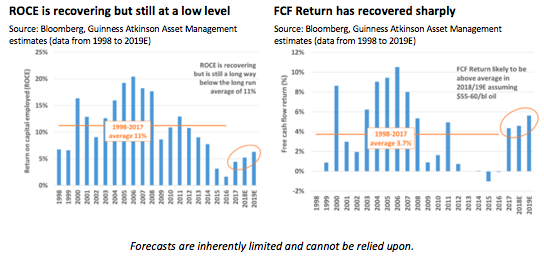

Our preferred method for monitoring longer term profitability is Return on Capital Employed (ROCE) while we use Free Cash Flow Return on Capital Employed (FCF Return) as our preferred measure of near term profitability movements.

• ROCE is recovering from a low of 2% in 2016 to around 5% in 2018. The long run average for our portfolio is around 11% and we see good reason to believe that profitability will return to around the long run average level, just as it did after 1998 when oil prices last hit a bottom. It takes time for ROCE to improve but we have increasing confidence that this will happen.

• We are comfortable with this because the FCF return has rebounded sharply and is now at above average levels (based on only $55/bl crude oil prices). This is a pre-cursor for improving ROCE.

How will energy equities perform if company profitability improves?

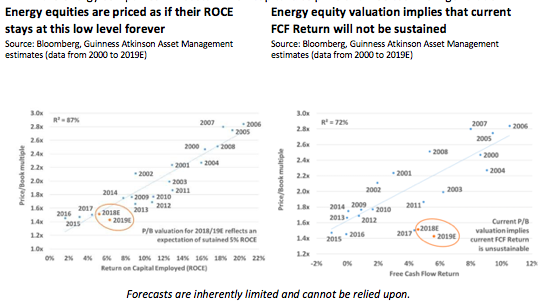

The stock market has historically valued energy companies based on their sustainable levels of profitability (generally a combination of both ROCE and FCF Return) whether it is delivered by self- help improvements or via increases in the long term oil price.

• Current valuation implies that the ROCE of our companies will not improve from the current level. If ROCE improves to 11% and the market were to pay for it sustainably, it would imply an increase in the equity valuation of around 40%.

• Current valuation implies that the FCF Return of the portfolio will fall considerably from current levels. If FCF Return maintains these levels, and the market paid for it sustainably, it would imply an uplift in equity valuation of 45%. Currently, the market is very skeptical that the energy companies will sustain their capital discipline and free cash flow generation.

So, if we are correct, what is the potential outcome?

Ultimately, we see rising profitability for the Guinness Atkinson Global Energy portfolio stemming from a combination of higher long dated oil prices and sustained capital discipline. After a long period of underperformance relative to the broad market, we see energy equities now playing catch-up.

The Fund’s portfolio may change significantly over a short period of time; no recommendation is made for the purchase or sale of any particular stock.

The Fund's investment objectives, risks, charges and expenses must be considered carefully before investing. The statutory and summary prospectuses contain this and other important information and can be obtained by calling 800- 915-6565 or visiting www.gafunds.com. Read and consider it carefully before investing.

The Fund’s holdings, industry sector weightings and geographic weightings may change at any time due to ongoing portfolio management. References to specific investments and weightings should not be construed as a recommendation by the Fund or Guinness Atkinson Asset Management, Inc. to buy or sell the securities. Current and future portfolio holdings are subject to risk.

Mutual fund investing involves risk and loss of principal is possible. The Fund invests in foreign securities which will involve greater volatility, political, economic and currency risks and differences in accounting methods. The Fund is non-diversified meaning it concentrates its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund. The Fund also invests in smaller companies, which involve additional risks such as limited liquidity and greater volatility. The Fund’s focus on the energy sector to the exclusion of other sectors exposes the Fund to greater market risk and potential monetary losses than if the Fund’s assets were diversified among various sectors. The decline in the prices of energy (oil, gas, electricity) or alternative energy supplies would likely have a negative effect on the fund’s holdings.

Opinions expressed are subject to change, are not guaranteed and should not be considered investment advice.

Distributed by Foreside Fund Services, LLC

© Guinness Atkinson

Read more commentaries by Guinness Atkinson Asset Management