Executive Summary

A rising global interest rate environment is once again leading to volatility in the emerging debt markets. Year-to-date through May 31, as the US Treasury 10-year yield has risen to the 3% neighborhood, the EMBIG benchmark of sovereign hard currency bonds is down 4.3%, and the GBI-EMGD benchmark of local currency sovereign debt is down 3.7%. In a piece I wrote in June of 2015 on the eve of the Fed’s long-awaited tightening cycle, I highlighted several reasons why the emerging debt markets should not panic at the Fed’s monetary policy normalization.1 And, while the EMBIG returned only 1.2% in 2015, it went on to return 10.2% and 9.3% in 2016 and 2017, respectively, amid ongoing Fed rate hikes. In this piece, I present some updated and different thoughts on how we at GMO think about the impact of rising rates on sovereign hard currency bond spreads. For now, I will limit the discussion to hard currency bond spreads by linking rising rates to the credit fundamentals via public debt sustainability analysis. I find that economic growth matters much more than interest rates to a country’s public debt dynamics. Lower global growth is a much larger risk to emerging markets than higher global interest rates.

As a fixed income asset class with relatively high duration, sovereign emerging debt is sensitive to interest rates. But is there anything else we can say? The yield on a sovereign debt portfolio can be broken down into two main components – the risk-free yield (US Treasury of similar duration) plus a credit spread. Therefore, it is clear that, ceteris paribus, a rise in the US Treasury (UST) yield will lower the price of the portfolio via this risk-free yield component. But need it be the case that a rise in the UST yield also affects the credit spread of the emerging debt portfolio? Thus far in 2018, we have witnessed exactly this phenomenon. Rising UST yields have been associated with rising credit spreads (56 basis points through May 31). But are there historical or theoretical underpinnings that justify this move? This will be the subject of this paper.

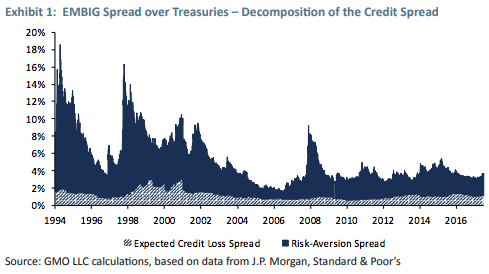

In Exhibit 1, we segment the credit spread of the EMBIG benchmark into two components. The smaller component is the pure credit risk premium. Think of this as the spread, in basis points, required to compensate a risk-neutral investor for credit losses due to default. We calculate this using an algorithm we developed that uses ratings transition matrices provided by the rating agencies to calculate default probabilities for countries in the benchmark. When combined with other assumptions, including recovery values in the event of default, we can calculate this “expected credit loss spread.” Notice that this is the smallest of the two components of the overall credit spread. This is because the average credit quality of the benchmark is fairly stable over time, and, indeed, the historical experience is that sovereign defaults are, thankfully, rare. There is, on average, about one sovereign default per year. Moreover, our internal analysis of sovereign defaults over the past 20 to 25 years reveals that they tend to be idiosyncratic and uncorrelated. Therefore, in a benchmark with more than 60 countries, there is a strong diversification benefit (from default risk, anyway). Overall then, it is intuitive to us that this spread component should be relatively small and relatively stable over time. Currently it stands at about 114 basis points.

The other, larger, spread component is a different matter. For the purposes of this paper, we will call it the “risk-averse spread.” This spread compensates the investor for risk aversion, market sentiment, liquidity, and other factors. Not only is it a much larger component (except for the pre-crisis period between 2005 and 2007 when it was about the same as the credit spread premium), but it is also much more volatile. It moves with the vagaries of global markets, and sometimes has little to do with developments within emerging markets. The year 2008 is a case in point. One can see in the exhibit that this risk-averse spread widened to about 700 to 800 bps in 2008, yet the pure credit spread moved relatively little. This is consistent with the observed fact that only one country in the benchmark defaulted in 2008 – Ecuador – which at the time was roughly 1% of the benchmark.

In thinking about the impact of UST rates on emerging sovereign credit spreads, let’s consider each type of spread in turn, beginning with the expected credit loss spread. How might rising interest rates affect this spread? We believe the most direct transmission channel is through the effect on the public debt dynamics, which also represents an important input into our country risk assessment process.

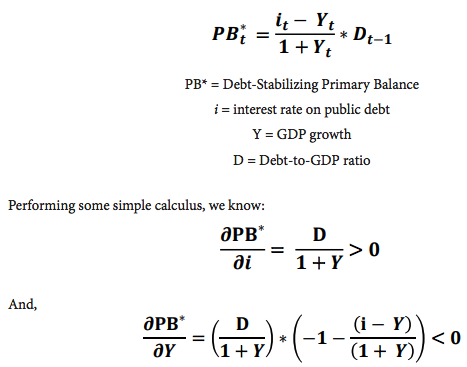

We know from the established algebra of public finance that the primary fiscal balance (the fiscal balance excluding interest payments) that is needed to stabilize a country’s debt-to-GDP ratio is a function of the interest rate on the debt and GDP growth in the following way:2

In words, an increase in the average interest rate on public debt increases the primary balance a country needs to run in order to stabilize the debt-to-GDP ratio. It increases that hurdle and places more pressure on fiscal performance. In contrast, an increase in GDP growth reduces the primary balance hurdle needed to stabilize the debt dynamics. These are intuitive conclusions that are proven by the mathematics. This leads to the question of how sensitive these variables might be to rising US rates.

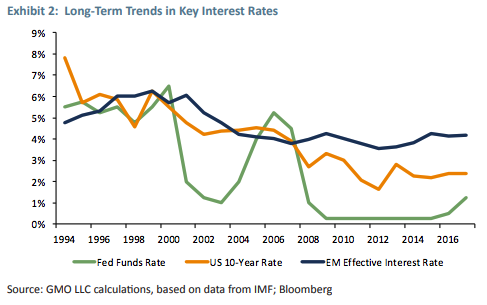

In Exhibit 2 we show the long-run trend in the average interest rate on emerging market countries’ public debt, alongside the Fed funds target and the 10-year UST. A first observation is that the rollercoaster ride in the Fed funds rate appears to have very little relationship with emerging countries’ cost of borrowing. This is intuitive, because very little of this debt is contracted on a floating-rate basis, unlike the 1970s and 1980s when money center banks were the primary lenders and most debt was linked to LIBOR.

Second, over this period the average cost of public debt in emerging countries fluctuated within a band (approx. 4% to 6%) that was much more narrow than the 10-year UST (approx. 2% to 8%). We believe this is the result of several trends and features in developing country public finance. For example, these countries have access to concessional financing from bilateral and multilateral lenders that can be “toggled” on or off depending on the state of the world. To be sure, in recent years it has been “toggled off ” in favor of international bond markets where, thanks to low UST yields, more lenient conditionality, and other attributes, this practice has led to record bond issuance. However, if there were a sudden large increase in UST yields, this concessional financing would likely be toggled back on. Another trend has been the emergence of local bond markets. As more and more countries have adopted inflation-targeting monetary policy regimes, leading to more predictable inflation outcomes, these markets have become an important alternative source of financing for governments. Additionally, at least in the case of internationally-issued sovereign bonds, maturities tend to be long. The average life of these bonds held in the EMBIG index, for example, is over 11 years. Therefore, while it takes little time for the marginal cost of financing to be affected by an increase in UST yields, it takes a long time for it to affect the average cost of financing for these countries.

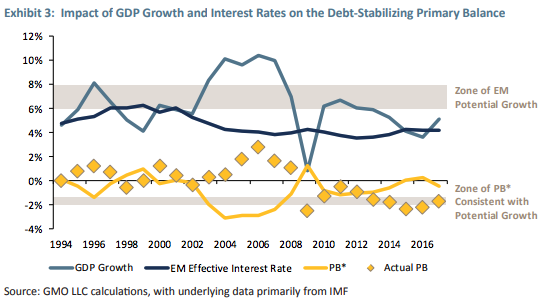

Now let’s introduce economic growth, the other main determinant in the debt dynamics, into the analysis, which is the subject of Exhibit 3. The main conclusion from this chart is that economic growth matters much more for debt sustainability than interest rates, at least within normal historical bounds for these variables. In the exhibit, we plot the average interest rate from the previous exhibit, along with the economic growth rate for the countries in the EMBIG benchmark. With these inputs, we can then calculate and plot the debt-stabilizing primary balance in each year. For added emphasis, we also plot the actual primary balance in each year. Finally, by defining a range for the rate of potential GDP growth for emerging countries, which we estimate at 6% to 8% in nominal terms, we can calculate a range of primary fiscal balance that should stabilize the debt-to-GDP ratio over the longer run, which we estimate as a deficit of 1% to 2% of GDP for the average country, per the exhibit.

I could write several pages on this exhibit, but let me try to close by highlighting a few items, including a reason for caution on the future. First, by far the most dominant determinant of PB* in any given year is the rate of GDP growth, as is obvious in the exhibit. It appears much more relevant to debt dynamics than the interest rate, which we discussed earlier. Indeed, economic growth, for this reason and others, features prominently in our country risk assessment process. During times of high economic growth, such as the 2004-07 period, PB* was a very low hurdle that was relatively easy for countries to reach. Indeed, the actual primary balance, as seen in the exhibit, was in strong surplus for the average emerging country during those years, as strong growth facilitated cyclically-sensitive tax revenues. One would expect debt-to-GDP ratios to have fallen during that time, boosting creditworthiness, and they did so (not shown).

The second point to highlight is one of caution. In the more recent years since the end of the global financial crisis, debt dynamics and fiscal performance have worsened, on average, in emerging countries. Emerging country growth has been at or below the lower end of our range for potential, even as UST yields also reached historical lows. The debt-stabilizing primary balance for the average EMBIG country has been 0% to -1% of GDP by our calculations, yet the actual primary fiscal balance has been significantly below that. By our calculations displayed in Exhibit 3, it has been the longest stretch of irresponsible fiscal policy in the last 25 years, and there is little doubt that quantitative easing and extremely low developed market interest rates fostered this profligacy, via virtually unfettered access to international bond markets by even low single-B rated countries. But the trends are not alarming. While debt-to-GDP ratios have moved higher, they remain within manageable bounds for the vast majority of the countries in our universe. Nevertheless, this trend is consistent with the downward drift in sovereign credit ratings we have observed in recent years.

The final point is that if our zone of potential GDP growth (we calculate this as roughly 4% to 5% real growth and about 2% to 3% inflation to arrive at 6% to 8%) is roughly correct, the corresponding zone of PB*, at 1% to 2% of deficit, judging from the historical experience, is very achievable, notwithstanding recent slippages.

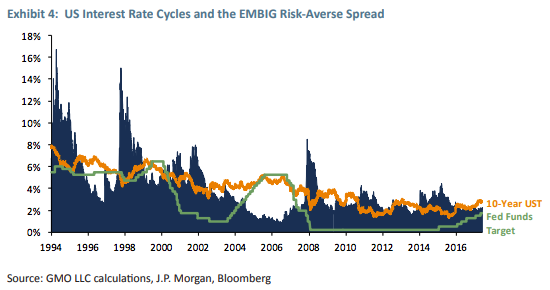

Now, let’s turn to the risk-averse spread. In Exhibit 4 we plot this spread component along with the Fed funds target rate and the 10-year UST yield. A few things are noteworthy. First, there have been relatively few Fed rate tightening cycles during this period,3 and in all three of those cycles (1999- 2000; 2004-06; 2015-current), the risk-averse spread was actually falling on a trend basis, not rising. Conversely, episodes of Fed easing have more often been associated with a rising risk-averse spread, not a falling one. This is somewhat counter to the casual observation of the market’s obsession with Fed meetings, minutes of Fed meetings, Fed-speak, non-farm payroll releases, and other high frequency data.

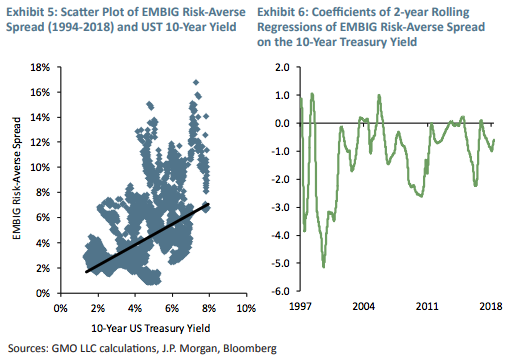

Second, the same phenomenon seems to apply with respect to the 10-year UST yield. To be sure, we can clearly see a secular decline in UST yields and the risk-averse spread, but upon closer inspection of shorter time periods, we observe that periods of rising UST yields are more often associated with falling risk-averse spreads, and vice versa. We demonstrate this in Exhibits 5 and 6. Exhibit 5 is a scatter plot of the data set over the entire period. Because UST yields and sovereign spreads have both declined on a secular basis, we observe a positive correlation. However, in shorter time periods, this is not the case, as seen in Exhibit 6, where we plot the time series of coefficients of rolling 2-year regressions on the UST yield and the risk-averse spread. Most of the time, we see a negative coefficient. In other words, most of the time, over a 2-year period, UST yields and risk-aversion spreads are moving in opposite directions.4

Does this result fit with intuition? Does it fit with the market’s fear of the end of tapering and its apparent obsession with Fed meetings? We believe it does, despite the opposite knee-jerk, short term reactions we often observe in the market that cause short-term bouts of volatility. The reason is that periods of rising UST rates are often associated with reflationary environments in which global economic growth is strong. These periods are generally positive for emerging market fundamentals. In contrast, falling UST rates and yields are often associated with deflationary environments and risk aversion that results in a flight to “quality” in US Treasuries.

Based on this analysis, we conclude that there is very little evidence that rising US rates should cause the risk-averse spread on emerging sovereign debt to increase, as long as the process is relatively orderly, which monetary policy officials seem keen to ensure. Rather, the risk-averse spread seems to be influenced by exogenous factors and shocks that are impossible to predict. Sometimes these shocks emanate from the emerging world, such as the Asian and Russian crises of 1997-98, and sometimes they come from the developed world, such as the global financial crisis, the tech bubble, or the European sovereign debt crisis. Many of the extreme widening periods in the risk-aversion premium have little to do with emerging country fundamentals.

Conclusions

We do not mean to minimize the importance of rising UST yields and policy rates on the hard currency emerging debt asset class. The market’s reaction this year indicates that they may have some influence on spreads. But the historical evidence and the actual theoretical underpinnings tell us that the effects need not be significant. Rather, GDP growth is much more impactful on the debt dynamics. However, our analysis also indicates that a scenario in which rates and borrowing costs are rising, and GDP growth in developing countries is falling, would be a double whammy to the debt dynamics. Despite all the talk of “synchronized global growth,” the market might be indicating its concern over a negative global supply shock scenario (caused, for example, by trade wars and spreading economic nationalism) that would raise inflation and interest rates and decrease global growth. According to our analysis, such a reality would justify higher credit spreads via the impact on debt dynamics.

Our sovereign risk assessment process places high importance on fiscal performance and debt dynamics. We pay close attention to how far away countries are from the primary balance that would stabilize their debt-to-GDP ratio. We wish the “initial conditions” were stronger, and it is likely that the borrowing binge we have seen in recent years is indirectly responsible for some of the spread widening we have seen in recent months, because the market is extrapolating recent subpar fiscal performance into the future. If UST yields continue to rise, we would expect countries’ public debt management teams within the finance ministries to realign borrowing, perhaps in favor of local markets or concessional financing. We would also expect them to try to convince politicians to rein in fiscal spending and reduce deficits. We will be watching for these trends and adjusting our country risk assessments accordingly.

Carl Ross. Dr. Ross is engaged in research for GMO’s Emerging Country Debt team. Prior to joining GMO in 2014, he was a managing director at Oppenheimer & Co. Inc. where he covered emerging debt markets. Previously, he was the Senior Managing Director and Head of Emerging Markets Fixed Income Research at Bear Stearns & Co. Dr. Ross earned his BA in Economics from Mount Allison University as well as his M.A. and PhD in Economics from Georgetown University.

Disclaimer: The views expressed are the views and understanding of Carl Ross through the period ending June 2018, and are subject to change at any time based on market and other conditions. While all reasonable effort has been taken to insure accuracy, no representation or warranty for accuracy is provided nor should be assumed. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

1 See “The Imminent Fed Rate Hike – Impact on Emerging Market Debt,” dated June 2015. This is available from your GMO representative.

2 See, for example, https://www.imf.org/external/region/tlm/rr/pdf/aug7.pdf

3 We chose the year 1994 to begin the analysis as this corresponds to the inception of GMO’s Emerging Country Debt Strategy.

4 We performed the same regressions using six-month and one-year periods and obtained similar results.

Copyright © 2018 by GMO LLC. All rights reserved.

© GMO

Read more commentaries by GMO