Weighing the Week Ahead: Will Incipient Headwinds Derail the Economy?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is loaded. The many reports include several of the most-watched. The data may even generate enough fresh news to break the summer slumber. There is plenty of skepticism about the most recent economic data. I expect pundits to be asking:

Will incipient headwinds derail the economy?

Last Week Recap

In my last edition of WTWA I guessed that a boring week would lead to reviews of what strategies had been working in the first part of the year. There was some of that, and it certainly was not an exciting week for financial news. The focus turned to stories with great human interest, ranging in importance from family separation at the border to a CEO replacement for violating fraternization rules, to what Mrs. Trump was wearing on her trip to visit detained children.

And of course, continuing rounds of escalation in the growing trade war.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. I especially like the version updated each week by Jill Mislinski. She includes a lot of valuable information in a single visual. The full post has even more charts and analysis, including commentary on volume. Check it out.

The market was down 0.88% with opening gaps in both directions on several days. Despite the seesaw appearance, the trading range was less than 1.2%. I summarize actual and implied volatility each week in our Indicator Snapshot section below. Volatility is back into the long-term range.

Personal Note

It is very nice to be recognized as one of the 100 Most Influential Advisors of 2018 by Investopedia. Their criteria emphasize several important communication factors, not just the size of the business. While we have been growing nicely, we are agile enough to provide great service and specialized programs for each investor.

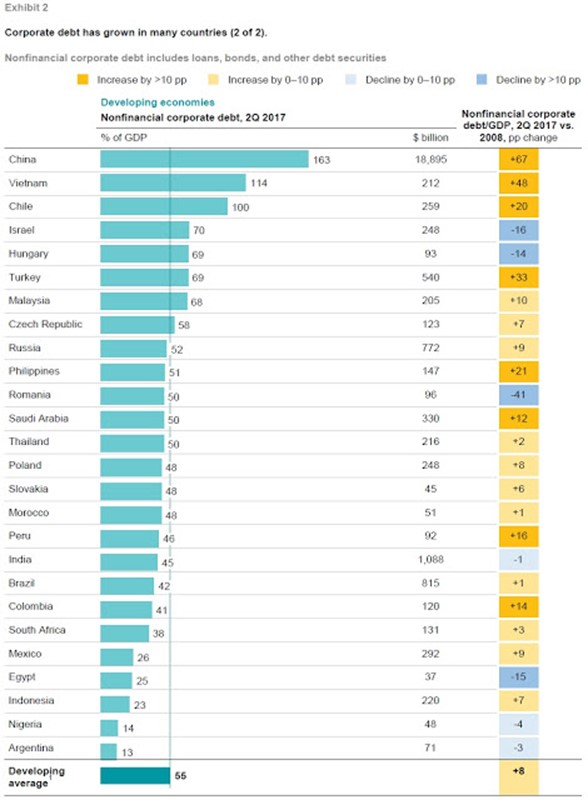

Noteworthy – Worldwide Corporate Debt

Timothy Taylor observes that overall world debt is at an all-time high when measured as a share of GDP. The components of the debt have shifted from government borrowing (during and after the Great Recession, to corporate borrowing. He writes as follows:

Moreover, this corporate borrowing has two new traits. One is that as bank regulators all over the globe have tightened up, this rise in corporate borrowing tends to take the form of bonds rather than bank loans. The other interesting trait is that this rise in corporate borrowing around the world can be traced back to developing economies–and especially to China.

Prof. Taylor has a good summary of a recent McKinsey Global Institute paper. He also reaches several investment conclusions, including care in buying this debt.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

The Good

- Housing starts grew at a SAAR of 1350K, up from 1286K and beating expectations of 1323K. Calculated Risk notes that the increase is 20.3% compared to May 2017 – but observing that it was an “easy” comparison. Bill’s key point is that the starts now reflect single family much more than the flattening multi-family results. Check out the full update for the expected excellent charts.

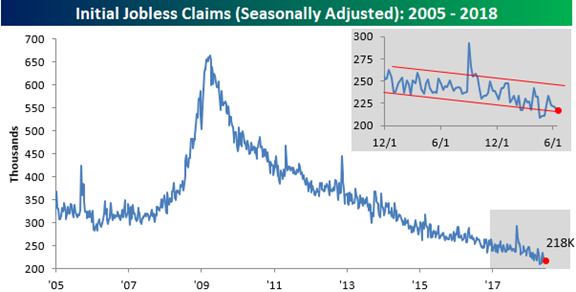

- Initial jobless claims were only 218K, once again beating expectations and maintaining the extremely low level. (Bespoke)

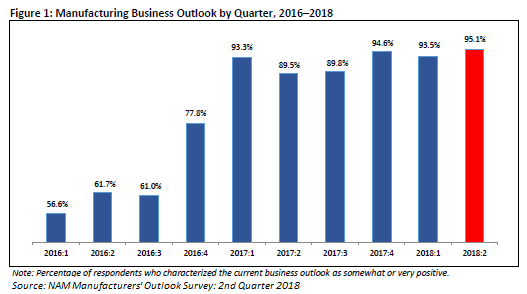

- Manufacturers’ optimism is at a record high. David Templeton (HORAN) provides careful analysis, data, and several charts. Here is one.

- Architectural billings strengthen to 52.8. Calculated Risk notes that this is a leading indicator (about 9-12 months).

- Foreclosure starts are the lowest in 17 years. (Black Knight via Calculated Risk)

The Bad

- Leading economic indicators increased only 0.2% versus 0.4% last month and expectations of another 0.4% increase.

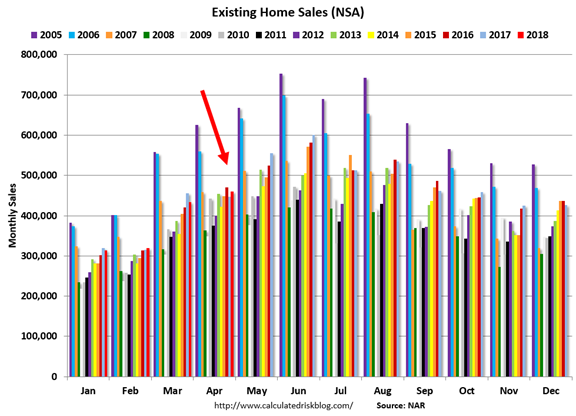

- Existing home sales registered only 5.43M (SAAR) down slightly from April and missing expectations of 5.55M. Calculated Risk notes that the small decline does not tell us much about the effect of interest rates or tax law changes. One reason I regard Bill as my top source on housing is his open-minded approach to data. In addition, he is willing to move with the evidence, uses a wide variety of sources, and has been quite accurate through more than a full market cycle.

- Building permits increased 1301K down from April’s 1364K and expectations of 1350K. These are all seasonally adjusted numbers.

- Hotel Occupancy declined, although the series maintains a lead over the 2017 record. (Calculated Risk).

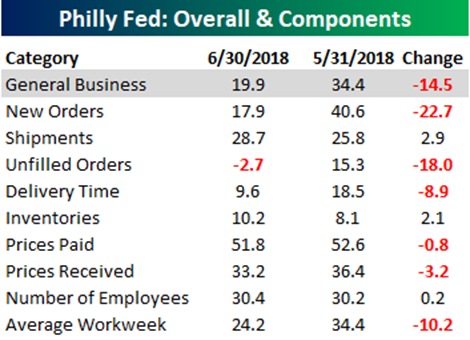

- The Philly Fed index for June was only 19.9 with expectations for 27.0. I do not pay much attention to this measure, but some academic studies show that many market participants do. Perhaps it is because of its status as the first report for the current month. Bespoke’s analysis includes a look at the components.

The Ugly

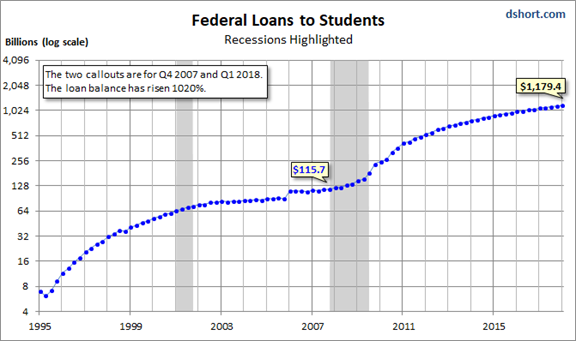

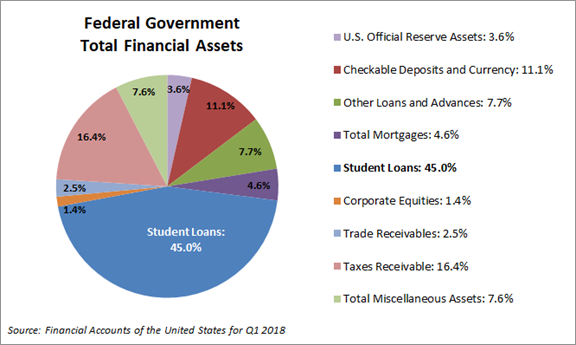

The largest US asset is……? This has a bad feeling about it for both borrower and lender. See the post byJill Mislinski for more charts and analysis.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

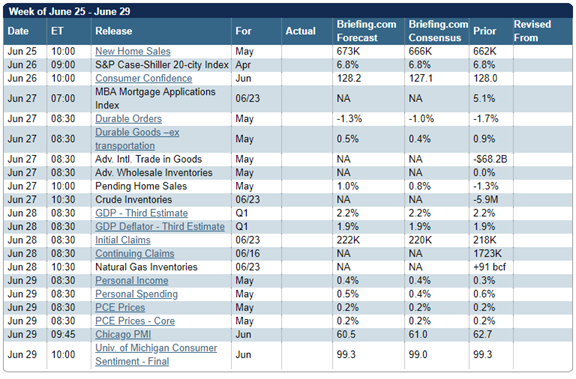

The Calendar

The calendar is loaded with releases, including several of the most important. Consumer confidence and sentiment from the major sources, home sales, income and spending are all important. The third estimate of Q1 GDP is “old news” but many will contrast it with the strong real-time indicators for Q2. The PCE price report gets less attention than the CPI, but it is the Fed’s favorite measure.

And of course, we can expect plenty of trade news from around the world.

Briefing.com has a good U.S. economic calendar for the week (and many other good features which I monitor each day). Here are the main U.S. releases.

Next Week’s Theme

This is a big week for economic reports. There will be plenty of fresh news for those seeking to assess current economic strength. We can also expect frequent developments on trade issues. These potential headwinds are the biggest threat to corporate earnings growth.

Mrs. OldProf is a sports fan, but not a hockey fan. Despite her cursory attention to the NHL draft, she did not fall for my straight-faced comment about the tariff on Canadian hockey players.

The current, real-time economic assessments remain amazingly strong. It is not surprising that many question the data, the conclusions, or the effect of perceived headwinds.

I expect pundits to be asking:

Will threatened headwinds derail economic growth?

As usual we have a wide range of opinion. It is difficult to do my regular scale for these, but here is a general listing from bullish to bearish. As always, I have read recent reports supporting each viewpoint.

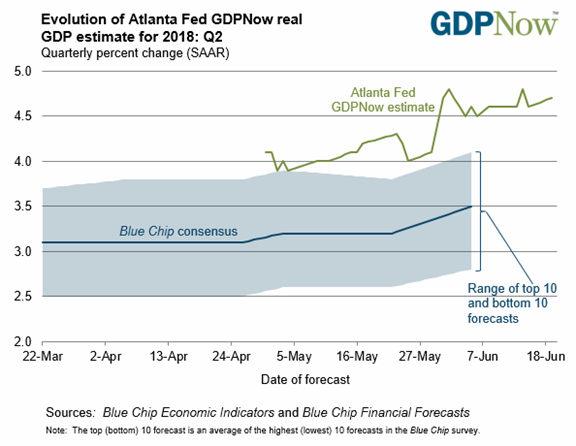

- A current growth rate of 4.7%, a slight downward revision during the week. (Atlanta Fed)

- Inaccurate measures and forecasts.

- Currently strong but already signs of peaking.

- Unsustainably high level – low productivity growth, demographic headwinds, rising debt.

- Fed will limit growth (and/or kill it say aggressive Fed opponents).

- Immigration effects – estimated to subtract about 1% from potential growth.

- Tariff effects – the trade war is escalating (The Economist). Currently estimated for a 0.2% impact on growth, but it could easily be a full point or higher with escalation.

- Crash coming says a billionaire investor.

These are all important, with significant potential impacts. As usual, I’ll offer my own conclusions in today’s Final Thought.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

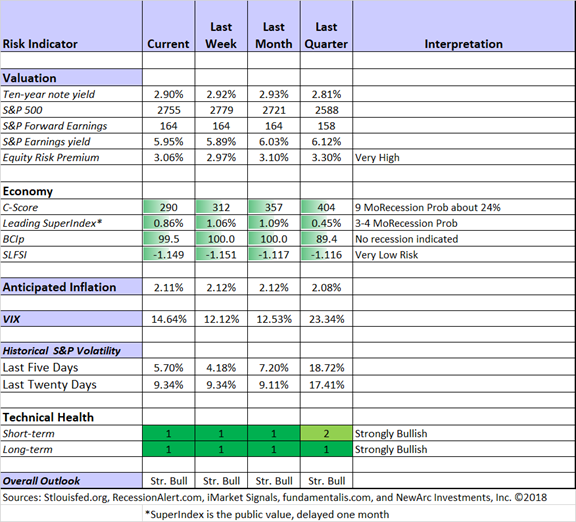

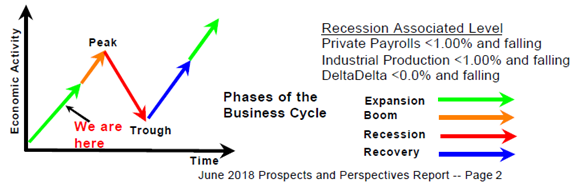

Short-term trading conditions continue at highly favorable levels, reflected by our trading program results. Both actual and implied volatility are low, with the VIX (a measure of market expectations) remaining higher than reality. The C-score has dropped further. I continue to watch this carefully. My co-inventor Bob Dieli recommends supporting the conclusions with other concurrent indicators and I agree. He does a complete economic summary in one of his valuable monthly releases. This is important information for serious investors and less expensive than most other institutional-strength products. Here is his latest business cycle update, fully explained in the monthly report. Avoiding the “late innings” fear has been very profitable for Bob’s subscribers.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

Georg Vrba: Business cycle indicator and market timing tools. None of Georg’s indicators signal recession.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis.

Guest Sources:

Scott Grannis notes Key Credit Indicators Still Green. He writes:

We are now 2 ½ years into a Fed rate-hiking cycle: the Fed started raising short-term rates in late 2015 from a low of 0.25% to now 2.0%. Real yields have risen from -1.5% to now about zero—still very low from an historical perspective. Not surprisingly (since there has effectively been no tightening), there are still no signs of rising systemic risk or deteriorating credit conditions. Credit spreads remain low and liquidity remains abundant. Although the Fed has been draining bank reserves, they are still magnificently abundant, totaling about $1.9 trillion.

Dr. Tim Duy, the leading Fed watcher responds to the blaring headlines of recession warnings – this time from David Rosenberg. Rosie opines that cycles end because “the Fed puts a bullet in its forehead.” [Our own favorite business cycle expert, Bob Dieli reaches the same conclusion about the general pattern. But not now].

Prof Duy writes:

I buy the story that the Fed is likely to have a large role in causing the next recession. Either via overtightening or failing to loosen quickly enough in response to a negative shock.

And I truly get the frustration of being a business cycle economist in the midst of what will almost certainly be a record-breaking expansion. Imagine a business cycle economist going year after year without a recession to ride. It’s like Tinkerbell without her wings.

But the timeline here is wrong. And timing is everything when it comes to the recession call. Recessions don’t happen out of thin air. Data starts shifting ahead of a recession. Manufacturing activity sags. Housing starts tumble. Jobless claims start rising. You know the drill, and we are seeing any of it yet.

For a recession to start in the next twelve months, the data has to make a hard turn now. Maybe yesterday.

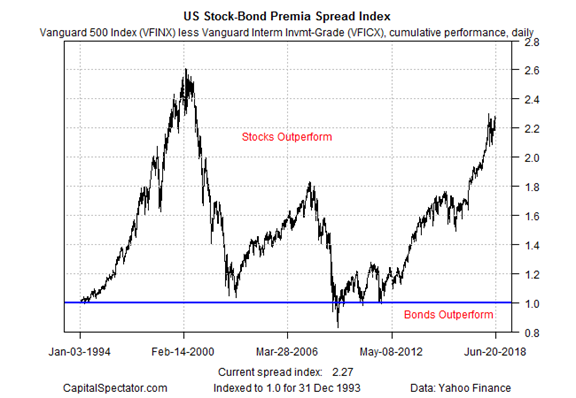

James Picerno notes the recent strength of stocks versus bonds and asks how long it can continue.

Insight for Traders

Check out our weekly Stock Exchange post. We combine links to important posts about trading, themes of current interest, and ideas from our trading models. This week we asked fellow traders about their trading “personality.” The character guide to our models shows a personality for each of them. The diverse approaches are all generating excellent results, but the stock selections vary widely. We also highlight trading posts from leading sources. The ratings from Felix and Oscar this week feature the S&P 500. Blue Harbinger is our editor for this information and ringleader for the group discussion.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility.

Best of the Week

If I had to pick a single most important source for investors to read this week it would be Jack Vogel’s analysis at alpha architect, Trust the Process. As I like to do myself, he tries to create open-mindedness in readers by stepping away from pre-conceived investment conclusions. A sports analogy is often a good vehicle, especially if it can be understood by those who are not fans of the particular sport.

He then considers several different investment approaches, analyzing the risk and results over different time intervals. Many will be surprised at the conclusions from the data. The most important evidence is that analysis of past data is very sensitive to the period chosen. His conclusion is important and right on target:

When it comes to investing, answering the question, “Can I trust the Process?” is very hard. Sometimes the process will not work over long periods, which can make trusting the process even harder.

The three examples given above were not necessarily out of the blue, as these are approaches to investing that we believe in:

- Stocks will have higher returns than bonds in the long run.(18)

- Value and Momentum are two ways one can attempt to beat the benchmark.

- Trend-following is a decent attempt to lower drawdowns on all asset classes.

Yes, we are fans of equity investing, as well as the value, momentum, and trend factors.

This is nice work, clearly explained and using relevant data. Dr. Vogel takes on a difficult and important topic and handles it in a way that is understandable for the average investor.

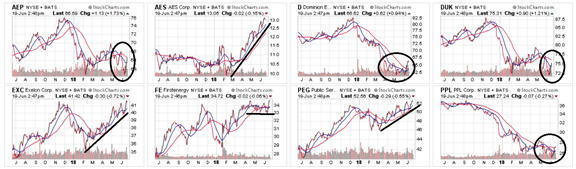

Stock Ideas

Chuck Carnevale continues his search for great companies where the valuation has become attractive. This week’s subject is PepsiCo (PEP). The valuation is back to 2013 levels and the dividend is solid. As usual, his post is also a lesson in stock analysis.

Colorado Wealth Management recommends a dividend champion REIT with an attractive chart, Tanger Factory Outlet Centers (SKT). REIT specialist Brad Thomas reaches the same conclusion, writing:

While Mr. Market and I may be on opposite sides, I am convinced that Tanger Factory Outlet (SKT) is the quintessential “diamond in the rough” – because the financial markets fail to fully incorporate fundamental values into the share price, and the investor’s margin of safety is the widest.

Alibaba (BABA) is a “no brainer” according to value investor Jae Jun. Here is his dramatic conclusion:

Alibaba has built the economy to what it is now and has the backing of the government. It’s an unfair advantage that Alibaba has taken full advantage of. It comes with its own consequences, but the difference with Amazon in USA and Alibaba in China is that, should Alibaba shut down, China will be in chaos.

Hale Stewart analyzes the utilities in the FERC PJM region. Those interested in the sector (which does not excite me, but I know is of great interest) should study this for background as well as ideas.

And for those with a dividend focus, Rob Marstrand explains why buying a stock to capture the dividend does not help in the long term and might actually cost you through more taxes. This is a good lesson about the most important four dates related to dividends.

Stock Moats

Do you consider a stock’s moat as part of your investment decision? You should. Morningstar maintains aWide Moat Focus Index. They note that consumer defensives look cheap, reporting this list of recent additions.

Earnings Anticipation

Many investors consider buying or selling a stock right before an earnings report. Some sharp analysts provide early analysis useful for that decision or for a fast reaction to the announcement. D.M. MartinsResearch covers Carnival (CCL) and Brian Gilmartin does a nice report on Bed Bath & Beyond (BBBY).

Portfolio Construction

My contrarian take on portfolio construction includes several elements. Last week I described How to Choose an ETF. Most people emphasize past performance and fees – seemingly relevant and easy to find. I explain why a proven investment process is far more important. To illustrate, I described three of my personal holdings and why I like them. (CAPE, PLCY, and CWS). Check out the full post for more details. Eddy’s market comment this week underscored my observations about his record and the transparency of his process. He includes a detailed explanation of holdings and his current thoughts.

What I recommend is not radical for those who keep up with the latest work. But it is different from current themes and marketing. See this week’ best investment advice.

Personal Finance

Seeking Alpha Senior Editor Gil Weinreich has made a few more changes in his excellent series for financial advisors (and serious individual investors). Not only does he include some podcasts, but he also highlights other key issues. This week I especially enjoyed his post describing a possible “China Debt Trap.” A favorite link was Roger Nussbaum’s advice on calculating the income needed in retirement. This post was a response to Laurence Kotlikoff’s The 70% Replacement Rate in Retirement is Rubbish. That article is itself a response to Michael Kitces In Defence of the 70% Replacement Ratio in Retirement. This is an important topic for retirement planning, so dig as deeply as you can.

Abnormal Returns always has helpful links and now some longform posts as well. I am a subscriber, and I read every post. It is a helpful source for many ideas I feature on WTWA. On Wednesday he has a special group of links for those interested in personal finance. As usual, this week included many good ideas, my favorite is how the Financial Samurai explains why your risk tolerance is “an illusion” until it is tested by big losses.

Many investment managers, in a CYA move, use a questionnaire to determine “risk tolerance.” I find that a deeper interview and discussion is required.

Watch out for…

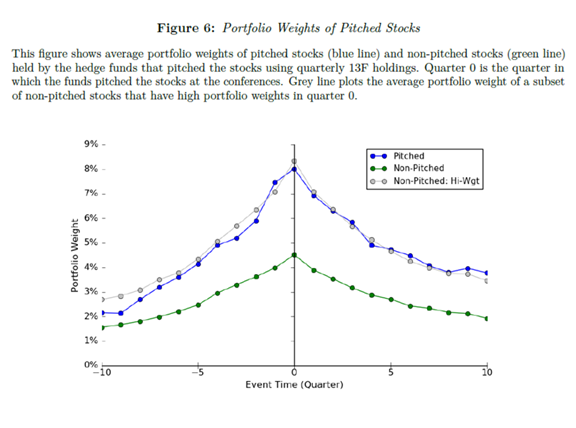

Hedge fund stock pitches. A Harvard Business School paper from PhD student Patrick Luo (viaBloomberg) suggests that the ideas presented at conferences are old ideas.

“This suggests that the pitched stocks were their ‘best ideas’ but not likely any longer,” Luo wrote. “Returns of pitched stocks diverged from market immediately after the pitches—long pitches spike up and short pitches spike down. These results suggest that these investment conferences are closely followed by other investors and have high market impacts.”

Starbucks (SBUX). Stone Fox Capital is concerned about replacing the company founder, Howard Shultz.

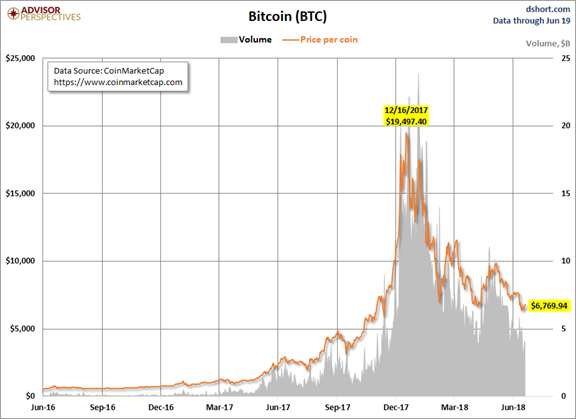

What next for crypto? The chart shows why this is a trading vehicle, not an investment, and why you should keep your positions small.

Final Thoughts

A trade war remains the most important threat to economic growth. It combines the potential for a lower GDP (and lower corporate earnings) with higher prices. (Rob Marstrand). I see only the first indications, but I am watching this matter closely. I am more willing than most to do some policy experiments. We certainly do not know everything in advance. That said, the policymakers must be willing to observe the effects and change course when indicated.

Signs of trouble

- EU tariffs (Gil Weinreich).

- Impact of Chinese tariffs on US manufacturers (WSJ).

- Mexican and Canadian tariffs (Barron’s and Econofact).

- Impact on farmers and commodities – soybeans, grain.

- Increased Chinese industrial espionage (Fortune).

Encouraging signs

- Policy shift on family separation. Some Trump Administration policies change in reaction to widespread opinion.

- Recognition of secondary effects of all types, including increased costs for US manufacturers. This is another important feedback loop.

- GOP legislators are more outspoken in opposition.

- The Koch Brothers lobbying Congress. Their far-flung business enterprises are a good reflection of economic effects. Their financial muscle in elections gets the attention of legislators. (Time – among many sources).

The Fear and Greed Trader’s excellent weekly review leads with a quotation from Peter Lynch:

“The key to making money in stocks is not to get scared out of them.”

He goes on to write:

Pessimism is intellectually seductive, and the arguments always sound smarter, because they dovetail with our own worries. That has been proven over and over in market history and is so abundantly evident during this bull phase of the market.

It sounds smarter. “Sounding” smarter doesn’t necessarily produce the desired results. Once we add money and investing to the mix, with pessimism surrounding that mixture, it takes on a whole different look. In our capitalist mindset, losing money is tantamount to a crime. It’s embarrassing and something no investor wants to talk about, yet losing money is a part of the investment cycle.

An author that puts together an article that calls for a recession will get far more page views than others. Call for a great depression and you might get a spot on CNBC. On the flip side, mention the good times ahead and put an optimistic slant on the situation, no matter how successful your view has been, and you have a “salesmen” attached to the end of your name.

Exactly right. When the economy is doing well, why not enjoy the benefits. It is prudent to keep an eye on the horizon, but foolish to make speculative guesses that something might go wrong.

I’m more worried about:

- Trade policy perceptions. The psychology can create a self-fulfilling prophecy, even if the result is benign. Economic growth is fueled by confidence.

- Google – now beating medical staff at predicting when you will die. Having more information seems like a good idea, but how will it be used?

I’m less worried about:

- The Fed. The transition to Chairman Powell seems to be a smooth one. There is a continuing focus on data and willingness to be flexible. (Hale Stewart)

- North Korea. So far, so good after the summit

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits