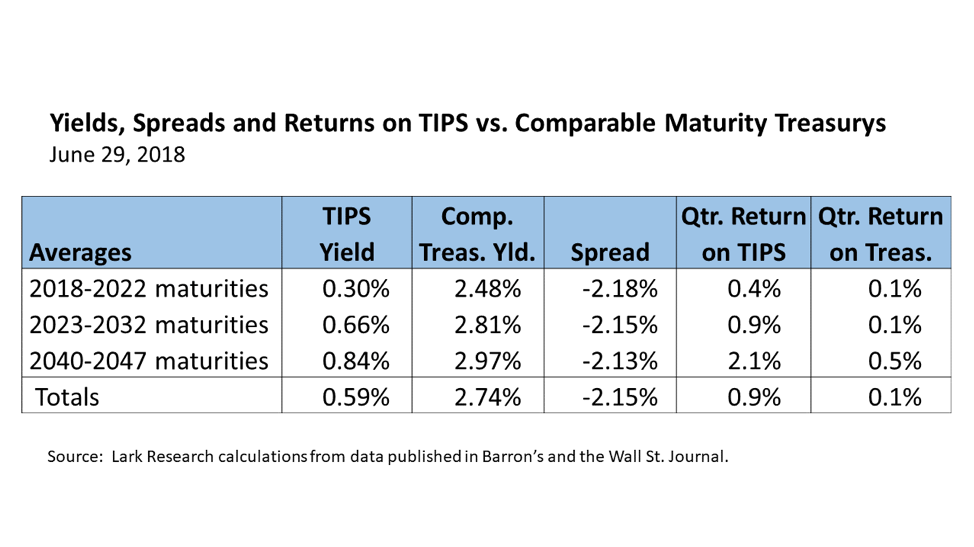

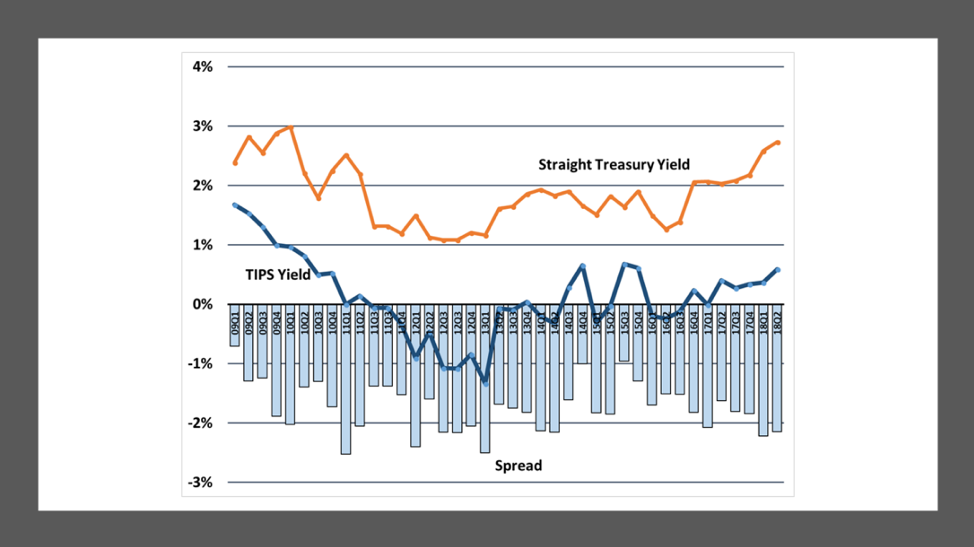

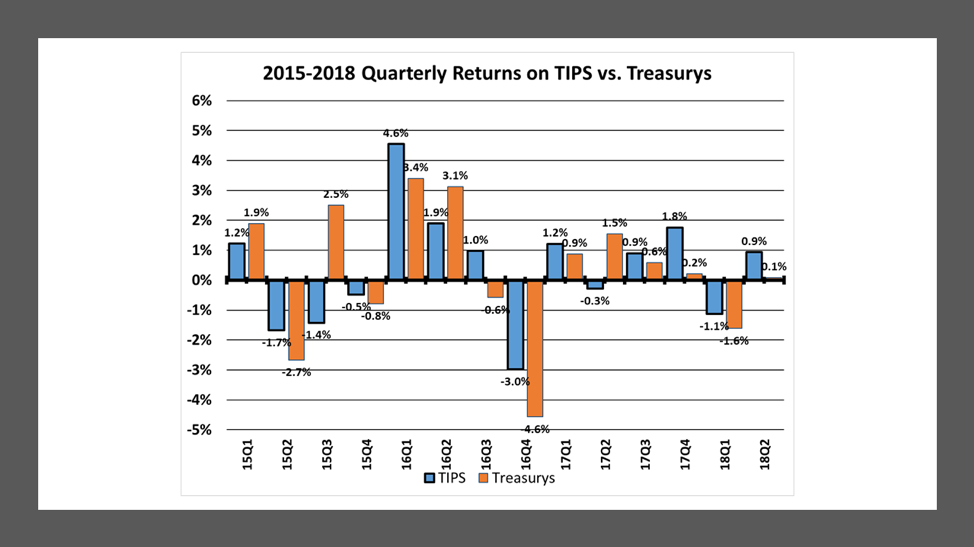

In a quarter when the pace of Treasury yield increases moderated, TIPS outperformed comparable maturity straight Treasurys. This was the fourth consecutive quarter that TIPS beat straight Treasurys. On average, TIPS gained 0.9% in the quarter, better than the 0.1% gain on comparable maturity straight Treasurys. The average yield on TIPS rose by 23 basis points (bp) to 0.59%, while the average yield on straight Treasurys increased by 16 bp to 2.74%. As a result, the average spread between straight Treasurys and TIPS yields declined by 7 bp from 222 bp to 215 bp.

A greater increase in TIPS yields ought to have led to TIPS underperforming straight Treasurys. But the negative drag of rising interest rates was more than offset by the CPI inflation adjustment. According to my calculations, the CPI added 1.08% to the average TIPS return during the quarter, the largest inflation adjustment in three years.

My return calculations exclude the returns generated on the newest 30-year TIPS and related comparable maturity Treasury bond, both issued in February. I excluded these bonds because their positive returns skewed the average total returns significantly. For example, with this new 30-year TIPS bond - the 1% TIPS due February 15, 2048 - the average total return on long-term TIPS would have been 3.3%, 115 basis points higher and the average return on all TIPS would have been 1.15%, 22 basis points higher. Likewise, including the comparable straight Treasury bonds – the 3% Treasury Bonds due February 15, 2048 – would have added 125 basis points to the average total return on long-term Treasurys and 22 basis points to the average total return. Sometimes (often?), newly issued bonds are priced to move (or timed just right). Those who purchased either of these bonds have so far reaped superior returns vs. benchmarks.

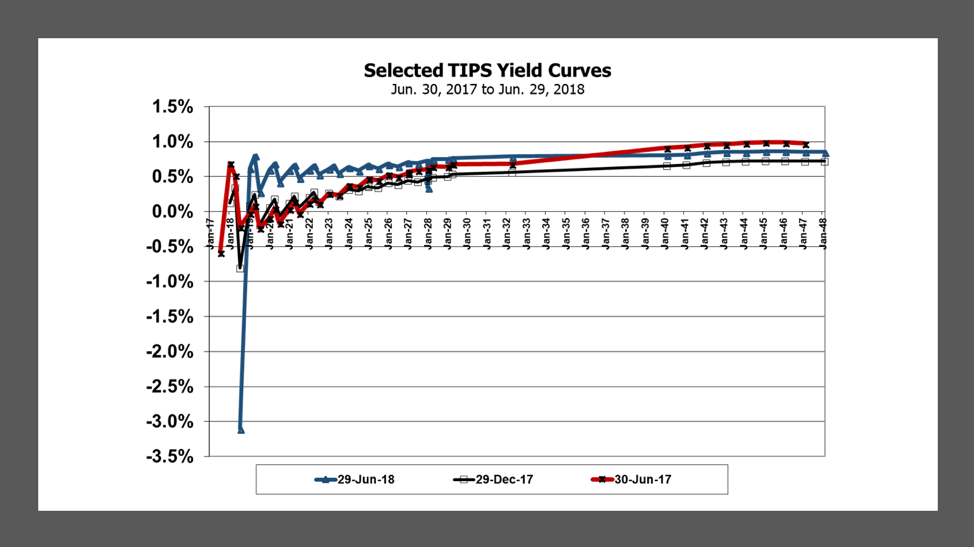

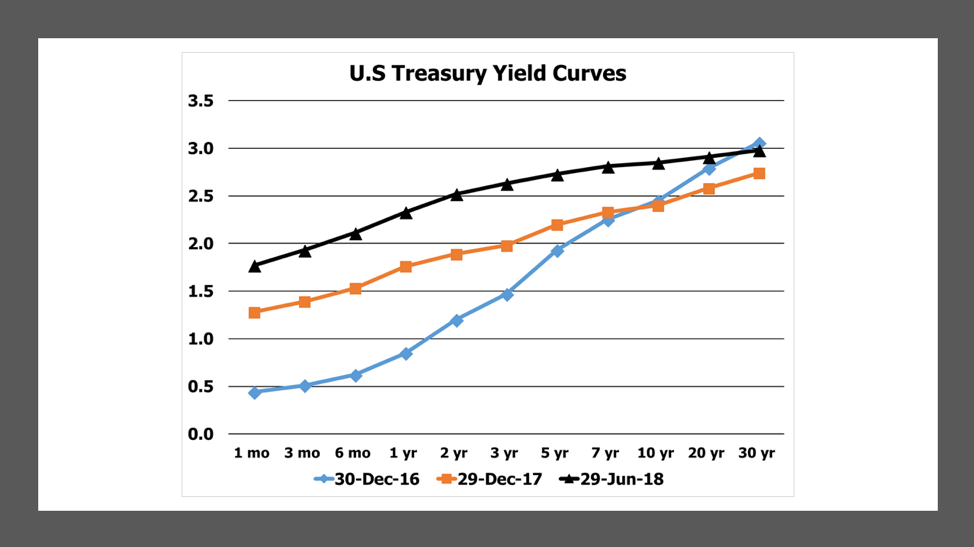

Like straight Treasurys, the US TIPS yield curve has flattened over the past twelve months, with short-term TIPS yields rising and long-term TIPS yields falling. Short-term TIPS yields have risen more than long-term yields have fallen. It is noteworthy that the average yield on short-term TIPS rose from ‑0.24% on March 29 to 0.30% on June 29, an increase of 54 basis points. Yet, short-term TIPS still posted a positive return of 0.4%, better than straight Treasurys 0.1%, entirely due to the CPI inflation adjustment.

The average yield spread between straight Treasurys and TIPS narrowed during the quarter by 7 bp from 222 bp to 215 bp. That spread is still at the high end of the nine-year range from 71 bp to 252 bp (with an average of 173 bp). TIPS may still be a good relative value versus Treasurys over the long haul, but the outlook for inflation may be moderating near-term. In that case, straight Treasurys might rally vs. TIPS bringing down the spread.

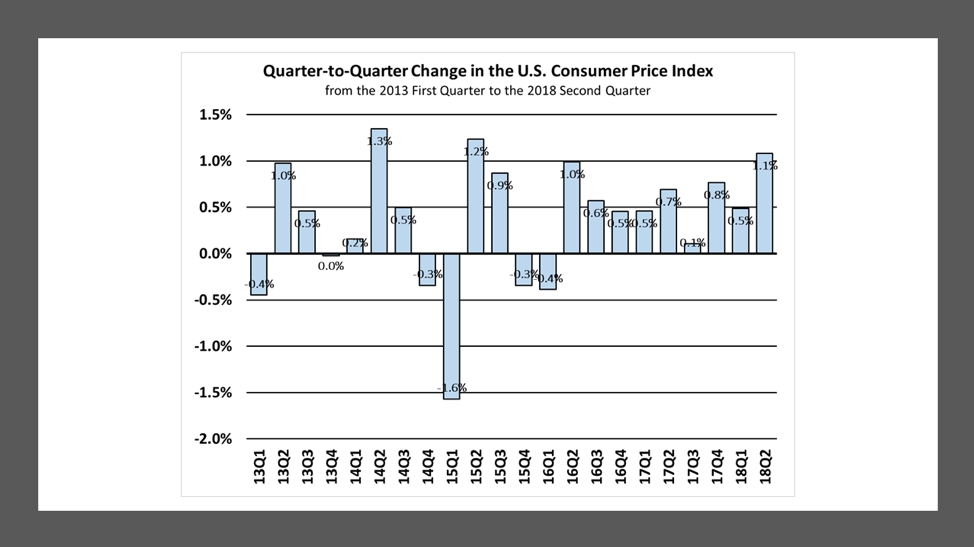

While the average yield on short-term TIPS was negative at the end of the first quarter, a sign that investors were betting heavily on a pick-up in inflation, the rise in the average short-term TIPS yield to 0.30% by the end of the second quarter suggests that the near-term outlook for inflation may have moderated. Year-over-year, the increase in May headline CPI was 280 basis points and core CPI (excluding food and energy) was up 224 basis points. The most recent Philly Fed Survey of Professional Forecasters anticipates that both headline and core CPI inflation will be 2.50% in 2018. (However, the Survey came out before the May CPI report was released, so it is possible that economists will take their 2018 CPI inflation forecasts up a notch in the next SPF report.)

Higher gasoline prices contributed to the increase in May CPI, but their effect on inflation will diminish over time as long gasoline prices do not continue to increase. Rising shelter costs also drove May CPI higher, with both (apartment) rents and owners’ equivalent rent posting meaningful increases. Nationally, seasonally-adjusted house prices have risen at a 5.6% compounded annual rate over the past five years and roughly about 6%-7% of the housing stock changes hands every year, so that rapid rate of house price appreciation is smoothed into housing costs (i.e. owners’ equivalent rent) over time. Yet, the month-to-month percentage change in shelter costs has picked up somewhat (to above a 4% annual rate) in recent months.

As already noted, the yield curve has continued to flatten, with short-term rates rising and long-term rates remaining largely range-bound. The spread between the 10-year Treasury yield and 2-year yield has narrowed from 125 basis points at the end of 2016 to 47 basis points at the end of 2017 and then to 33 basis points at the end of June.

According to the CBOE’s Fed Watch Tool, which calculates Fed Funds rate probabilities based upon futures prices, the market believes that there is a 78% chance that the FOMC will hike the Fed Funds rate by another quarter point (to a range of 2.00%-2.25%) in September and a 49% chance of another 25 basis points hike in December. If indeed the Fed does raise the Fed Funds rate twice more this year, it runs the risk of inverting the yield curve if long-term rates do not rise commensurately.

An inverted yield curve has historically been a reliable sign of an approaching recession1. History shows that the inverted yield curve has preceded every recession in the past 60 years. However, the timing of the recession that follows inversion is uncertain. Traditionally, it may come in as little as six months or as long as two years.

History also shows that the FOMC prompted recent yield curve inversion by raising short-term rates ahead of the past few recessions. It raised rates sharply in advance of economic slowdowns in 1989 (to fight inflation) and from 2004 to 2006 (to normalize interest rates). This time, however, may be different, as long as inflation remains in check. FOMC minutes from the June 2018 meeting indicate the risk of yield inversion was discussed at length, so the Fed appears to be closely following yield curve developments. Some economists also suggest that inverting the yield curve may not necessarily presage a recession this time around because interest rates remain very low and monetary policy is still extraordinarily accommodative.

Since sustaining and promoting economic growth is a top priority of both the Fed and the Federal government, it would be surprising if the FOMC were to engineer the next yield curve inversion. As long inflation remains in check (with a potential acceleration in wage growth a primary concern), the FOMC may take the position that it can normalize rates more slowly. At the same time, with the Fed now one year into its balance sheet rewinding, now allowing some $40 billion of Treasury and agency securities to roll off each month, it may have a greater ability to influence long-term rates.

On the other hand, the bond market may be exerting downward pressure on long-term rates because of concerns about a slowdown in economic activity tied to the increasing risk of a trade war between the U.S. and its major trading partners over the imposition of tariffs by the Trump administration. Until this push-pull on interest rates is reconciled – for example, by the U.S. striking new deals to avoid trade wars – the risk of inverting the yield curve may remain elevated. If so, straight Treasurys may be a better investment in the near term.

July 7, 2018

Stephen P. Percoco

Lark Research

839 Dewitt Street

Linden, New Jersey 07036 (908) 448-2246

[email protected]

1 See https://www.nytimes.com/2018/06/25/business/what-is-yield-curve-recession-prediction.html and https://www.frbsf.org/economic-research/files/el2018-07.pdf (cited in the New York Times article).

Read more commentaries by Lark Research