For much of this recovery and expansion, many have opined that this economic cycle would ultimately end very differently than those of the past. We have resisted this narrative and instead explained our belief that this cycle will indeed follow the same path and end like all others. We contend that it is just taking longer to get to each of those “milestone points” along this path because the scars of the Great Recession were deep. As a result, both business owners and consumers have behaved more moderately and, from a political perspective, every action was focused on making the world safer. Now these scars appear to be healing. With another quarter in the books, we believe the preponderance of the evidence points to a U.S. economy that is pushing down a familiar path that is similar to those of the past.

Indeed, the biggest “abnormality” those who believe this time is different have evidenced is that inflation has remained constrained. We believe this narrative is changing and looking more normal. Indeed, during the second quarter, the U.S. Core Personal Consumption Expenditures Price Index hit the Federal Reserve’s 2-percent target for the first time since 2012. And we believe that forward-looking measures of inflation continue to point higher as economic growth strengthens. While these rising inflationary pressures will be a growing risk, we continue to believe that the Federal Reserve will act with a velvet touch regarding interest rate hikes.

Economic Growth is Finally Broadening

Real time economic indicators continue to point to more – not less – economic growth. For many years, the U.S consumer did the heavy lifting while business investments and the manufacturing sector were lackluster. That is no longer the case. Indeed, the Institute for Supply Management (ISM) Manufacturing Index continues to post robust readings. Importantly, much of this optimism is being generated by new orders entering factories, which historically are leading indicators of continued future economic growth. June 2018 marked the 14th straight month (and 17th out of the past 18 months) that new orders were above 60. A reading above 50 means expansion, with a reading above 60 denoting robust expansion. A review of history reveals that this level of new order growth often occurs near the beginning of an economic cycle, not at the end of a cycle or, worse yet, right before a recession.

Economic optimism has also broadened to include “Main Street America” and small business owners. During the quarter, the National Federation of Independent Business Owners Index hit its second highest level in its 45-year history, with the only higher print occurring in 1983. Interestingly, another variable that many use as evidence of the new normal is that wage growth has remained lackluster. We note that in this report, actual compensation hit a 45-year high, with similar record highs made on earnings and expansion plans.

We believe this cycle is progressing along a path similar to those of the past, but at a slower cadence. And given our belief that recessions cause market declines, we paint a picture of continued economic growth and positive market returns.

Are Market Indicators Normal?

With economic growth and inflation looking more normal by the quarter, those who believe this cycle is different and that we are on the precipice of a recession have switched to using market indicators to support their belief. Specifically, the difference between the yield on the 10-Year U.S. Treasury less a 2-Year U.S. Treasury has become their barometer, given that it has historically inverted before all recessions in the recent past. With this spread falling from 0.47 percent at the beginning of the quarter to 0.33 percent at the end, many believe this is signaling an impending recession. While we pay heed to this indicator, we note that a healthy dosage of context is needed with any yield curve comments.

Over the past few years, the world’s most influential central banks (the U.S. Federal Reserve, European Central Bank, Bank of England and Bank of Japan) have bought numerous longer-term government bonds with an expressed intent of pushing longer rates lower. Their actions have likely distorted longer-term yields. Now these central banks are at various points on the path to ceasing their long bond buying at a time when bond supply both here and abroad will likely be ticking higher. As we move from artificial buyers (central bankers) to real buyers (investors), we ponder whether real buyers will demand a higher real return for the longer-term uncertainty risks they bear.

Ironically, we note that yield curve flattening is a “normal” part of the economic cycle, but one that can take years to complete. For example, during the rate hike cycle that began in 1994, the yield curve initially flattened rapidly as the Federal Reserve hiked rates. A mere 10 months into that rate hike cycle, the difference between the 10-Year and the 2-Year U.S. Treasury was a meager 0.085 percent. When economic growth continued and the Federal Reserve fine-tuned by cutting them in 1995 and early 1996, the yield curve never actually inverted but stayed largely in a low range between 0 and 0.75 percent. After a brief inversion in mid-1998 during the Asian Currency Crisis, the yield curve returned to positive levels until it finally inverted on a more prolonged basis in February 2000. A recession did follow, but not until March 2001.

We believe that this Federal Reserve is going to act much like its brethren of the 1990s; if the yield curve continues to narrow, it will likely adjust by slowing down rate hikes. Indeed, many Federal Reserve officials have recently stated that they are paying heed to this indicator and have no desire to knowingly invert the yield curve by hiking short-term rates too aggressively.

Trade Policy Difference?

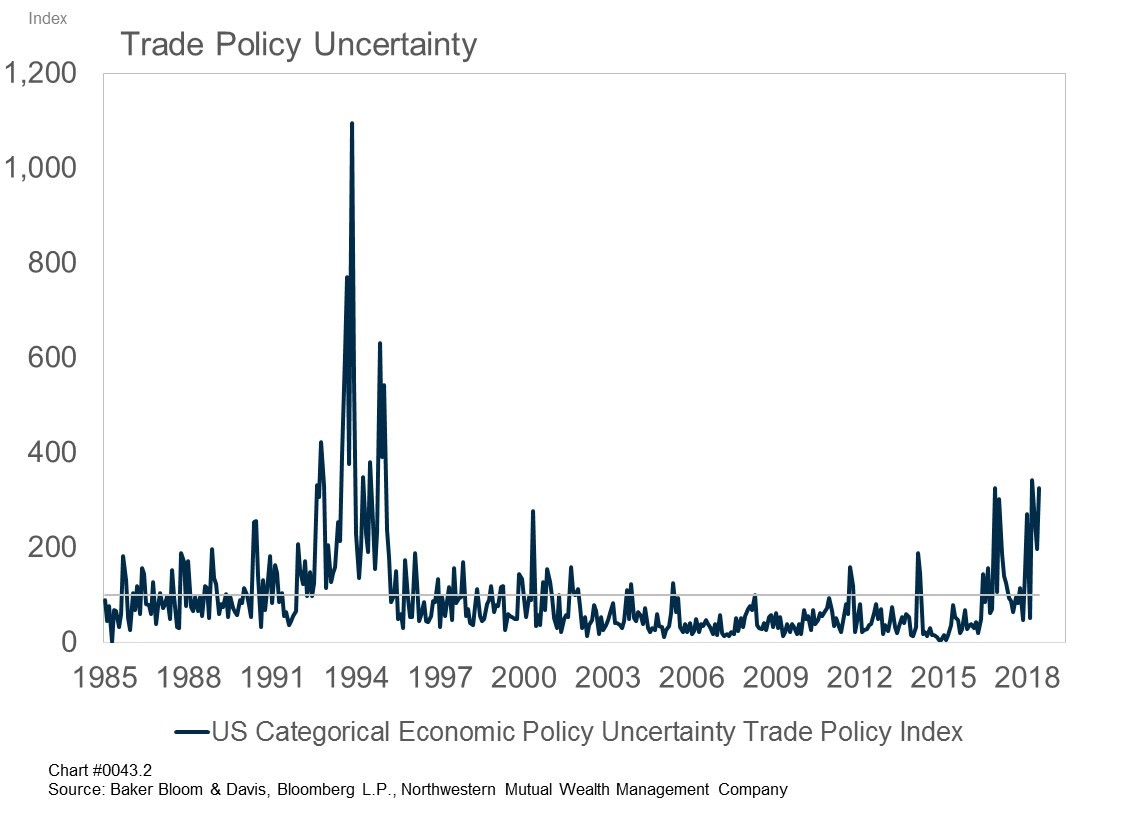

What feels different about this cycle is the potential for a trade war. However, we note that in the late 1980s and early 1990s, the U.S. was similarly fixated on addressing its large trade deficit, especially with regard to Japan. A review of an index designed to capture uncertainty shows that in the early 1990s trade was a big economic and market concern. The U.S. Economic Policy Uncertainty Index is created by combing through major newspapers and finding references to economic uncertainty. One of the uncertainty subcomponents of the overall index is trade policy uncertainty. While this index is rising, it remains below levels registered in the early 1990s. And while it is impossible to draw cause and effect conclusions from one variable, we note that trade uncertainty did not cause a U.S. recession then.

We continue to believe that trade uncertainty and tariffs are not yet causing a significant enough headwind to offset the strong underlying U.S. macroeconomic fundamentals. Rather, we believe trade is a microeconomic issue, or one that creates company-specific winners and losers. Importantly, we believe that this negotiation will ultimately lead to a new intermediate-term path forward.

However, if tariffs continue to grow, we worry that corporations could become dissuaded from investing in plants, property and equipment. Business fixed investment is the lubricant of workforce productivity over the intermediate to longer term, and productivity growth is key to expanding our future standard of living. Ironically, these tariffs are being implemented opposite tax reform, which we believe will ultimately be ranked as a success or failure based upon its ability to nudge business owners to invest. If productivity expands, not only will our future growth rate be higher, but we note that this economic cycle could last longer than current forecasts.

Emerging Markets and the Economic Cycle

While U.S. stocks pushed higher during the quarter, the rest of the world struggled. This was especially true of emerging market equities, which fell nearly 8 percent during the quarter. A simple math exercise points to any trade war effects being greater for countries (China and other emerging economies) that are much more reliant on export growth than the United States. However, we note that at this point in a “normal cycle,” emerging market stocks are often sold off on concerns that are central bank driven.

For the first time in many years, the Federal Reserve has become slightly more hawkish, and many investors are worried that they will tighten rates at an overly aggressive pace. Much like other instances in past economic cycles, this has led to nearer-term dollar strength, which has pressured many emerging market currencies and caused worried investors to retreat from emerging markets’ stocks and bonds. This has led many emerging market central banks to begin raising interest rates in a bid to make their interest rates more attractive and keep investor money from fleeing their borders, and the story completes that these rate hikes will eventually slow these economies to a halt.

Allow us to disagree. We note that while some emerging market central banks have raised rates, they are still historically very low. And while the Federal Reserve is likely to continue tightening, we don’t believe it or any other major central bank are in any hurry to slam the brakes on economic growth. Rather, we believe that global economic growth will continue over the coming years and emerging market equities will eventually be pulled higher with it. Indeed, this was the path for emerging market equities in the past two tightening cycles. They initially sold off on rate hike concerns but ultimately pushed higher as economic growth continued.

Avoid the urge to become protectionist in your portfolio. We believe international and emerging market equities still provide opportunities for patient intermediate- to longer-term focused investors as the economic cycle continues to tick along the path to normal.

Disclosures

This commentary was prepared specifically for your wealth management advisor by Northwestern Mutual Wealth Management Company®. Northwestern Mutual is the marketing name for The Northwestern Mutual Life Insurance Company, Milwaukee, WI (NM) (life and disability insurance, annuities and life insurance with long-term care benefits) and its subsidiaries. Northwestern Mutual Wealth Management Company®, Milwaukee, WI, (investment management, trust services, and fee-based financial planning) subsidiary of NM, limited purpose federal savings bank. Northwestern Mutual Investment Services, LLC, (securities) subsidiary of NM, broker-dealer, registered investment adviser, member FINRA and SIPC.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. Indexes and/or benchmarks are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance and are not indicative of any specific investment. Diversification and strategic asset allocation do not assure profit or protect against loss. Although stocks have historically outperformed bonds, they also have historically been more volatile. Investors should carefully consider their ability to invest during volatile periods in the market. The securities of small capitalization companies are subject to higher volatility than larger, more established companies and may be less liquid. With fixed income securities, such as bonds, interest rates and bond prices tend to move in opposite directions. When interest rates fall, bond prices typically rise; and conversely, when interest rates rise, bond prices typically fall. This also holds true for bond mutual funds. When interest rates are at low levels, there is risk that a sustained rise in interest rates may cause losses to the price of bonds or market value of bond funds that you own. At maturity, however, the issuer of the bond is obligated to return the principal to the investor. The longer the maturity of a bond or of bonds held in a bond fund, the greater the degree of a price or market value change resulting from a change in interest rates (also known as duration risk). Bond funds continuously replace the bonds they hold as they mature and thus do not usually have maturity dates and are not obligated to return the investor’s principal. Additionally, high-yield bonds and bond funds that invest in high-yield bonds present greater credit risk than investment-grade bonds. Bond and bond fund investors should carefully consider risks such as interest rate risk, credit risk, liquidity risk and inflation risk before investing in a particular bond or bond fund.

The 10-year Treasury Note Rate is the yield on U.S. Government-issued 10-year debt.

The Personal Consumption Expenditures Price Index (PCEPI), also referred to as the PCE deflator, PCE price deflator or the Implicit Price Deflator for Personal Consumption Expenditures (IPD for PCE) by the BEA, and as the Chain-type Price Index for Personal Consumption Expenditures (CTPIPCE) by the FOMC, is a United States-wide indicator of the average increase in prices for all domestic personal consumption. Core PCE indicates prices for domestic personal consumption minus food and energy.

The Institute for Supply Management (ISM) is a not-for-profit U.S. association for the benefit of the purchasing and supply management profession, particularly in the areas of education and research.

The ISM Manufacturing Index tracks the amount of manufacturing activity that occurred in the previous month by surveying more than 300 manufacturing firms and monitoring employment, production inventories, new orders and supplier devices.

The National Federation of Independent Business is a small business association representing small and independent businesses. A nonprofit, nonpartisan organization founded in 1943, NFIB represents the consensus views of its members in Washington and all 50 state capitals.

The National Federation of Independent Business Index is a monthly business outlook survey of small and independent business owners who are members of the NFIB.

The European Central Bank (ECB) is the central bank responsible for the monetary system of the European Union (EU) and the euro currency.

The Bank of England (BOE) is the central bank of the UK.

The Bank of Japan (BOJ) is the central bank of Japan.

The United States Economic Policy Uncertainty Index measures market-related economic uncertainty through an analysis of news articles containing terms in three categories pertaining to the economy, uncertainty and the stock market.

Northwestern Mutual is the marketing name for The Northwestern Mutual Life Insurance Company and its subsidiaries. Life and disability insurance, annuities, and life insurance with long-term care benefits are issued by The Northwestern Mutual Life Insurance Company, Milwaukee, WI (NM). Long-term care insurance is issued by Northwestern Long Term Care Insurance Company, Milwaukee, WI, (NLTC) a subsidiary of NM. Securities are offered through Northwestern Mutual Investment Services, LLC, (NMIS) a subsidiary of NM, broker-dealer, registered investment adviser, member FINRA and SIPC. Fiduciary and fee-based financial planning services are offered through Northwestern Mutual Wealth Management Company® (NMWMC), Milwaukee, WI, a subsidiary of NM and a federal savings bank. Products and services referenced are offered and sold only by appropriately appointed and licensed entities and financial advisors. Not all products and services are available in all states. Not all Northwestern Mutual representatives are advisors. Only those representatives with the titles "Financial Advisor" or "Wealth Management Advisor" are credentialed as NMWMC representatives to provide advisory services.

© 2018 The Northwestern Mutual Life Insurance Company

© Northwestern Mutual Wealth Management

Read more commentaries by Northwestern Mutual Wealth Management