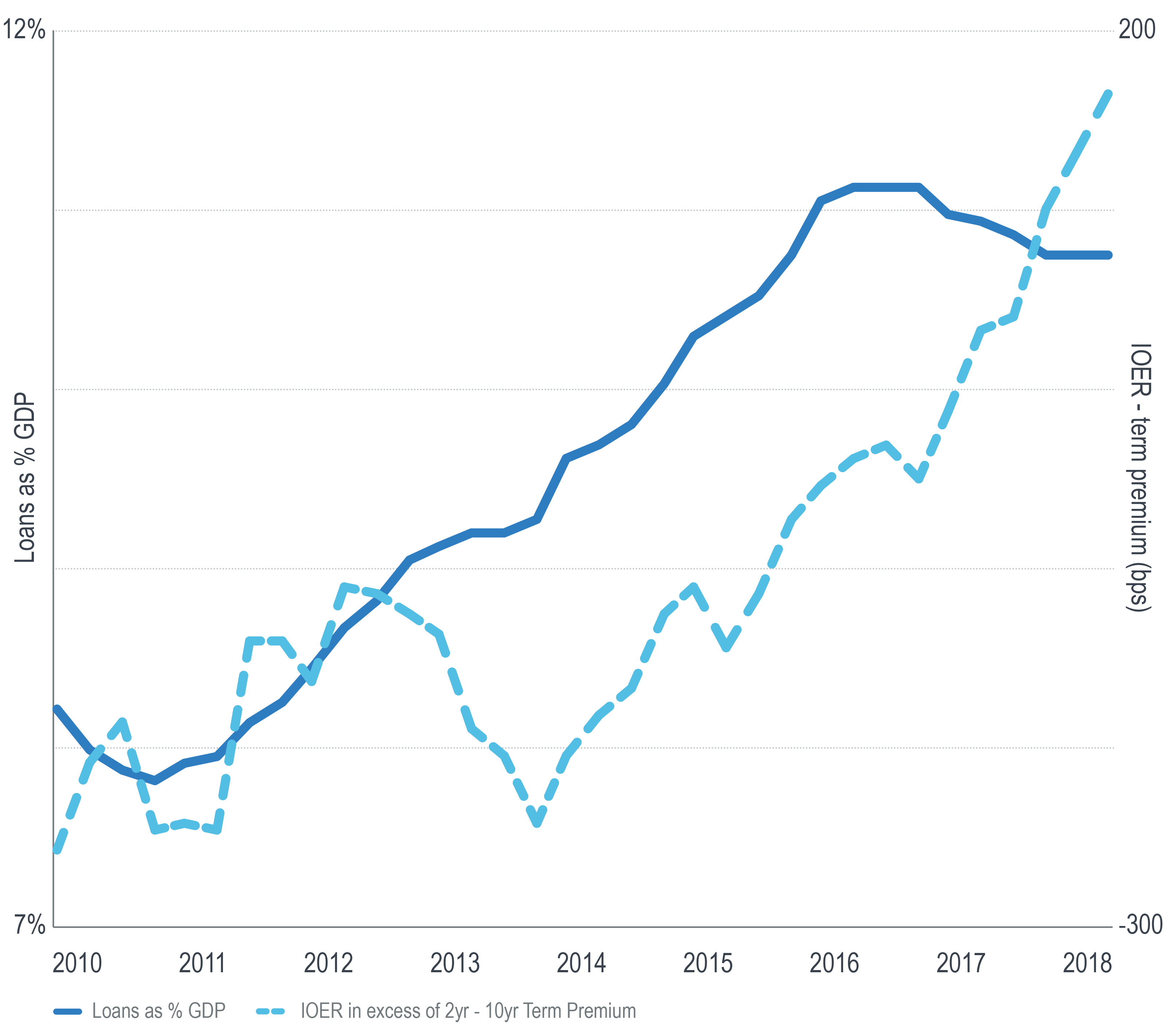

Loan Growth Has Slowed as IOER Has Risen.

The dark blue line tracks the amount of US commercial and industrial loans as a % of GDP. After rising from 2011 into 2016, the amount leveled off and has begun to trend downward.

Loans as a % of GDP is a noteworthy indicator because bank loans, within the context of a fractional reserve banking system, are the means by which the economy’s money is multiplied.

Bank lending is of course a function of the amount of profit a loan will generate, given the amount of risk it entails. The higher this ratio, the more banks will lend.

Day to day, however, banks must adhere to minimum reserve requirements relative to their loans. Any amount above the requirement is considered excess. In the absence of reserve growth, loan growth reduces the amount of excess reserves.

Historically, reserves were acquired through deposits, on which banks paid a short-term interest rate while lending against them at a (higher) longer-term rate. The profit from a loan would be a function of the difference between the short (deposit) and long-term (lending) rate.

However, when the Fed conducted its policy of quantitative easing (QE), it financed its asset purchases by crediting reserves to the banks from whom it was buying. As a result, over the course of three cycles of QE, the banking system amassed more than $2.5 trillion in excess reserves.

In addition to now having no need for deposits and offering depositors virtually nothing for them, banks in the post-crisis era earn Interest On Excess Reserves (IOER, paid by the Fed), and this rate has risen with each of the Fed’s seven rate hikes.

All else equal, higher risk-free IOER makes lending increasingly less attractive. This relationship gains strength as the IOER rate moves higher relative to the longer-term rates banks lend at, which is precisely what has been happening with each Fed rate hike.

Slower loan growth means slower multiplication of money, which in turn means less inflationary pressure. Amidst all the factors generating upward pressure on inflation, this one is arguably pushing back.

Unless otherwise noted, data is sourced from Bloomberg.

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

The results shown are historical, for informational purposes only, and do not guarantee future results.

Any discussion of risks contained herein with respect to any product or service should not be considered a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

Data included in this document has been sourced from providers that Milliman FRM believes to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by Milliman FRM as to the accuracy or completeness of the source data or any other information in this document.

Copyright ® 2011 – 2017 Milliman Financial Risk Management LLC