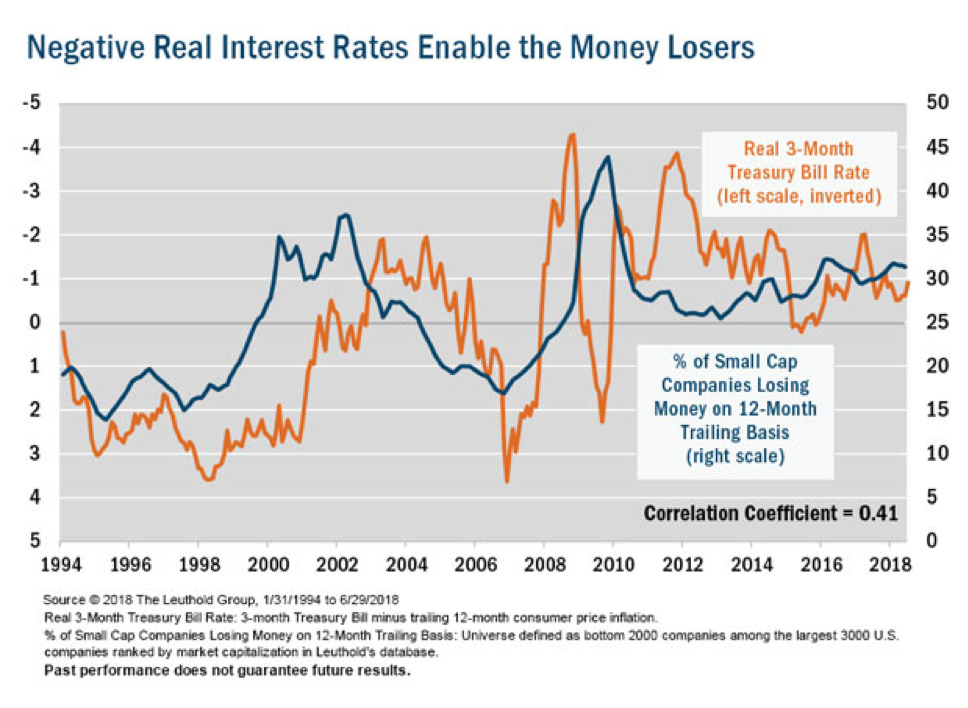

One of the unintended consequences of the Fed’s easy money policy over the past nine years has been a real-world lesson on the law of diminishing returns. As the chart shows, the drop in real rates on the three-month Treasury has coincided with a rise in the percentage of money-losing companies among small caps.

The relationship seems counterintuitive—lower borrowing costs should provide a break to cash-strapped businesses. Instead, many CEOs have viewed lower rates as a green light to borrow more in pursuit of speculative projects, and many have not panned out.

With the 10-year Treasury nudging back above 3% recently, and the London Interbank Offer Rate (LIBOR), which is used to set rates for many commercial loans, jumping more than 100 basis points in the past year, it appears the days of cheap money are winding down. As borrowing costs escalate, some money-losing businesses will no longer be able to subsidize their weak results and will face a day of reckoning as they are forced to pay for underperforming ventures.

We have always viewed strong balance sheets as an important factor when making investment decisions. With corporate debt near a historic peak relative to gross domestic product, we believe this emphasis will prove critical in the coming months.

Disclosure:

Past performance does not guarantee future results.

Investing involves risk, including the potential loss of principal. There is no guarantee that a particular investment strategy will be successful. Value investments are subject to the risk that their intrinsic value may not be recognized by the broad market.

The statements and opinions expressed in this article are those of the presenter. Any discussion of investments and investment strategies represents the presenter’s views as of the date created and are subject to change without notice. The opinions expressed are for general information only and are not intended to provide specific advice or recommendations for any individual. Any forecasts may not prove to be true. Economic predictions are based on estimates and are subject to change.

Small-cap investment strategies, which emphasize the significant growth potential of small companies, have their own unique risks and potential for rewards and may not be suitable for all investors. Small-cap securities are generally more volatile and less liquid than those of larger companies.

Definitions: Basis Point (bps): is a unit that is equal to 1/100th of 1% and is used to denote the change in a financial instrument. Consumer Price Inflation: is the rate at which the prices of goods and services bought by households rise and fall; it is estimated using consumer price indices. Correlation Coefficient: is a number between 0 and 1. If there is no relationship between the predicted values and the actual values, the correlation coefficient is 0 or very low (the predicted values are no better than random numbers). As the strength of the relationship between the predicted values and actual values increases, so does the correlation coefficient. A perfect fit gives a coefficient of 1.0. Thus, the higher the correlation coefficient, the better. London Interbank Offered Rate (LIBOR) is a benchmark rate that some of the world’s leading banks charge each other for short-term loans. It serves as the first step to calculating interest rates on various loans throughout the world. LIBOR is administered by the ICE Benchmark Administration (IBA), and is based on five currencies: U.S. dollar (USD), Euro (EUR), pound sterling (GBP), Japanese yen (JPY) and Swiss franc (CHF), and serves seven different maturities: overnight, one week, and 1, 2, 3, 6 and 12 months. A total of 35 rates are posted every business day with the three-month U.S. dollar rate being the most common. Treasury Bill (T-Bill): is a short-term debt obligation backed by the U.S. government with a maturity of less than one year. T-bills are sold in denominations of $1,000 up to a maximum purchase of $5 million and commonly have maturities of one month (four weeks), three months (13 weeks) or six months (26 weeks). Treasury Note: is a marketable U.S. government debt security with a fixed interest rate and a maturity between one and 10 years.

©2018 Heartland Advisors heartlandadvisors.com

2018694

© Heartland Advisors

Read more commentaries by Heartland Advisors