• Today’s market is barbelled regarding company size, with the mega-cap Tech stocks and the S&P 600 Small Cap index both outperforming the middle of the S&P 500.

• Over the past twenty-five years, this particular type of environment has only occurred in 15% of the months, and it did not play out well in past cycles, surfacing near the end of both the 2000 and 2007 market tops.

• The S&P 500 Equal Weighted index and the S&P 600 Small Cap index are two ways to measure the small company factor and, although they differ in design and risk, their performance has been remarkably similar.

Today’s Barbelled Size Factor

The relative performance of small cap stocks is an important indicator of business fundamentals and market sentiment. We’ve recently noticed that the market has been sending mixed messages about size. Intrigued by these contrary signals, our curiosity prompted a closer look at the all-important size factor.

▪ On one hand, the capitalization-weighted S&P 500 has been outperforming the equal-weighted version. The Social/Mobile/Cloud giants have been powering the market in 2018 suggesting that ‘Large’ is in charge.

▪ On the other hand, the S&P 600 Small Cap index is trouncing the S&P 500. Small Caps are favorably positioned because of their focus on the domestic economy, greater benefits from tax cuts, and higher sensitivity to a strong business cycle, suggesting that ‘Small’ is the place to be.

Capitalization-weighted indexes will outperform their equal-weighted counterparts when Large Caps are winning, and the equal-weighted version will dominate when the rank-and-file stock is beating the mega caps. Many investors watch this relationship as a straightforward indicator of the size factor; since both renditions of the index own the exact same names the only difference is the influence of market cap. Comparing the S&P 500 to the S&P 600 (or Russell 2000) is another way to track the size factor but this relationship involves two completely different groups of companies and sets of sector weights, requiring an additional layer of analysis to sort out the main drivers of relative returns.

Two Methods, Similar Results…

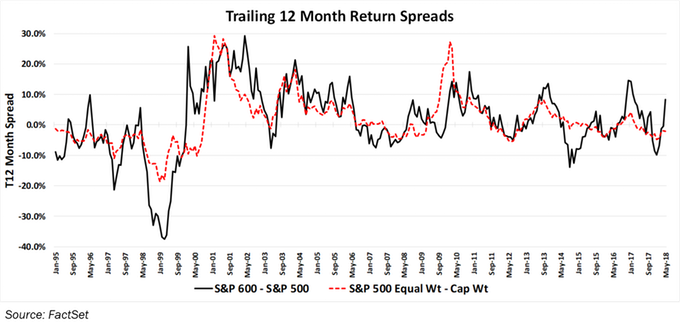

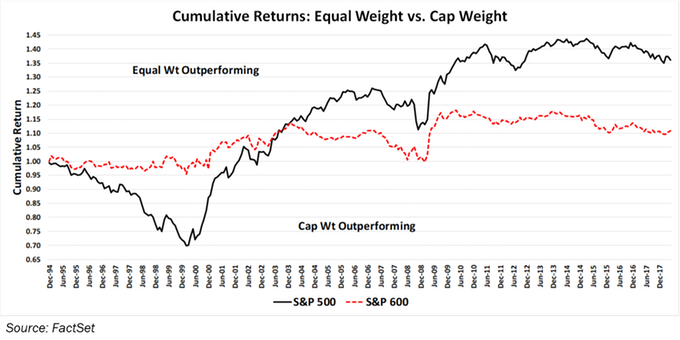

While these two approaches differ considerably in their methodologies, we were surprised by the consistent story they tell. Chart 1 shows the trailing 12-month return spreads for (a) the S&P 500 Equal Weighted (EW) index minus the cap weighted (CW) S&P 500, and (b) the S&P 600 Small Cap minus the S&P 500. Our expectation was that the S&P 600 spread would be much wider because it holds completely different companies whereas the S&P 500 EW would reveal a closer fit because it holds the same components as the core S&P. Although the S&P 600 return series reaches more extreme levels at times, the two series track fairly well.

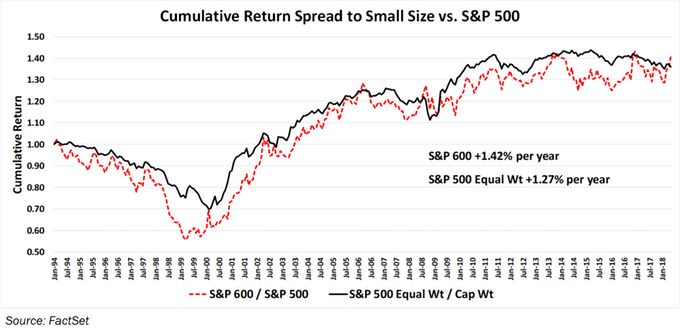

The consistency of these two measures is confirmed in Chart 2, which shows the cumulative spread of each index versus the core S&P 500. Both underperformed going into the Tech bubble but compounded nicely during the next decade; each has trended sideways since 2011. Over this 24-year span, the S&P 600 Small Cap index has outperformed by 1.42% per year while the 500 EW outgained the base S&P 500 by 1.27%.

… But Different Risks

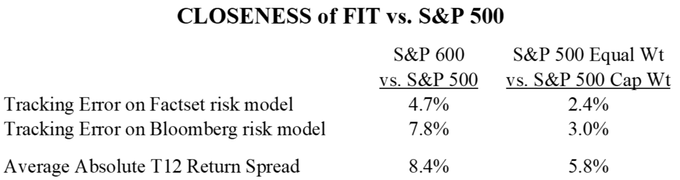

Both approaches have earned similar spreads over time, but the 500 EW gets there in a smoother fashion. Table 1 shows the expected tracking error of each size measure using two different risk models, and both agree that the S&P 500 EW contains much less inherent risk than does the S&P 600. We also calculated the average absolute difference in T12 returns between the 500 EW and 500 CW to be 5.8% compared to 8.4% for the S&P 600.

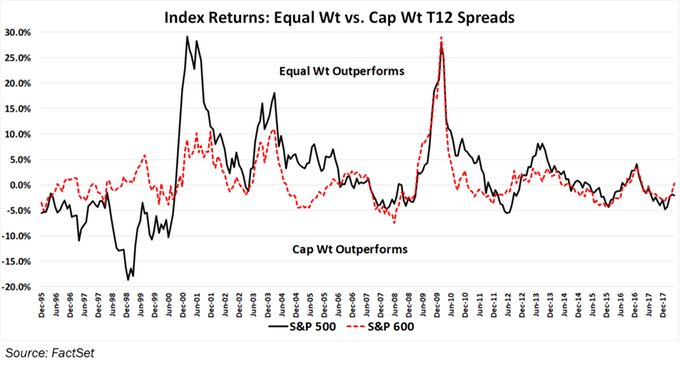

Having been amazed by the robustness of the S&P 500 EW in capturing the size effect, we examined the equally-weighted S&P 600 to see if the result carried over. Chart 3 demonstrates that the EW/CW cycle also impacts small caps, particularly since 2006.

However, Chart 4 suggests that the equal-weighted gains have been much less rewarding for small caps. While the S&P 500 EW outperformed by nearly 40%, the S&P 600 EW gained just 10% over its base index. This is because the S&P 500 is much more top heavy than the 600. The largest company in the S&P 500 averages a capitalization weighting more than 3.1% above its equal-weighted allocation, whereas the largest company in the S&P 600 averages just 0.6% more than it would under equal weighting.

Is The Current “Size Barbell” Unusual?

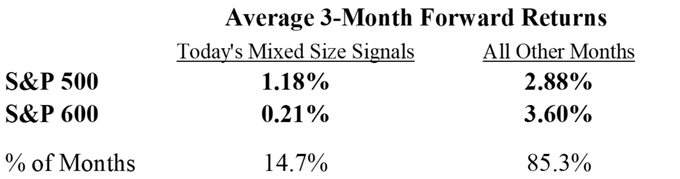

Today we face the peculiar situation where the cap-weighted S&P 500 is beating the S&P 500 EW, while at the same time the S&P 600 is beating the S&P 500. The equity market is barbelled on size, with the Tech giants and small companies both outperforming the core of the S&P 500. Sensing that this odd circumstance had a story to tell, we searched for similar conditions using market data over the last quarter century. Table 2 shows that the mega cap/small cap barbell has appeared in about 15% of the months since 1993. Wondering if this mixed-size signal had anything to say about future market action, we calculated forward three-month returns and the results tell a notably bearish story.

Forward three-month absolute returns, for past instances of the mixed-size signal, were +1.18% for the S&P 500 and +0.21% for the S&P 600. In all other months the three-month forward absolute returns were +2.88% and +3.60%, respectively. Furthermore, we eyeballed the data and found three clusters where the mixed-size combination appeared multiple times:

June 1999 to June 2000

June 2002 to December 2002

March 2007 to September 2008

Market historians will quickly recognize that two of these periods were associated with severe bear markets, and 2002 was no picnic either! The return analysis for those months characterized by the combination of S&P 500 CW and S&P 600 outperformance (like today) is most discomforting.

Adding Some Style To Our Study

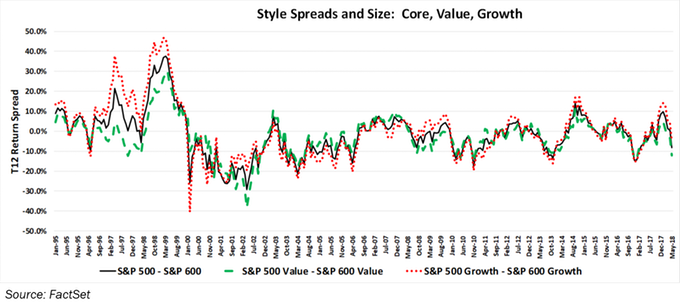

Growth has dominated Value in recent years, and we decided to explore whether the size cycle has any relationship to the style cycle. Our first test was to compare styles across size, i.e., Large Cap Value versus Small Cap Value, and Large Cap Growth versus Small Cap Growth. Chart 5 compares the overall size cycle (S&P 500 minus S&P 600 as the solid line) with the indexes split into their Value and Growth components. We were astonished to see how closely the dashed line (Large Value minus Small Value) and the dotted line (Large Growth minus Small Growth) tracked the overall size cycle. It is clear that the size cycle dominates, and the size decision is easily transferable to investors focused on either the Growth or Value style.

Value/Growth Spreads By Size

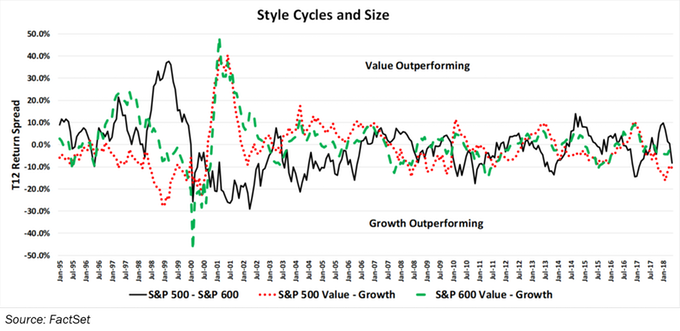

If we shuffle the combinations of size and style to focus on the battle between Value and Growth we see a much different picture, shown in Chart 6. First, we note that the Value minus Growth cycle does not track the size cycle at all, in fact it appears to be a contrary fit more than anything else. Second, we see that the Large Cap and Small Cap Value/Growth cycles generally track one another, but gaps often open, including the last year when Large Value has done much worse relative to Growth than has Small Value.

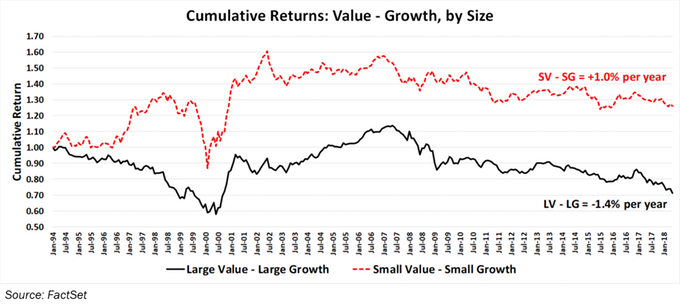

As we detailed in our recent special report, The Value Style’s 100-Year Flood, it has been a rough decade for Value investors regardless of size. Small Value retains the long-term edge on Small Growth in Chart 7, but Large Value is approaching a record relative low. Over the last twelve months, LV trails LG by 10.5% while SV lags SG by just 3.4%. Our 100-Year Flood report details how the Social/Mobile/Cloud Tech giants have accounted for a fair portion of both the size and Growth bias within the S&P 500 over the last few years, a phenomenon having much less impact on Small Caps.

Indexes Are Becoming More “Growthy”

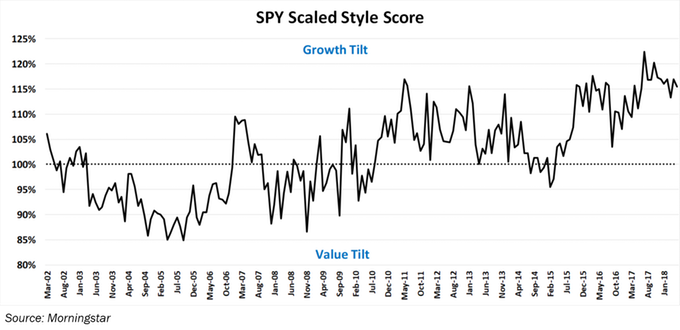

Since the top end of the size barbell (S&P 500 CW beating the S&P 500 EW) appears to be driven by the Social/Mobile/Cloud names that dominate the cap-weighted S&P today, we wrap up this report with a fundamental analysis using the Morningstar style box methodology. To summarize, Morningstar calculates style scores using five value metrics (the most important being P/E on forward earnings), and five growth metrics (the most important being analysts’ long-term growth estimates), rolled into one score. The style score for each index is calculated as the size-weighted average of each stock.

Chart 8 plots the SPY ETF’s style scaled to a neutral Value/Growth reading set to 100, showing the index has become more “growthy” in the last year after registering an all-time high of 22% above neutral in July of 2017. This confirms our suspicion that the cap-weighted S&P 500 has become more heavily- tilted toward expensive Growth companies.

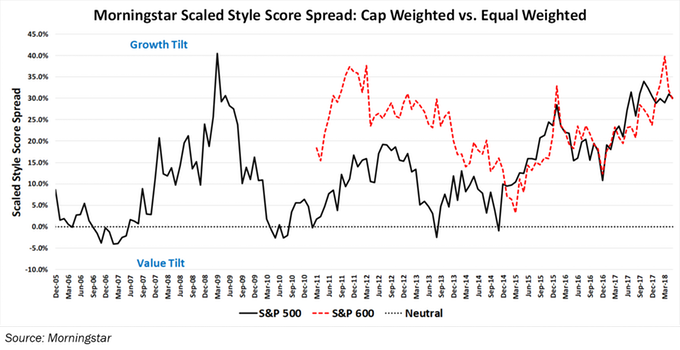

Chart 9 continues the exercise by plotting the difference in scale-style scores between the cap-weighted and equal-weighted versions of S&P 500 and S&P 600 using ETFs. In both the large and small universes, the cap-weighted indexes are now approximately 30% more growthy than their equally-weighted counterparts. It seems clear to us that if the market’s current fascination with Growth stocks begins to fade, the cap-weighted indexes—having a much higher exposure to the Growth style—would suffer disproportionately from a shift to Value.

Research Takeaways:

• The S&P 500 Equal Weighted index and the S&P 600 Small Cap index both capture the Small Cap effect, with ending-wealth approximately 40% higher than the S&P 500. We generally favor the approach of playing size through the S&P 500 EW because it avoids the tracking error introduced by the S&P 600’s different lineup of companies.

• Investors concerned about excess enthusiasm for mega-cap Tech should note that cap-weighted indexes have become much growthier in style relative to equal-weighted indexes, and the latter should offer better protection during a selloff in Social/Mobile/Cloud.

• The size cycle is present in the Value and Growth styles, meaning that style-focused investors should pay attention to the overall trends in size. However, the choice between Value and Growth moves contrary to the size cycle.

• A barbelled size effect has appeared most often in periods when the S&P 500 experienced significant bear market selloffs, and overall returns in this environment are well below those earned during other market conditions.

© 2018 The Leuthold Group

www.leutholdfunds.com

Read more commentaries by The Leuthold Group