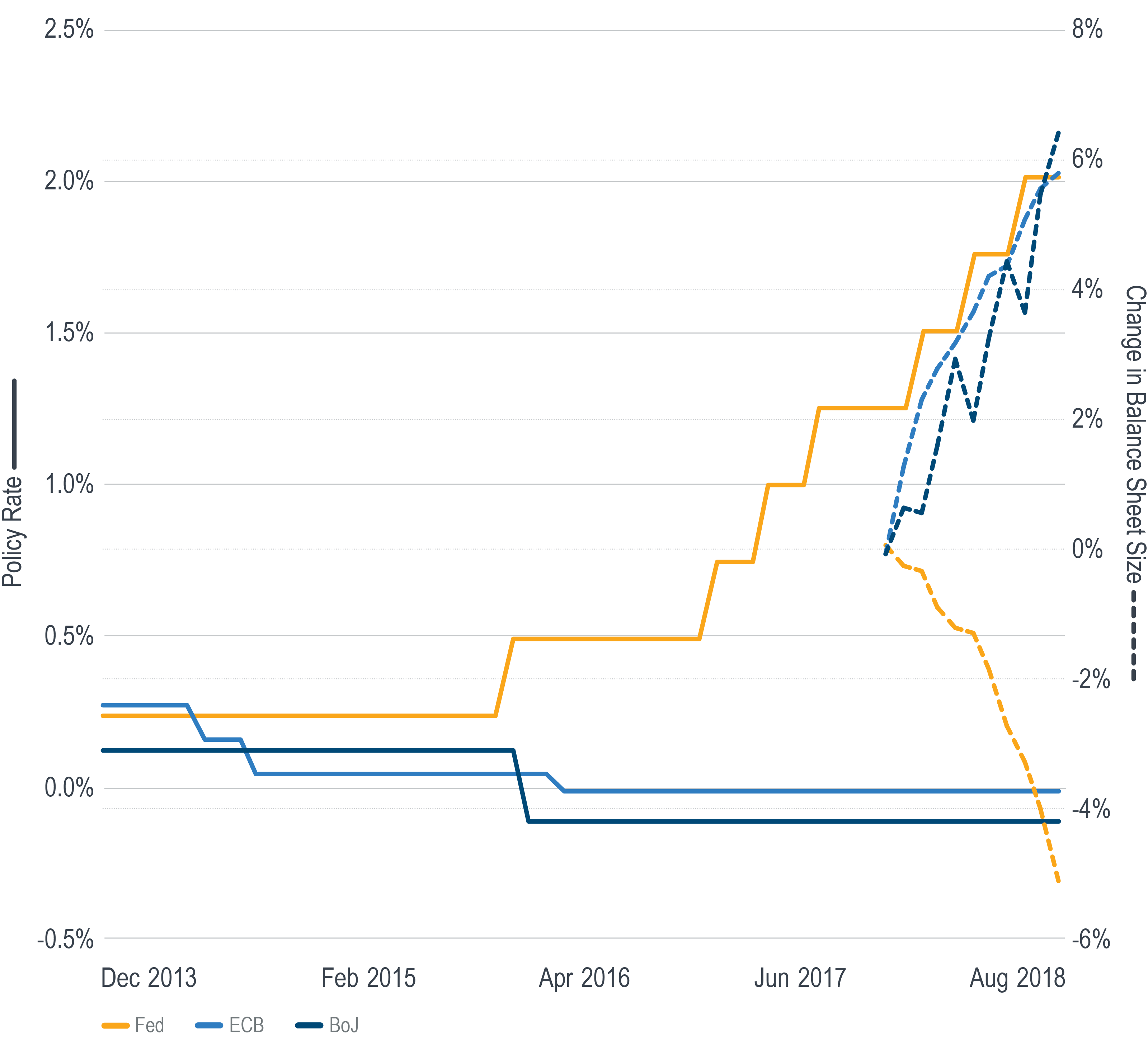

The monetary policies of the world’s three largest central banks have been diverging for more than two years.

After leaving its fed funds rate unchanged at 25 bps for seven years, the Fed made its first rate hike in 2016. That same year, the European Central Bank (ECB) and Bank of Japan (BoJ) cut their rates further.

Since then, the Fed has made six more rate hikes with another one coming later this month, while the other two banks have left their rates unchanged.

In October 2017 the Fed formally began its balance sheet normalization process, wherein they began to let bonds mature without reinvesting the principle. Since then, its balance sheet has shrunk by about 5% (dotted line).

Meanwhile, as the Fed has been shedding assets from its balance sheet, the ECB and BoJ have been adding assets to theirs. Since October 2017, both their balance sheets have grown by about 6%.

Conventional wisdom says that tighter monetary policy generally causes the currency to strengthen. And yet, in spite of the policy divergence in both rates and balance sheets, the dollar is flat against the euro and down 2% against the yen.

What are investors to make of this?

If there’s anything to be gleaned from this, it may be that such massive central bank intervention can distort the economic and financial environment in ways that are hard to comprehend. If that’s true, it has implications for investors’ perceptions of uncertainty and risk.

Unless otherwise noted, data is sourced from Bloomberg.

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

The results shown are historical, for informational purposes only, and do not guarantee future results.

Any discussion of risks contained herein with respect to any product or service should not be considered a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

Data included in this document has been sourced from providers that Milliman FRM believes to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by Milliman FRM as to the accuracy or completeness of the source data or any other information in this document.