The Phillips Curve (the relationship between wages and the unemployment rate) finally awoke from its slumber with today’s unemployment report showing private sector wages rising 2.9% year-over-year and non-supervisory wages rising 2.8% year-over-year, the fastest growth rate since 2009. Even more important than that, though, is that all indications continue to point to even faster wage growth in the months and quarters ahead. Below are five important indicators, some with a leading relationship with wages, that all suggest faster wage growth, and an even tighter labor market is in the offing.

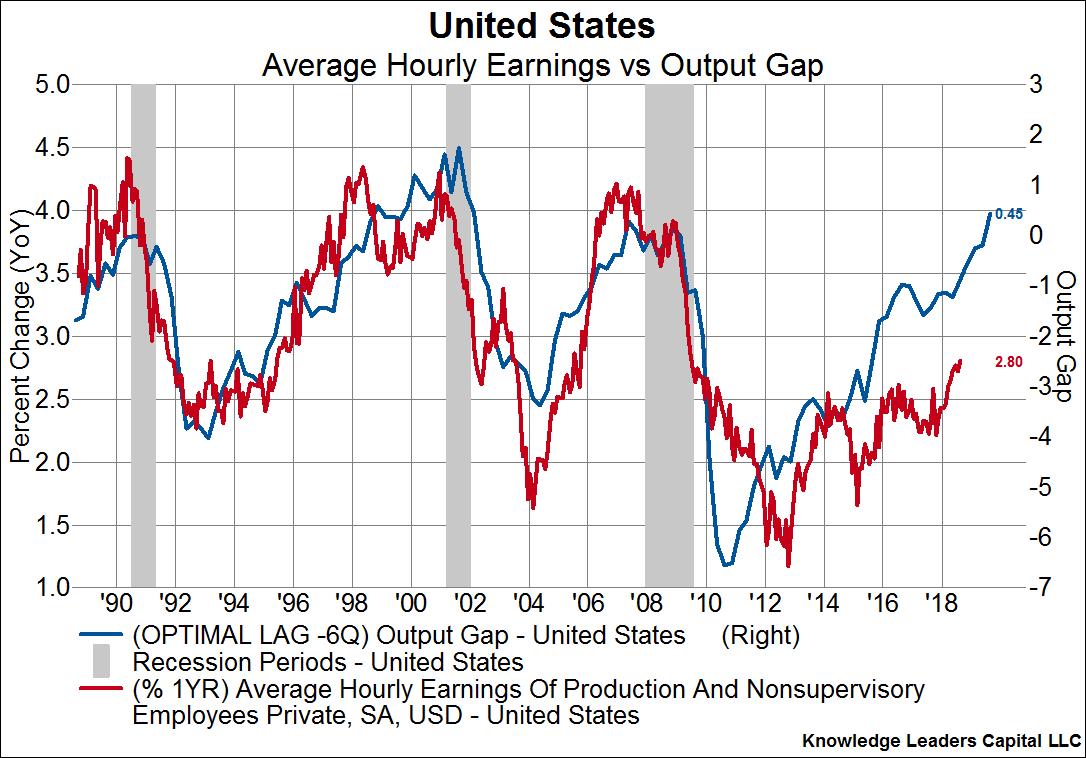

The output gap. The output gap is the difference between actual economic growth and longer-term potential growth of an economy. A positive output gap, like we have now, indicates the economy is growing faster than can be sustained without inducing pricing and wage pressures. The output gap leads wage growth by about six quarters and suggests wage growth in the mid-3% range in the near future.

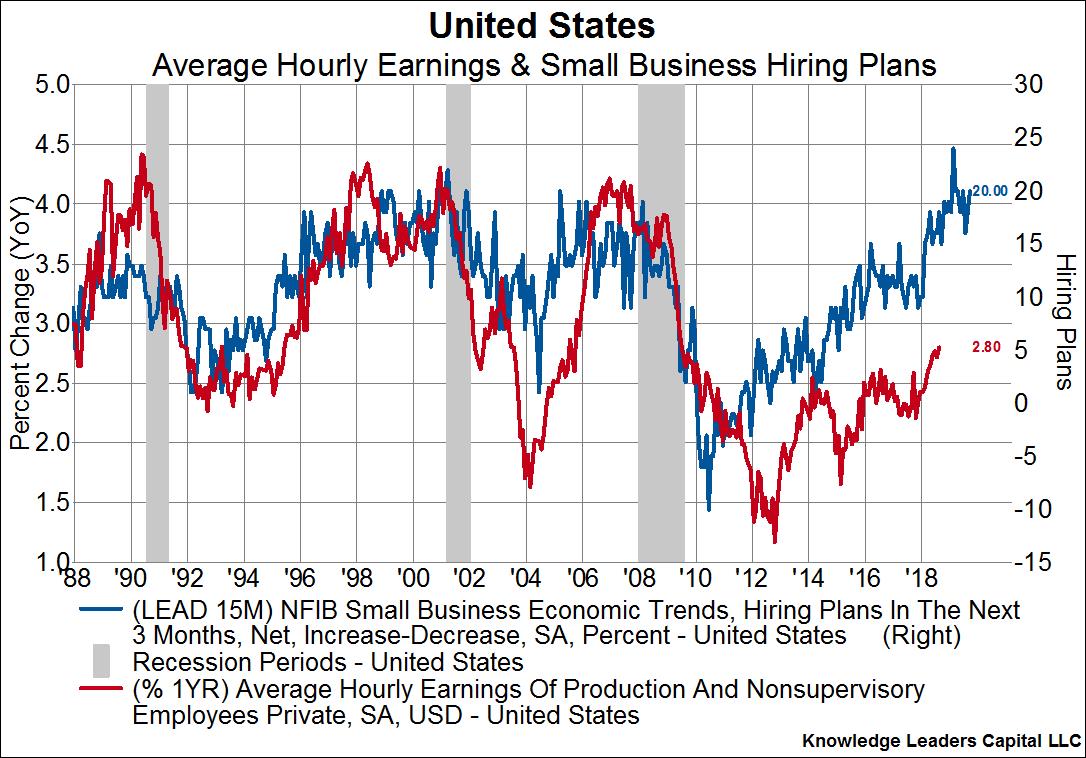

Small business hiring plans. Small business hiring is normally the driver of aggregate employment and small businesses are telling us they plan to add employees within the next three months. This type of behavior is normally positive for wages, ditto when the unemployment rate is 3.9% and those small businesses have to complete for workers. Small business hiring plans lead wage growth by 15 months and also suggest wage growth in the mid-3% range.

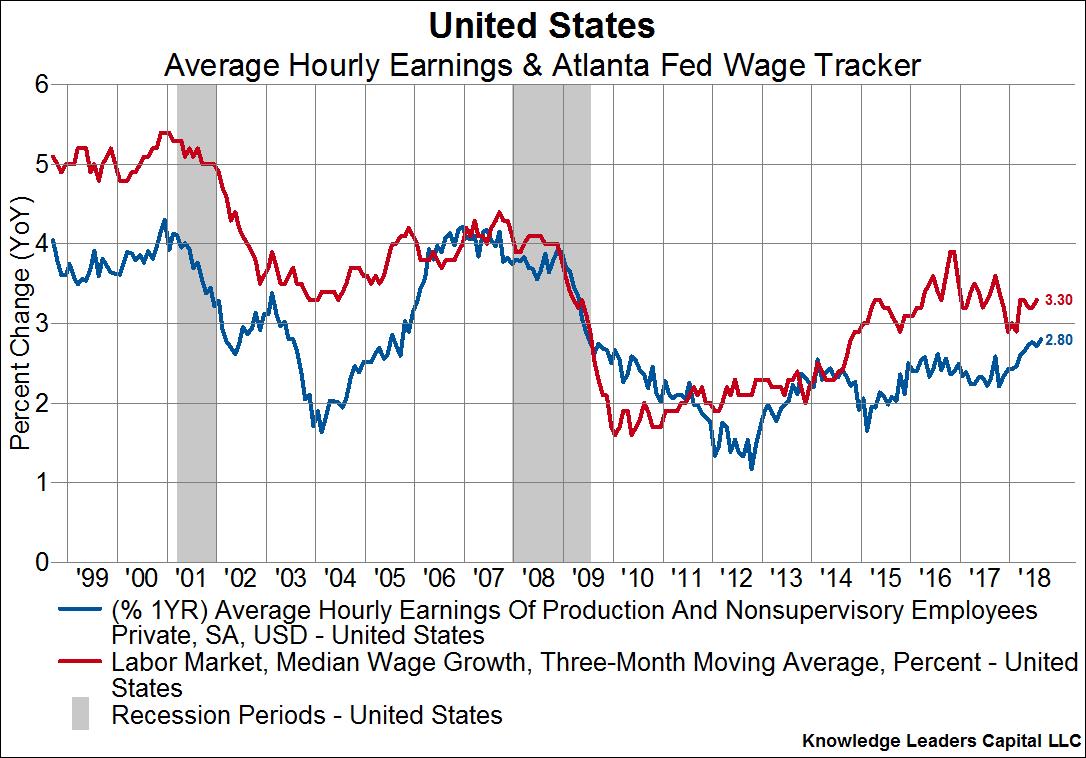

Atlanta Fed Wage Tracker. The Atlanta Fed distributes a measure of median wage growth derived from the Bureau of Labor Statistics survey data. It has a close relationship with aggregate wages and is not only running faster than aggregate wages (3.3% vs 2.8%), but has also turned up since the beginning of the year.

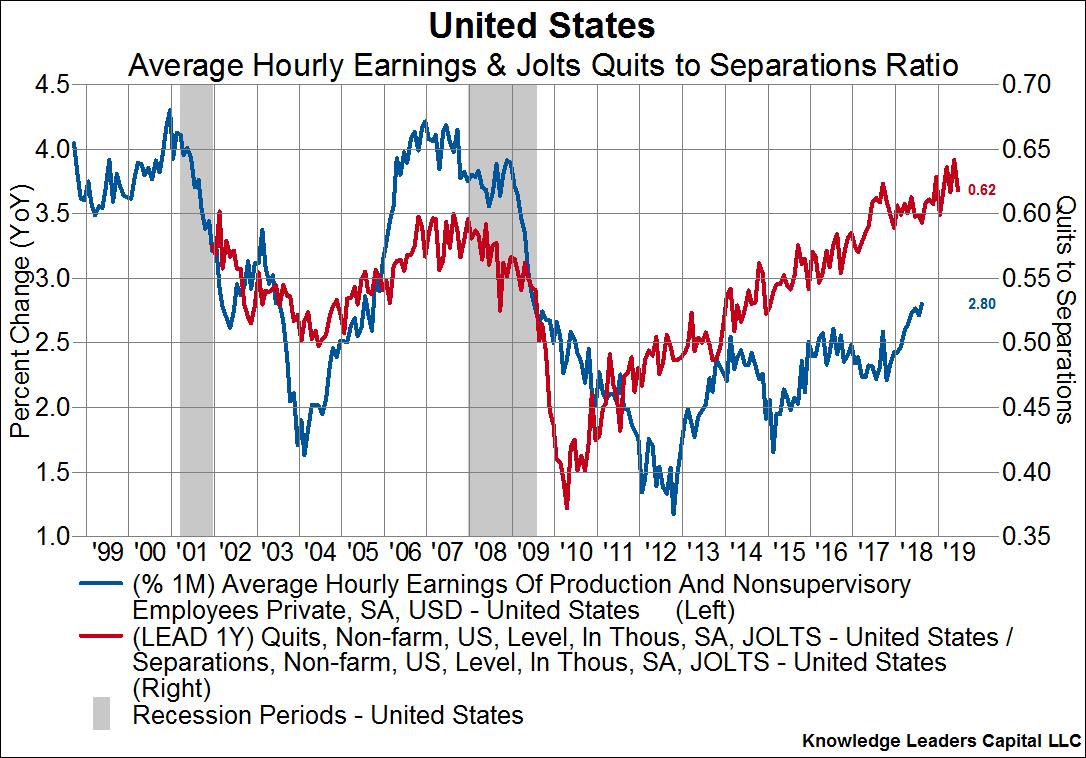

JOLTS quits to separations ratio. The Job Openings and Labor Turnover Survey (JOLTS) has sub-components that include the number of people quitting a job voluntarily and the total number of separations (voluntary quits plus terminations). It stands to reason that as the percent of voluntary quits as a percent of total separations rises, wages should also rise, since people generally only leave their current job for a better paying job. And indeed that is the case when we compare wages to the quits to separations ratio. In fact, the quits to separations ratio leads wage growth by about a year and it currently suggests we are in for another year of upward wage pressure.

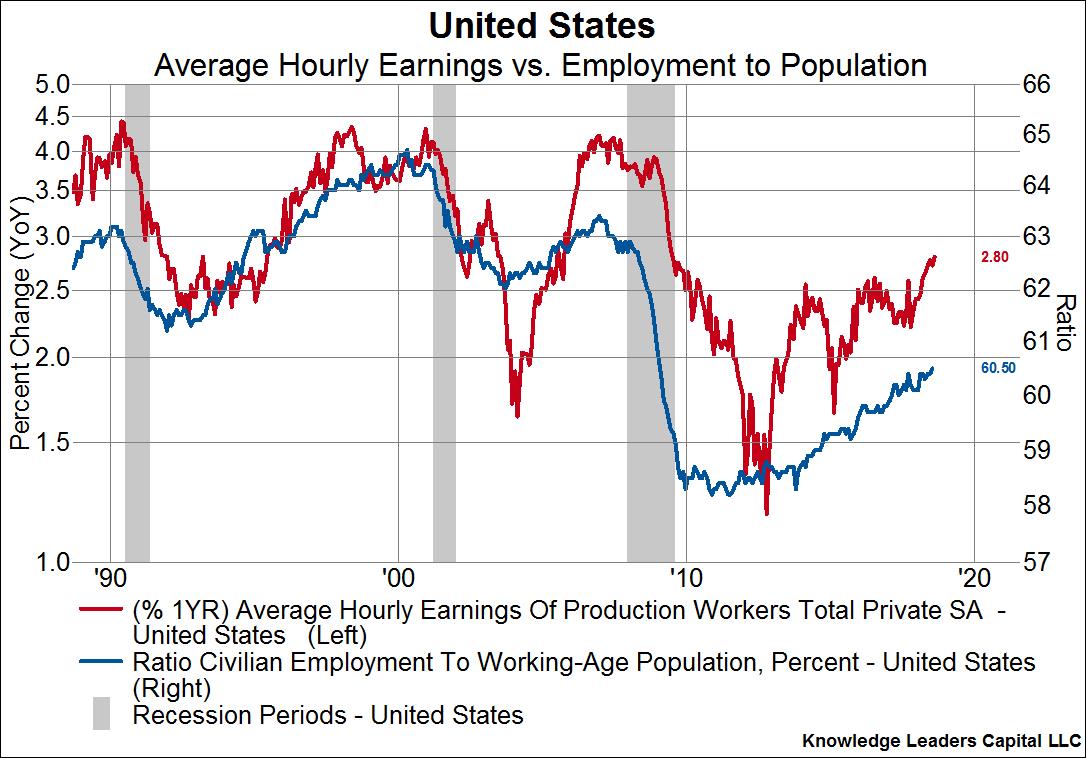

The employment to population ratio. The employment to population ratio is not only low compared to history, but it is rising steadily. While it’s unlikely that the employment to population ratio will reach previous cycle heights due to structural factors (financial crisis, opioid crisis, the AI revolution), it does not look to be peaking. That is good news for wage growth, since employers are becoming less able to pull from those out of the labor force to fill open positions.

This evidence suggests wage growth is likely to continue for some time, which will have implications for markets and investors. No doubt the Fed is paying attention to wage growth, and this latest reading will keep the pressure on to continue its path of rate increases, a condition that would have its own set of reactions. At the same time, if wage growth is driven by productivity gains, then potential output may expand in lock step, which would allow for Fed hikes without breaching the all important neutral level. In any case, look for future wage growth to coincide with a more hawkish Fed, and everything that comes with it.

© Knowledge Leaders Capital

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital