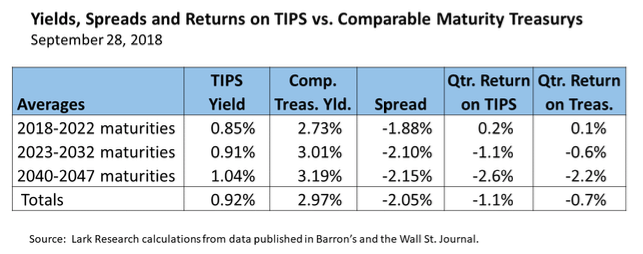

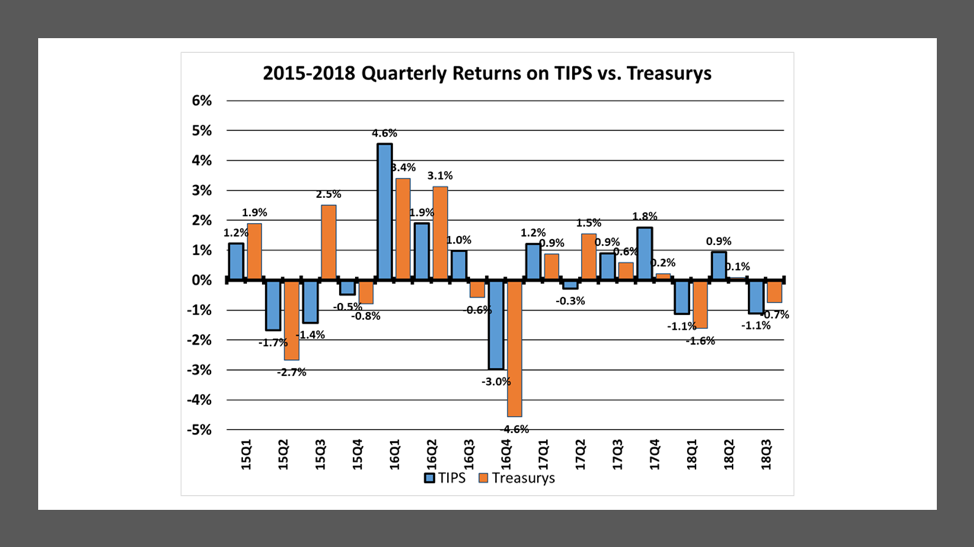

As interest rates marched higher, TIPS underperformed comparable maturity straight Treasurys for the first time in five quarters. On average, TIPS lost 1.1% in the third quarter, worse than the 0.7% loss on comparable maturity straight Treasurys. The average yield on TIPS rose by 33 basis points (bp) to 0.92%, compared with the 23 bp increase to 2.97% for Treasurys. As a result, the average spread between straight Treasurys and TIPS yields declined by 10 bp from 215 bp to 205 bp.

The faster rise in TIPS yields and decline in the average spread suggests that inflation expectations moderated slightly during the quarter. Investors sought a higher yield on TIPS to compensate for a lower anticipated inflation adjustment.

As was the case in previous quarters, the returns on longer maturity securities were more volatile. Long-maturity TIPS suffered a 2.6% decline, worse than straight Treasurys 2.2% decline. In contrast, short-maturity TIPS and Treasurys posted slightly positive returns. This range of performance is expected in a rising rate environment.

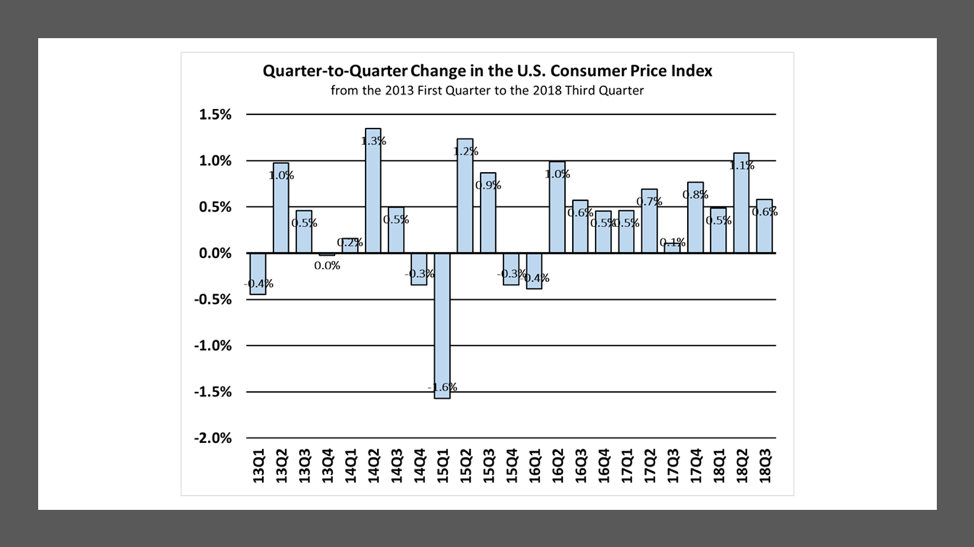

The gain in TIPS from the inflation adjustment eased from the 2018 third quarter. During the 2018 third quarter, the CPI rose by 0.6% year-over-year, less than the 2018 second quarter’s 1.1% gain. The CPI had been rising progressively faster pace for most of 2018, but August saw a lower increase in both the headline and core CPI. Headline CPI eased from 2.95% in July to 2.70% in August and core CPI (excluding food and energy) eased from 2.35% to 2.20%. With the 17% increase in the price of oil since mid-August and the 12% increase in the price of natural gas since early September, it is a fair bet that headline CPI will rise at a modestly faster pace in the months ahead.

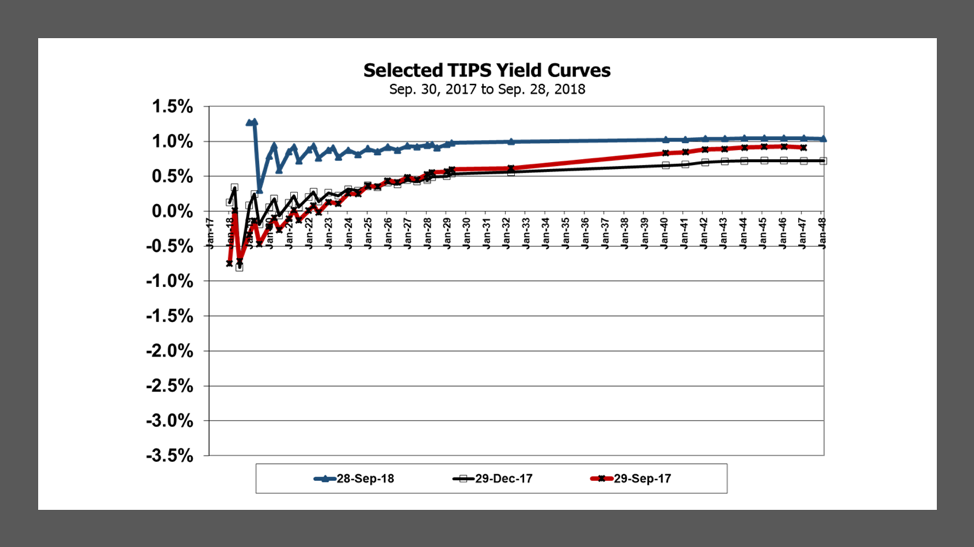

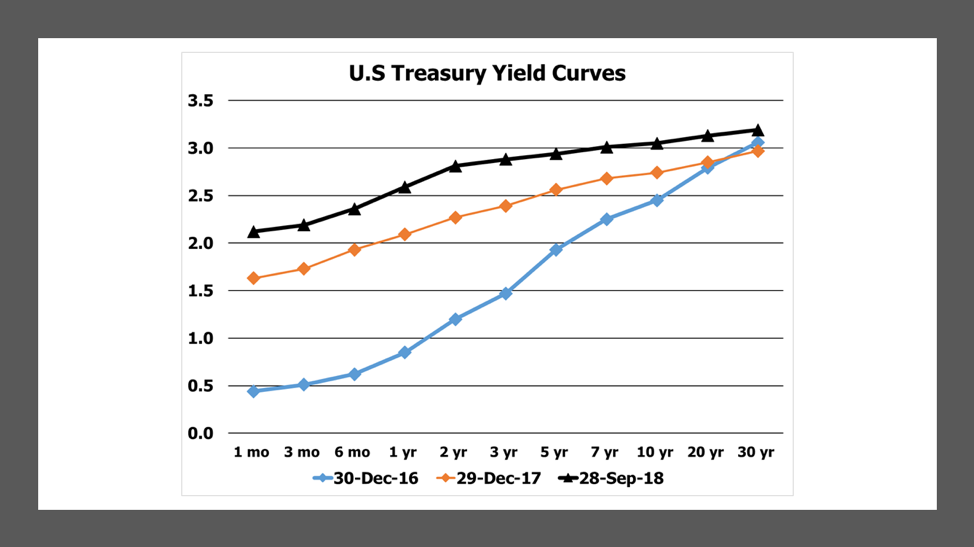

Like straight Treasurys, the US TIPS yield curve has flattened modestly in 2018, as short-term TIPS yields have risen at a faster pace. The change in the third quarter yield curve was slightly more balanced than in previous quarters, with shorter maturities of both TIPS and Treasurys rising about 25 bp and longer maturities rising about 20 bp.

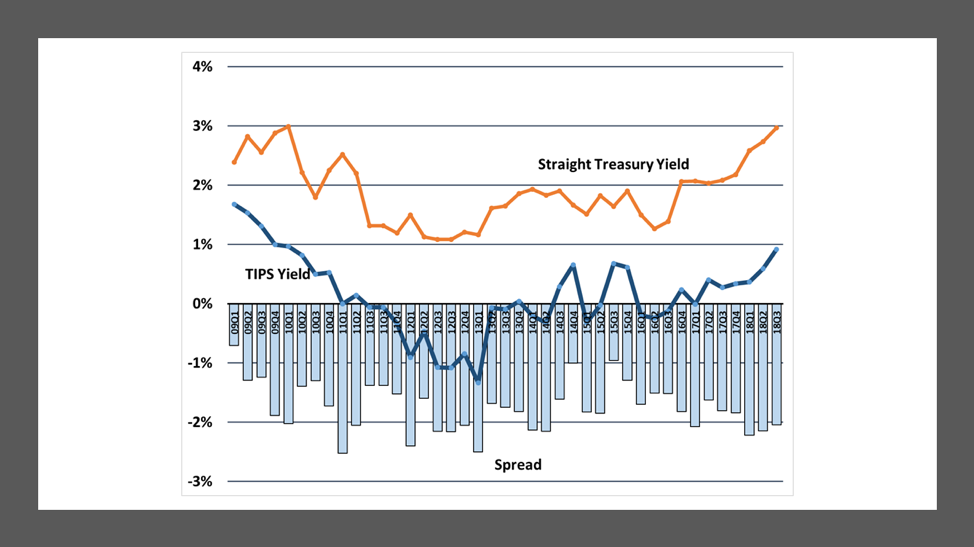

The average yield spread between straight Treasurys and TIPS narrowed during the quarter by 10 bp from 215 bp to 205 bp, still above the long-term average of 175 bp. The average TIPS and comparable maturity Treasury yields of 0.92% and 2.97%, respectively, are back to levels last seen in 2009.

The spread between the 10-year U.S. Treasury yield and the 2-year yield has narrowed from 47 bp at the beginning of the year to only 24 bp at the end of September. The rate of flattening has continued at a steady pace throughout the year, with a 9 bp reduction during the third quarter.

At its most recent meeting in September, the Federal Open Market Committee (FOMC) as expected raised the target range for the Fed Funds rate by a quarter basis point to 2.00%-2.25%. In its statement, the FOMC characterized both the economy and the labor market as strong.

Accordingly, most FOMC members anticipate another 25 bp increase in December and as many as three more in 2019, which would bring the target rate above 3.0% in 2019. The “dot plot” table, which indicates the collective assessments of FOMC members, suggests that the targeted Fed Funds rate will essentially stay flat in 2020, but rise about a quarter point in 2021. Longer term, FOMC members see the appropriate Fed Funds rate falling back to around 2.75%.

Taken together, the FOMC members’ economic and rate projections imply a need to raise the Fed Funds target rate temporarily above the appropriate long-term rate. This is probably out of concern that unemployment is too low and so the Committee must act to raise the rate above what they perceive as the normalized level in order to prevent a rise in inflation above the 2.0% target. So far, although the annual rate of increase in hourly wages has risen slightly to around 2.8% over the past few months from about 2.6% earlier in the year, the upward pressure on wages has been limited by the increase in people entering or re-entering the workforce.

FOMC members’ economic projections suggest that GDP growth will moderate from about 3.1% in 2018 to 2.5% in 2019 and then to 2.0% in 2020, as the positive effects of the tax cut subside. Rising interest rates will also serve to slow economic growth. They see unemployment bottoming out at about 3.5% in 2019 and 2020 and then rising to 3.7% in 2021 on its way back to a long-term sustainable level of around 4.5%. Inflation, meanwhile, is expected to moderate slightly from 2.1% in 2018 to 2.0% in 2019 and then rise back to 2.1% in 2020 and 2020, remaining near long-term expected levels of around 2.0%.

Thus, the FOMC believes that its actions to raise rates will keep inflation at or near its target level without slowing economic growth too much. It is not clear, however, whether the financial markets agree with the Committee’s assessment. Already, there are clear signs of the slowing in the housing market. Additional interest rate increases will slow housing further. Rising interest rates have also served to strengthen the dollar, which could put additional pressure on exports. (For now, though, industrial activity remains strong.)

The continued flattening of the yield curve suggests that the bond market is not as concerned about a pick-up in inflation as the Fed. The yield on the 10-year Treasury remains below (but just barely so) its 2018 high water mark of 3.115%, set in May, even though the FOMC has raised the Fed Funds target twice since then. The continued flattening of the yield curve suggests that the bond market has only grudgingly given the FOMC room to raise rates. If the Treasury yield curve moves closer to inverting, more FOMC members may argue against continuing to raise the Fed Funds rate. Thus, the interplay between FOMC policy and long-term Treasury yields will ultimately decide the course of interest rates.

At this point, I do not have a strong opinion of the relative attractiveness of TIPS versus Treasurys. In the short term, if headline consumer inflation picks up because of recent increases oil and natural gas prices, TIPS will probably outperform Treasurys. Beyond that, if the economy begins to show more signs of slowing and the yield curve continues to flatten (or inverts), Treasurys will begin to outperform TIPS, in anticipation that the FOMC will back away from its current plan to raise the Fed Funds target rate.

October 2, 2018

Stephen P. Percoco

Lark Research

839 Dewitt Street

Linden, New Jersey 07036

(908) 448-2246

[email protected]

© 2018 by Lark Research. All rights reserved. Reproduction without permission is prohibited.

Read more commentaries by Lark Research