Value and Growth Stocks: The Case for Being Overweight in Both

Should investors be overweight to both growth and value? Is it even possible?

The stock market is at an interesting point today, currently enjoying one of its longest expansions on record. As history has all-too well demonstrated, though, the good times won’t last forever. At some point, something has to give—but when? For many investors, looking to maximize their returns before the clock runs out on today’s bull market, the fear of missing out by adopting a defensive strategy too early is very real.

We get it. After all, who wants to leave the party when the music is still blasting? That’s why, at Russell Investments, we’re looking at equity positioning differently amid today’s market environment. As a multi-asset manager that believes in active management, we’ve noticed that rising short-term interest rates typically improve prospects for growth managers, while increasing earnings growth tends to give value managers a boost.

This conclusion brings us back to our original question: Should we be overweight to both growth and value factors in our portfolios?

If you search growth and value in your internet browser, you’ll see the words pitted against each other, rather than being complimentary. The idea of these two factors being overweight in a portfolio at the same time isn’t one often talked about. But, given today’s market backdrop, we believe it’s a viable position to take. So, the burning question naturally becomes: How? How do we achieve an overweight in these two factors at the same time even though both are often seen as opposing one another?

Growth vs. value

Let’s set the stage by first defining both. Value stocks are shares in companies that have attractive fundamentals (price-to-book ratio, price-to-earnings ratio, etc.) that are trading at a discount to the market. Financials, energy, and real estate are a few sectors that generally fall into this category. At Russell Investments, one of our strategic beliefs is that value will outperform in the long run.

Growth stocks, on the other hand, are shares of companies with higher historical and forecasted growth rates, measured by variables such as earnings and sales relative to the market. Information technology is the most notable growth sector and has been a key driver of returns over the last few years.

Recent performance

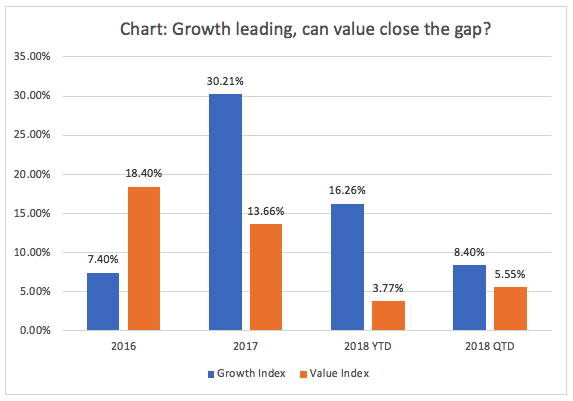

As the chart below shows, in terms of recent performance, value came off strong in 2016, only to be outperformed by growth (by more than double) in 2017. Growth continued that rally into the first part of 2018, but in the most recent quarter, value has started to close the gap. It will be important to keep an eye on these two as we approach the end of 2018. Will sentiment continue to slow for growth, allowing value to outperform for the remainder of 2018? We’ll be paying close attention to our indicators to help us forecast what could happen.

Source: Russell 1000® Growth Index, Russell 1000® Value Index. Data as of August 31, 2018. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investments

Market cycle position matters

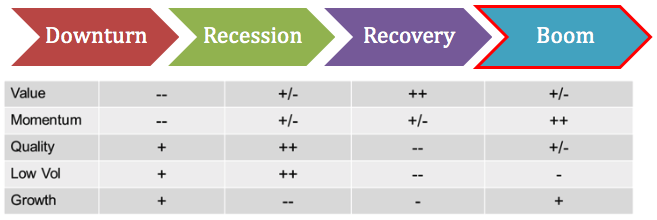

Diving into the first question above—should we overweight both of these factors?—it’s helpful to understand where we are within the market cycle today. Given underlying economic and market fundamentals, in addition to factor outperformance, we believe it’s safe to say we’re in a boom phase of the market (see graphic below). But where specifically we are within the boom phase is the ultimate question.

Why? Simply put, value and growth stocks tend to outperform during such a phase. It stands to reason, then, that if there’s still room to run during this phase, value and growth are both viable factors.

Looking further ahead, we note that value tends to be punished in a downturn phase of the market, while growth is most often rewarded. These are general assumptions, based on our research, and it should be noted that other market factors could come into play to derail these forecasts.

Source: Russell Investments research. Based on emerging markets, UK, Europe, U.S., Japan, Canada, Australia and Asia ex-Japan regions. Data from 1970-present.

Key: ++ = Strongly outperform

+ = Modest Outperform

+/- = Mixed Performance

- = Modest Underperform

-- = Strongly underperform

Value and growth through our CVS lens

At Russell Investments, we also utilize our cycle, valuation and sentiment (CVS) process to help us understand where we are in the cycle. What we’ve observed is that earnings growth has been acting as the tide to lift all boats, helping the value factor look more attractive. Moreover, some of the valuation characteristics of the value factor are discounted compared to history. Underlying valuation metrics like price-to-sales, price-to-earnings, and price-to-book ratios are all the cheapest they have been since 2016 (which was the year of outperformance for value).1 Growth, on the other hand, has become significantly more expensive since the beginning of the year, making it look unattractive from a valuation standpoint.

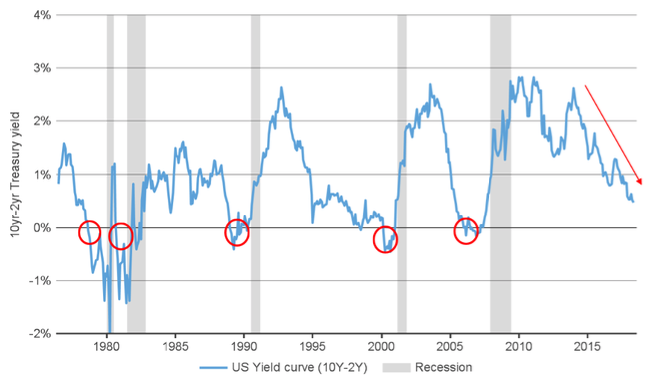

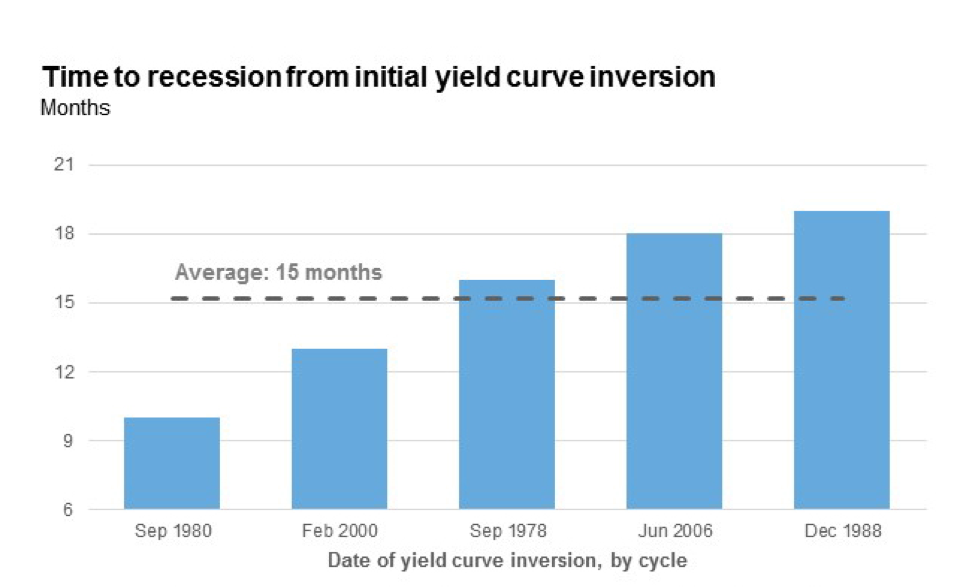

For growth stocks, rising short-term rates have historically been a tailwind—and our expectation is for that trend to continue. A chart of the U.S. Treasury yield curve helps illustrate this idea. The yield curve typically acts as an indicator of the start of a recession. As short-term rates rise and the spread between 10-year and 2-year yields becomes negative—or inverted—the market exits the boom period. This rotation then typically leads to a downturn, followed by a recession. While timing varies, the average time between inversion of the yield curve and onset of a recession is 15 months. Most notably, throughout that time, we’ve observed that growth tends to be an outperforming factor.

Source: Thomson Reuters Datastream, 4/27/2018. Past performance does not guarantee future performance.

Source: Russell Investments, Federal Reserve Board, National Bureau of Economic Research. Based on data from June 1976 to January 2018.

Since it appears likely that we still have a little way to go before a recession (see charts below), we believe having an overweight to growth in our portfolios is a practical position. However, it’s important to note that growth stocks are often not rewarded during a recession. This gets back to the importance of timing. While no one wants to leave the party too early, leaving the party too late—after the peak in equity markets has already been reached—is also punishing.

This is where we believe the importance of multi-factor investing comes into play.

Multi-factor investing: A potential way to achieve an overweight to both value and growth

Given the current positive indicators for both value and growth stocks that we see, how exactly might we achieve an overweight to both the value and growth factors in a portfolio?

Enter a multi-factor investing approach.

Traditionally, an investor holding allocations to value and growth managers may have been disappointed to learn that these exposures can offset one another when aggregated together. Fortunately, this is a problem that we believe we’re well-versed in helping to solve. A multi-asset approach allows us to hire what we believe are the best ideas and embed them within our portfolios.

We note that it’s difficult to tilt a total portfolio into exposures that we have conviction in, if the only way to control these exposures is by changing the weight of the underlying managers within the portfolio or by changing the fund-manager lineup. That’s why many of our portfolios contain an active positioning strategy that allows our portfolio managers to quickly and more precisely achieve the exposures desired at the total portfolio level, without creating a lot of turnover. Furthermore, an active positioning strategy allows us to look at the factor exposures at an aggregated level and make bets toward the desired factor exposures, such as both value and growth—and maintain this exposure even after portfolios are combined.

Another approach we use to achieve an overweight to each of these factors is through multi-factor investing, where we create an aggregate portfolio that encompasses our underlying factor portfolios. Many of our active positioning strategies are comprised of underlying Russell Investments factor portfolios. For example, we’ve created factor portfolios that are comprised of securities that fit the characteristic profile we have defined for each factor. These allow us to have more conviction in where we want the portfolio positioned amongst the factors. So then, for us to get to an overweight in both value and growth in the portfolio, we can overweight both factor portfolios to create a more diversified value and growth exposure within the portfolio.

Bringing it all together

Ultimately, we believe that today’s market dynamics are supportive of overweights to both growth and value stocks. Yes, this represents a new way of thinking—and yes, it’s a departure from the traditional structure of an equity portfolio. But this isn’t a traditional bull market. In order to potentially soak up additional returns in today’s market, we believe innovation should be at the forefront of any investing strategy. As this approach shows, we’re up for the task.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page.

Investing involves risk and principal loss is possible.

Past performance does not guarantee future performance.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

This material is not an offer, solicitation or recommendation to purchase any security. Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type.

The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional. The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Please remember that all investments carry some level of risk. Although steps can be taken to help reduce risk it cannot be completely removed. They do no not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Investments that are allocated across multiple types of securities may be exposed to a variety of risks based on the asset classes, investment styles, market sectors, and size of companies preferred by the investment managers. Investors should consider how the combined risks impact their total investment portfolio and understand that different risks can lead to varying financial consequences, including loss of principal. Please see a prospectus for further details.

Indexes are unmanaged and cannot be invested in directly.

The Russell 1000® Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 companies with lower price-to-book ratios and lower expected growth values.

The Russell 1000® Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments' management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

Copyright © Russell Investments Group LLC 2018. All rights reserved.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

UNI-11344

1 Source: Russell Investments research