The Taming of the Diversified Portfolio

The concept we discuss here goes back to before the advent of the written word, living in parables echoed in religious and secular texts alike. The precise wording has evolved, but the message has not changed materially over time. Cervantes put it on paper more than 400 years ago through the lips of Sancho Panza, and we still use a translated version of it to teach our kids: “It is the part of a wise man to keep himself to-day for to-morrow, and not to venture all his eggs in one basket.” To be more succinct, diversify. Investors have leaned on this idea for a long time, and diversification is often heralded as the “only free lunch in investing.”

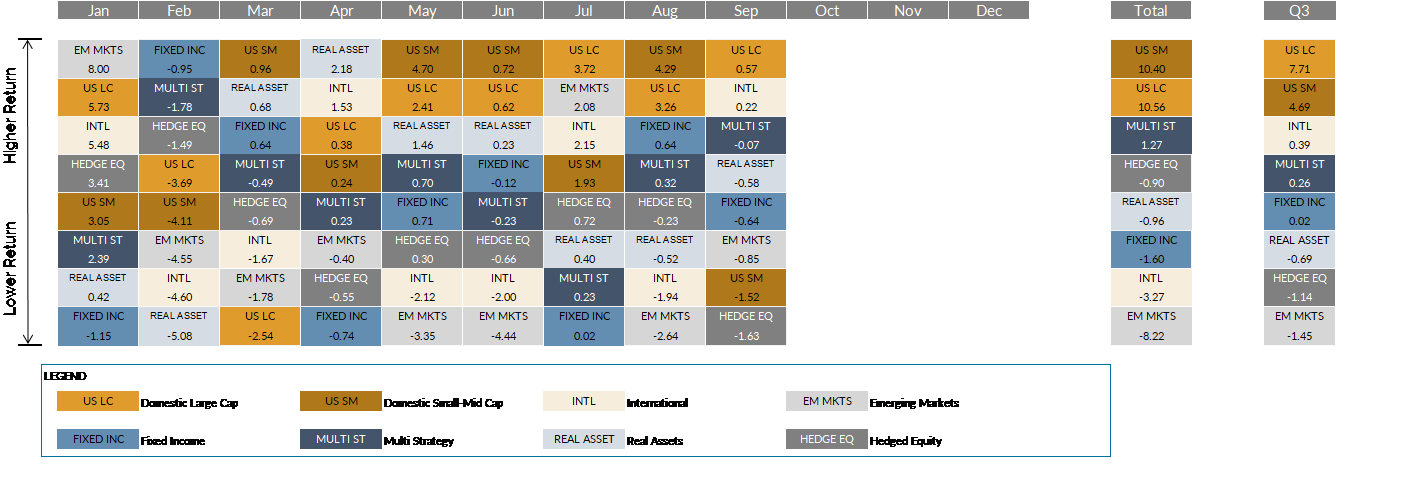

Translated into simple terms, the addition of less correlated assets to a portfolio reduces the portfolio’s risk while potentially improving expected returns. But, diversification has fallen short in recent years, leading to declarations that it is an antiquated concept with little applicability in the modern world. This year the S&P 500 Index finished the first three quarters up more than 10%. A portfolio with a 60% allocation to global equities and 40% to investment grade bonds returned less than 2% over the same period. The wide difference in performance between large cap U.S. equities and a globally diversified portfolio has come after a series of equally disappointing years. Is it time to declare diversification dead?

Investors need to remember why they initially sought a diversified portfolio. It will never be the best performing asset in the world, just as it will never be the worst performing asset in the world. The last recession and subsequent major bear market are key examples of why this is relevant. When investors looked back at 2008, very few credibly predicted the severity with which equity markets declined. From the market peak in October 2007 to the bottom in March 2009, the S&P 500 Index lost more than 50%. Investors with a 60/40 portfolio also lost money in that time, but as the markets began to rebound, given the deeper hole, it took significantly longer for equity markets to recover than a diversified portfolio. The lost decade of 2000-2010 provides the flip side of what we have seen recently. Over that 10 year period the S&P 500 Index lost a cumulative 9%, while international stocks rose 37%, commodities returned 51%, and investment grade bonds put up an astounding 85%.

We discussed a few of the most common behavioral biases last quarter and they speak to why investors struggle with a truly diversified portfolio.

- Loss aversion states that investors are more sensitive to losses than to gains, by a ratio of 2:1. Within a diversified portfolio, it should be expected that an asset somewhere in your portfolio is losing money at a given point in time. If that is not the case, are you truly diversified?

- We mentioned the home country bias exhibited by most investors, whereby the familiarity of a local stock market falsely builds investor comfort equating to a belief that market has lower risk. We are not alone in this approach. According to a recent study, Australians hold nearly 75% of their portfolios in Australian issues. Canadians hold 65% in Canada.

- Lastly, recency bias causes investors to more prominently recall and emphasize recent performance over that in the distant past, oftentimes extrapolating latest performance into the foreseeable future. A portfolio that owns different asset classes will have overachievers, naturally causing investors to wonder why they do not own more of that asset.

Investors should carefully consider their own susceptibility to recency bias in stock markets. After technology stocks peaked in 2000, they lost 80% and took more than 17 years to return to that prior peak. Only now, after another impressive run, are investors eagerly looking to return to those stocks. How many investors were proactively buying technology stocks prior to this run up? Similarly, despite the weak recent performance in emerging economy stocks, they remain the top performer over the last 15 years ending 2017.

It is helpful to look at our portfolios since the global financial crisis and wonder what could we have done differently? The answer will never be to chase yesterday’s winners. When we discuss diversified portfolios, it is done with the benefit of many years of data and evidence suggesting that a balanced approach helps minimize the highs and lows associated with investing.

Markets

Source: Morningstar, Bloomberg