US Economic Dominance

Tax cuts in the US have led to an acceleration in US economic growth this year. In September, US unemployment reached its lowest level (3.7%) in almost 50 years.1 We expect this acceleration to be temporary as the fiscal stimulus begins to fade over the coming year.

Monetary Tightening

With continued positive economic momentum, central banks have been moving towards normalizing monetary policy, with the US furthest along in the process. The Federal Reserve raised the Fed Funds rate for the third time in 2018 during their September meeting (2.00% to 2.25%). Investors are expecting roughly two more rate hikes based on current bond market pricing.2

We are Entering the Late Stage of the Economic Cycle

As central banks withdraw support, interest rates are rising, and market volatility is picking up. This is likely to produce falling asset prices and, ultimately, a slowdown in economic activity.

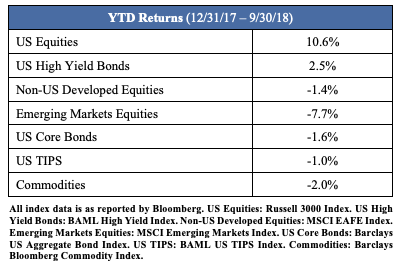

Traditional Assets are Facing Headwinds

Low yields and rising cash rates create an incentive for investors to move out of traditional assets and into cash. Below are year-to-date returns for major asset classes. All are down except for those assets (US equities and credit) that have directly benefitted from the US fiscal stimulus.2

Midterm Elections

Polls are suggesting that Democrats are likely to take the House, while the Republicans are likely to keep their Senate majority. Without a single party majority, additional fiscal stimulus (e.g., further tax cuts or infrastructure spending) is significantly less likely.

China is Slowing

China has been managing its economy through a delicate transition, which entails rebalancing its economy towards domestic consumption, opening up its capital markets, and reducing debt levels. Government steps to reduce real estate speculation and off-balance-sheet lending have produced an economic slowdown this year, with its Q3 growth rate (6.5%) reaching levels last seen in the global financial crisis.3 In addition, its currency and asset markets have responded negatively to US tariffs, which now apply to nearly half of China’s exports to the US. We expect the Chinese to respond to recent weakness with stimulus, though the US-China trade war remains a wild card.

Stress in Italy

Italy’s populist government has pushed ahead with its plans for a significant fiscal expansion, which is running into strong EU opposition. Italian bond yields climbed nearly 50 bps during the 3rd quarter, with continued increases since.3 As Italy is the world’s third largest debt issuer, Italian credit concerns can have knock on effects on broader asset markets, particularly in Europe.

Political Uncertainty in the UK

UK Prime Minister Theresa May has been losing domestic support as she struggles to find a Brexit solution that appeases the Euro-skeptic and pro-European factions of her parliamentary party. Meanwhile, the EU is reticent to grant a deal that gives clear advantages to a country leaving the Union. This raises the chances of a hard (no deal) Brexit, which would be very painful for the UK economy given its trade linkages with Europe.

Conventional Portfolios May be Challenged Looking Ahead

As we face a future of low returns and increasing risks, investors in conventional portfolios, which have enjoyed exceptional performance over the past 9 years, should consider reducing risk. We prefer to replace equities with similarly high returning, but uncorrelated strategies, which can help to maintain returns while reducing risk.

Disclosures

Advanced Research Investment Solutions, LLC (“ARIS”) is an SEC-registered investment adviser that provides investment advisory services and investment consulting services to a select set of clients and pooled investment vehicles. None of ARIS’s services are intended to represent a complete investment program.

This publication is for illustrative and informational purposes only and does not represent investment advice or a recommendation of or as an offer or solicitation with respect to the purchase or sale of any particular security, strategy or investment product. Past performance is not indicative of future results.

Different types of investments involve varying degrees of risk, including possible loss of the principal amount invested. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by ARIS), or any non-investment related content, will be profitable, equal any corresponding indicated historical performance level(s), be suitable for a client’s portfolio or individual situation, or prove successful. Nothing contained herein is intended to predict the performance of any investment. There can be no assurance that actual outcomes will match the assumptions or that actual returns will match any expected returns.

Nothing contained herein constitutes legal, tax or other advice nor is it to be relied upon in making an investment or other decision.

Certain information contained herein has been obtained or derived from unaffiliated third-party sources and, while ARIS believes this information to be reliable, neither ARIS nor any of its affiliates make any representation or warranty, express or implied, as to the accuracy, timeliness, sequence, adequacy or completeness of the information.

The information contained herein and the opinions expressed herein are those of ARIS as of the date of writing, are subject to change due to market conditions and without notice and have not been approved or verified by the United States Securities and Exchange Commission (the “SEC”), the Financial Industry Regulatory Authority (“FINRA”), or by any state securities authority.

This publication is not intended for redistribution or public use without ARIS’s express written consent.

Russell 3000: The Russell 3000 Index measures the performance of the largest 3,000 US equity market. As of the latest reconstitution, the dollar weighted average market capitalization was $58.2 billion; the median market capitalization was $589 million. An investment cannot be made directly in an index.

BAML High Yield: The BAML High Yield Index tracks the performance of US dollar denominated below investment grade corporate debt publicly issued in the US domestic market. Qualifying securities must have a below investment grade rating (based on an average of Moody’s, S&P and Fitch) and an investment grade rated country of risk (based on an average of Moody’s, S&P and Fitch foreign currency long term sovereign debt ratings).

MSCI EAFE: MSCI Europe, Australasia, and Far East (EAFE) Index represents a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. As of May 27, 2010 the MSCI EAFE Index consisted of the following 22 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom. An investment cannot be made directly in an index.

MSCI Emerging Markets Index: The MSCI Emerging Markets Index is designed to represent the performance of large- and mid-cap securities in 24 Emerging Markets. As of March 2018 it had more than 830 constituents and covered approximately 85% of the free float-adjusted market capitalization in each country. The index is built using MSCI’s Global Investable Market Index (GIMI) methodology, which is designed to take into account variations reflecting conditions across regions, market-cap segments, sectors and styles. With over $1.9 trillion in assets benchmarked globally to the Emerging Markets Index suite, MSCI is a leader in global equity indexes.

Barclays US Aggregate Bond Index: Barclays Aggregate Bond Index is a market value-weighted index that tracks the daily price, coupon, pay-downs, and total return performance of fixed-rate, publicly placed, dollar-denominated, and nonconvertible investment grade debt issues with at least $250 million par amount outstanding and with at least one year to final maturity. An investment cannot be made directly in an index.

BAML US TIPS Index: The BAML US TIPS Index is an unmanaged index comprised of U.S. Treasury Inflation Protected Securities with at least $1 billion in outstanding face value and a remaining term to final maturity of greater than one year.

Barclays Bloomberg Commodity Index: The Barclays Bloomberg Commodity index is composed of futures contracts and reflects the returns on a fully collateralized investment in the BCOM. This combines the returns of the BCOM with the returns on cash collateral invested in 13 week (3 Month) U.S. Treasury Bills.

1 Source: Bureau of Labor Statistics, United States Department of Labor

2 Source: Bloomberg.

3 Source: Bloomberg.

© ARIS

Read more commentaries by ARIS