The accommodative monetary policies implemented by the US Federal Reserve after the global financial crisis have contributed to a broad-based, sustained economic recovery. However, during the past four years there has been a notable divergence in corporate performance among the US real estate investment trusts (REITs) we cover, with some deteriorating significantly. Given this trend, as well as the late stage of the US economic expansion, Invesco Real Estate believes active management is essential to find opportunities among higher quality REITs and potentially avoid those companies which may be most exposed to further deterioration.

A closer look at REIT earnings trends

Every quarter, the 20-person Invesco Real Estate securities team evaluates all 172 names in the FTSE NAREIT All Equity REIT Index, one of the most comprehensive indexes which cover domestic REITs. We review each company’s fundamentals based upon the firm’s market cycle strength, real estate asset footprint and platform quality, balance sheet strength, corporate strategic plan and management track record. Then we rank this entire US REIT universe by these qualitative criteria, resulting in a group of potential investable candidates. Those companies failing our qualitative screens – typically one third of all REITs in our coverage universe - cannot be considered for potential investment (and are automatically sold if they are already in a portfolio).

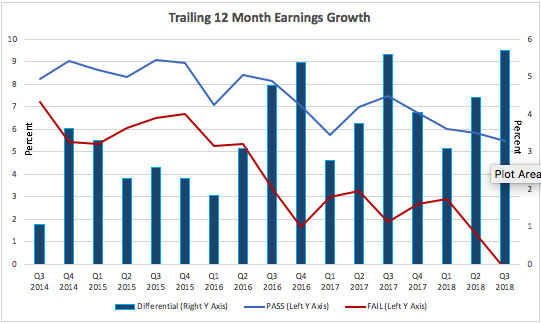

What is currently most striking about US REIT corporate performance? While earnings growth has been moderating gradually across the entire sector as the economic expansion becomes later cycle, earnings growth for companies that have passed our qualitative screens (higher quality REITs) remains strong at 5.5% - a decent rate of growth albeit a lower rate than seen in prior years. Conversely, for the one-third of US REITs that fail our screens (lower quality REITs), earnings growth has fallen dramatically from 7.2% (third quarter of 2014) to a current rate of -0.2%. This differential in earnings growth between the passing and failing companies has never been higher during the past four years.

The earnings gap is wide between higher quality (passing) and lower quality (failing) REITs

Source: Bloomberg, L.P., earnings growth data as of Aug. 30, 2018 and Invesco, passing and failing REIT data as of Aug. 30, 2018. The companies measured were the 172 REITs making up the FTSE NAREIT All Equity REIT Index. Invesco uses a proprietary process to screen REITs that includes assessment of location (market) strength, property evaluation, physical attributes (such as parking), management performance and balance sheet composition. Past performance is not indicative of future results.

Source: Bloomberg, L.P., earnings growth data as of Aug. 30, 2018 and Invesco, passing and failing REIT data as of Aug. 30, 2018. The companies measured were the 172 REITs making up the FTSE NAREIT All Equity REIT Index. Invesco uses a proprietary process to screen REITs that includes assessment of location (market) strength, property evaluation, physical attributes (such as parking), management performance and balance sheet composition. Past performance is not indicative of future results.

Striking balance sheet quality differentials

According to our ongoing analyses of the REIT sector, the balance sheet quality gap between the passing and failing companies has widened even more significantly than the earnings growth disparity might suggest. Passing companies have generally been deleveraging during the period shown in the chart below - from an average of 33% to 29%) - while failing companies have exhibited further balance sheet deterioration and increasing levels of leverage (from 41% to 47%). Our REIT investment team believes that balance sheet quality and leverage will become an increasingly important factor for performance given the potential for rising interest rates and a higher cost of capital for companies with weaker balance sheets.

Lower quality (failing) REITs have significantly higher leverage than higher quality REITs

Source: Bloomberg, L.P., balance sheet leverage data as of Aug. 30, 2018 and Invesco, passing and failing REIT data as of Aug. 30, 2018. The companies measured were the 172 REITs making up the FTSE NAREIT All Equity REIT Index. Invesco uses a proprietary process to screen REITs that includes assessment of location (market) strength, property evaluation, physical attributes (such as parking), management performance and balance sheet composition. Past performance is not indicative of future results.

Source: Bloomberg, L.P., balance sheet leverage data as of Aug. 30, 2018 and Invesco, passing and failing REIT data as of Aug. 30, 2018. The companies measured were the 172 REITs making up the FTSE NAREIT All Equity REIT Index. Invesco uses a proprietary process to screen REITs that includes assessment of location (market) strength, property evaluation, physical attributes (such as parking), management performance and balance sheet composition. Past performance is not indicative of future results.

Assessing active versus passive approaches to US REIT investments

Invesco Real Estate has observed an industry trend of passive investment managers gaining a greater share of the US REIT fund and ETF marketplace over the last five years. Part of this trend is explainable — since the global financial crisis, it has been more challenging for active managers to generate alpha as both high-quality and low-quality companies have performed similarly (and correlations within the REIT universe have remained relatively high). But with earnings growth and balance sheet quality dispersions becoming more extreme, we believe that active management in US REITs will become more prescient and timely for investors.

Sectors under pressure

Two US REIT sectors in particular have been under pressure recently in terms of deteriorating fundamentals and falling rental growth — retail and health care. We believe the potential for active managers to find growth and avoid risk in these two sectors may help investors achieve their goals.

- The retail sector has been the focus of much media attention as e-commerce has crimped the potential viability of class B and C shopping malls. In our view, those malls and related centers lacking a more diversified portfolio of food and beverage outlets, grocery stores, adjoining hotels or condominiums may find themselves on a path to obsolescence.

- The health care sector has come under pressure due to the overdevelopment of both senior housing and assisted living units — baby boomer demand may not catch up with supply for several years.

There are other REIT sectors (including lodging, apartments, self-storage and office) experiencing slowing, but still positive, rental growth. Some of this slowdown is due to new development and supply catching up to demand, specifically in the case of lodging, apartments and self-storage. Within the office sector, some of the slowing in rental growth is attributable to greater supply coupled with changes in demography and technological disruption (e.g., the rise of co-working spaces). We believe these additional sectors may benefit from active management in coming years as earnings growth and balance sheet quality differentials continue to widen.

Key takeaway

The Invesco Real Estate team believes that actively managing the higher risk portion of the REIT universe has long-term investment merit. The team may narrow the number of eligible investments that ultimately are added to portfolios as fewer pass our quality screening. And, we can overweight or underweight select stocks or sectors.

While the industry trend has recently moved towards passive management within the US REIT universe, our investment team believes that the widening dispersion of high-quality and low-quality companies — coupled with changing sector dynamics — may allow active managers the ability to demonstrate more value at this stage of the economic cycle.

About Invesco Real Estate

Invesco Real Estate has nearly 490 employees in 21 different markets worldwide with assets under management exceeding $65 billion as of June 30, 2018. Our focus areas include US real estate, global real estate, global real estate income, infrastructure and master limited partnerships.

Learn more about Invesco Active US Real Estate ETF, Invesco Real Estate Fund and Invesco Global Real Estate Income Fund.

Important information

Blog header image: Arcady/Shutterstock.com

A real estate investment trust (REIT) is a closed-end investment company that owns income-producing real estate.

The FTSE NAREIT All Equity REIT Index is an unmanaged index considered representative of US REITs.

Correlation is the degree to which two investments have historically moved in relation to each other.

Investments in real estate related instruments may be affected by economic, legal, or environmental factors that affect property values, rents or occupancies of real estate. Real estate companies, including REITs or similar structures, tend to be small and mid-cap companies and their shares may be more volatile and less liquid.

Paul Curbo

CFA® Portfolio Manager, Invesco Real Estate

Paul Curbo is a Portfolio Manager and member of the Real Estate Securities Portfolio Management and Research team with Invesco Real Estate.

Mr. Curbo entered the industry in 1993 and joined Invesco in 1998. Prior to assuming his current position, Mr. Curbo served as a senior research analyst in the real estate research group. He led one of Invesco’s regional teams and directed the firm’s research and strategy efforts in the Western region of the US.

Before joining Invesco, Mr. Curbo was a senior research associate with Security Capital Group, where he was responsible for analyzing multifamily, industrial and office real estate markets. He produced research on economic, demographic and real estate market information for Security Capital’s affiliate companies. Mr. Curbo previously held a position with Texas Commerce Bank.

Mr. Curbo earned a BBA in finance from The University of Texas at Austin and has completed graduate coursework in economic theory and econometrics at The University of Texas at Dallas. He is a CFA charterholder.

David Wertheim,

Senior Client Portfolio Manager

David Wertheim is a Senior Client Portfolio Manager focused on real asset securities. In this capacity, he works with Invesco’s real assets investment management team, serving as its representative to clients and prospects.

Mr. Wertheim began his career in 2000 and joined Invesco in 2018. Prior to joining Invesco, he was a senior client portfolio manager for real assets, commodities and equities with Deutsche Asset Management.

Mr. Wertheim earned a BBA from George Washington University with a dual concentration in international business and marketing.

Before investing, carefully read the prospectus and/or summary prospectus and carefully consider the investment objectives, risks, charges and expenses. For this and more complete information about the products, visit invesco.com/fundprospectus for a prospectus/summary prospectus.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2018 Invesco Ltd. All rights reserved.