2nd Half 2018: Change in Size of Central Bank Balance Sheets

As of the end of 2017, the Federal Reserve (Fed), European Central Bank (ECB) and Bank of Japan (BoJ) held combined assets worth approximately $14.4 trillion USD ($4.4T, $5.4T and $4.6T, respectively), representing nearly two-thirds of all the assets held by the world’s central banks.

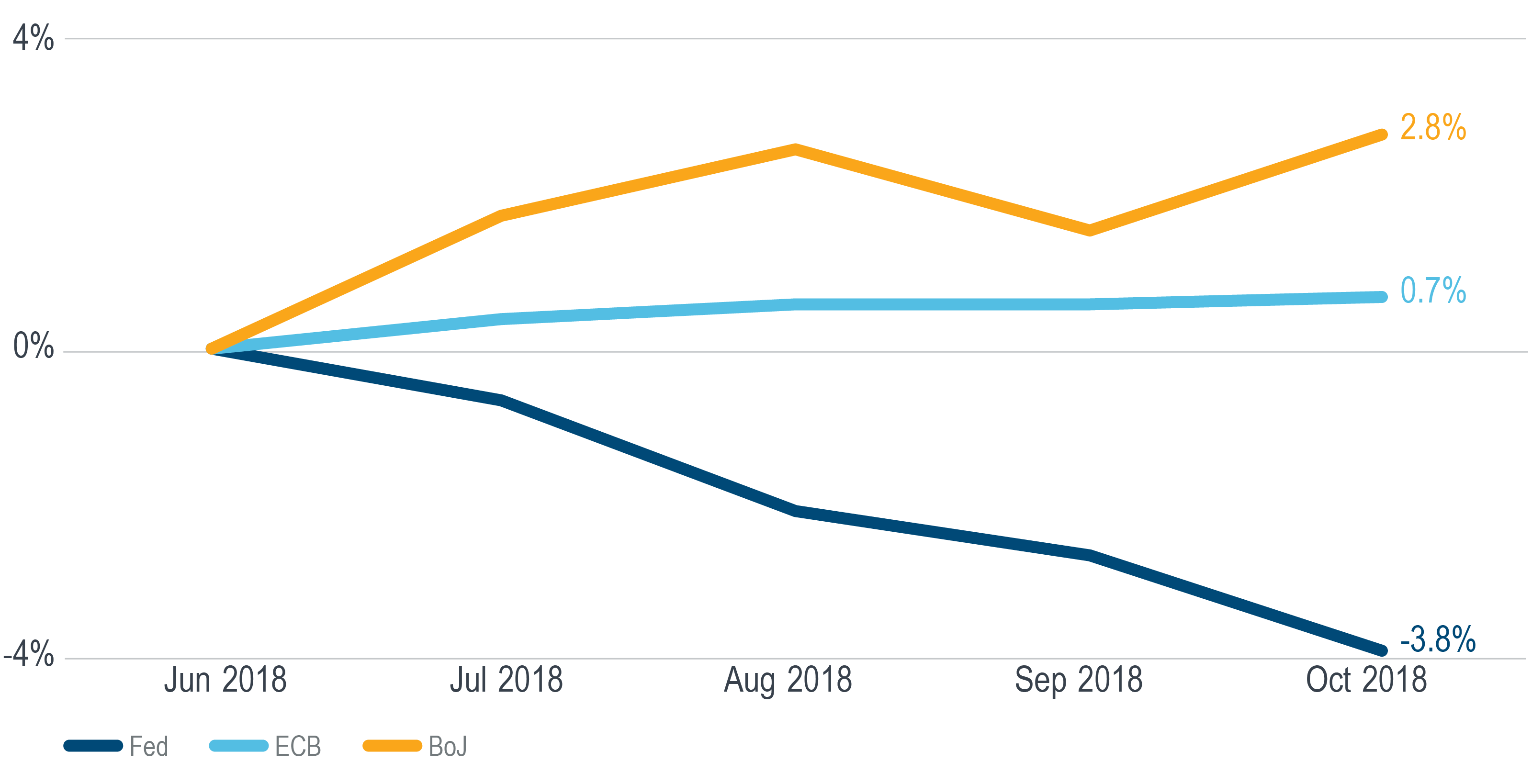

Year-to-date through October, the Fed has reduced the size of its balance sheet by approximately $310 billion or 6.9%, while the ECB and BoJ have expanded theirs by 3.4% and 5.8%, respectively.

The second half of the year, however, is shaping up differently from the first. The following table compares the changes in the size of each bank’s balance sheets during the first and second half of 2018:

2018 1st Half

Fed: -3.2% (-$143B)

ECB: +2.7% (+€121B)

BoJ: +3.0% (+¥15.6T)

2018 2nd Half (through October)

Fed: -3.8% (-$166B)

ECB: +0.7% (+€32B)

BoJ: +2.8% (+¥14.8T)

Worth noting:

- The Fed’s pace of balance sheet reduction has accelerated in the second half. From July through October the dollar reduction has already exceeded the amount of the entire first half.

- The ECB’s pace of balance sheet growth has decelerated in the second half. Four months into the second half it has grown by just 27% of the amount it grew in the first half.

- The BoJ’s pace of balance sheet growth has accelerated in the second half. The growth for January through April was ¥13.6T, while the growth for July through October was ¥14.8T.

This current trajectory suggests that before long, the BoJ may be the last of the three committed to quantitative easing (QE).

In the conclusion of a speech on November 5, BoJ Governor Haruhiko Kuroda said he hopes that, “corporate managers…will dispel the mindset and behavior that is based on the assumption of deflation and continue to take initiative in their leading roles within Japan’s economy.” He then committed that the BoJ, “will persistently continue with powerful monetary easing, thereby providing its utmost support for such initiative.”

There is no precedent for the addition and removal of such massive amounts of central bank stimulus. How this monetary experiment gets unwound and how it ultimately gets brought to an end will continue to be a matter of great interest to investors of all stripes.

1 “Japan’s Economy and Monetary Policy” Speech at a Meeting with Business Leaders in Nagoya, Nov. 5, 2018.